The above talk was given by Brian Ortelere, of Morgan, Lewis & Bockius LLP, at the 2014 Pension Research Council Conference.

The above talk was given by Brian Ortelere, of Morgan, Lewis & Bockius LLP, at the 2014 Pension Research Council Conference.

In Virginia, long-time lawmakers can boost their pensions dramatically by stepping down from the House or Senate in favor of another state job.

A state senator has drafted a bill that would limit the pension boost received by lawmakers who use this tactic.

Details of the bill from the Roanoke Times:

Quitting the Virginia House or Senate for a state job can sharply boost a legislator’s retirement benefits, and state Sen. David Marsden would like to change that.

Marsden, D-Fairfax, has introduced a bill meant to make trading elective office for state employment less of a financial windfall. Legislators who step down in the middle of their terms to take state jobs would still see their pension benefits grow, but more slowly than they do now.

“I think it rubs people the wrong way that somebody gets appointed for political purposes and then hits this bonanza,” he said. “Your retirement should be rewarded, but not with such an amazing windfall.”

State senators and delegates earn about $18,000 a year in positions that are considered part-time, but which count as full time in the state retirement system. Legislators who serve 30 or more years are eligible for the state’s full pension benefit, which is about half their annual salary — about $9,000 a year.

That figure balloons if the legislator takes a high-paying state job, since pension benefits are based on an average of the employee’s last three years of service, or five years for employees who began after this past Jan. 1. A long-serving legislator who puts in three years in a $100,000-a-year job would then receive an annual pension of about $50,000 a year.

Under Marsden’s bill, the pension benefit would be based on an average of 10 years’ salary for anyone who sees a dramatic spike in salary — exceeding 400 percent — in the last four years of service.

The bill hasn’t come out of nowhere. The FBI is currently investigating a Virginia lawmaker who did exactly what the bill aims to prevent: quit his post mid-term in favor of a high-paying state job. From the Roanoke Times:

Marsden proposed the legislation at a time when the FBI is investigating a state senator who quit in June amid job talks, and as state lawmakers prepare to tighten the state’s ethics laws in response to the conviction in September of former Gov. Robert McDonnell and his wife, Maureen, on federal corruption charges.

Phillip Puckett, D-Russell County, abruptly resigned the evenly divided state Senate in June with plans to take a high-paying job with the Republican-controlled state tobacco commission. His exit handed control of the chamber to the GOP in the middle of a standoff over Medicaid expansion. Democrats cried foul, and the FBI launched an investigation. Puckett said there was no quid pro quo and, amid the uproar, withdrew his name from consideration for the tobacco commission post.

In 1997, then-Gov. James Gilmore III, a Republican, named a Democratic state senator from Loudoun County, Charles Waddell, his deputy transportation secretary, a move that gave the GOP control of the Senate. Gilmore also appointed a Democrat to head the Department of Conservation and Recreation, creating an opening for a Republican to win a seat in the House.

Virginia Gov. Terry McAuliffe hasn’t taken a position on the bill.

Photo by Anderskev – Own work. Licensed under Creative Commons Attribution 3.0 via Wikimedia Commons

Omaha officials were planning on re-negotiating the city’s contract with police officers, and those negotiations were likely to include some changes to pension benefits – one of the city’s top fiscal priorities in 2015 is easing its unfunded pension liabilities.

But a judge ruled last week that the City didn’t provide labor groups with written notice that it would be re-opening negotiations. As a result, the police officers’ current contracts will not expire by the end of the year.

That could make it more difficult for the City to re-negotiate contracts to its liking.

More from KETV Omaha:

The city of Omaha will appeal a ruling that determined its labor agreement with the police union rolled over into 2014.

It’s a move the city calls surprising and disappointing.

[…]

“An appeal is necessary to protect the city’s right to achieve additional pension reform in 2014,” said Mayor Jean Stothert. “From the outset, we informed the OPOA that pension reform was one of our top priorities. Addressing the unfunded pension liability cannot wait. The OPOA must work with us, not look for gotcha tactics to delay negotiations.”

[…]

The union filed the lawsuit in June, alleging the city did not provide written notice to open contract negotiations by the April 1 deadline, and therefore, the current labor agreement, which was set to expire on Dec. 21, 2013, automatically rolled over into 2014.

On Wednesday, Douglas County District Court Judge Joseph Troia issued a ruling in favor of the police union.

“Neither the Association nor the City served written notice upon the other before April 1, 2014 of its intent to reopen negotiations,” the ruling said.

Troia wrote that the city’s written request to reopen negotiations didn’t come until April 17, when the city’s negotiator sent an email to the president of the police union.

Omaha has sent a letter to the union requesting a formal start to 2015 negotiations.

Last month, a circuit court struck down Illinois’ pension reform law, deeming it unconstitutional.

Scott Reeder, a journalist who has covered politics across the country for 25 years, wrote about what could happen if the Supreme Court upholds the circuit court’s ruling in his column in the Journal Standard:

Belz’s ruling sets the stage for the crisis to deepen.

While government worker unions were touting the ruling as a victory, it’s actually sowing despair for many current employees and sets the stage for generational warfare.

If the high court upholds this ruling, tax dollars that would be go to support schools, prisons and other state services will be diverted to fund pensions.

Look for teachers, prison guards and other state workers to receive pink slips to free up money for increased pension payments.

Who else but government workers routinely retire in their 50s, have guaranteed cost of living adjustments and pensions guaranteed to grow until the day they die?

Not most of us in the private sector, that’s for sure.

Things won’t be pretty during the 2015 legislative session, which begins in January.

Don’t be surprised if deep cuts are made in state spending, less money flows to schools and more government workers head toward the unemployment line.

And things could get worse when summer comes. That’s when the labor contract with the largest state workers’ union expires.

One should expect Gov.-elect Bruce Rauner to demand wage concessions.

It’s simple math.

With more money going to pensions, less will be available for wages and other benefits.

Of course, the Illinois Supreme Court could rule that the crisis is so extreme that the state’s emergency powers allow it to reshape pensions on their own.

Just how severe is the crisis?

If all of state government were to shut down and its entire operating budget were diverted to fund pensions, Illinois pensions would still be in the hole three years from now.

Now, that’s a crisis.

Read the entire piece here.

The Kentucky Teachers’ Retirement System (KTRS) and the Kentucky Employees Retirement System Non-Hazardous Plan (KERS Non-Haz) could both be in line for state money sooner than later.

But there might be some strings to that state funding, as lawmakers push for more transparency around investments and placement agents associated with the pension systems.

One lawmaker wants the pension systems to make the search for investment firms more competitive – and more public. From the Lexington Herald-Leader:

Rep. Jim Wayne, D-Louisville, wants the pension systems to use the state’s competitive bidding process to solicit investment proposals, rather than award the lucrative deals privately. Terms of each deal, including the management fees, would be made public. Wayne also would ban payments to third-party “placement agents,” middlemen who help private investment firms sell their products to pension funds.

“The status quo works for the special interests on Wall Street because it hides what they’re making off our pension system,” Wayne said.

Another lawmaker wants to know the fees paid to placement agents, as well as the pension benefits received by state lawmakers:

Sen. Chris McDaniel, R-Taylor Mill, wants full disclosure of placement agent fees. He also wants the public to see how much money individual members of the General Assembly expect to collect through pensions or how much they do collect if they are retired. Kentucky’s part-time lawmakers not only have awarded themselves state pensions, but they also carefully keep them in a separate system, apart from KRS, that is 62 percent funded.

Last winter, several bills along these lines were ignored by House and Senate leaders, including one that would have required public disclosure of all state retirees’ pensions. This time, McDaniel said, he has narrowed the focus to his fellow lawmakers.

“I’ve told people, 95 percent of state workers don’t receive a very big pension when they retire. But there are a handful of pension abuses, and it would be useful for us to understand how it works. So at the very least, the legislature can lead from the front and require transparency for its own pensions,” McDaniel said.

Not everyone in Kentucky politics agrees with the transparency initiatives. In fact, one powerful lawmaker says he won’t consider either of the aforementioned ideas:

House State Government Committee Chairman Brent Yonts, D-Greenville, said he’s not inclined to consider Wayne’s or McDaniel’s bills this winter.

“I’m reluctant to support a can-opener approach to the pension system without knowing the consequences of that and without knowing why it’s currently done this way,” Yonts said.

Outside investment managers might not want to accept KRS’ and KTRS’ money if they know their fees will be publicly disclosed, Yonts said. And nobody who gets a state pension should have to share that information with the public, he said.

“Frankly, I don’t think that’s the public’s business,” Yonts said. “They have access to the public payroll and salary information. They can theorize about what we’re going to collect in pensions. But the public is not entitled to know every last little thing about us.”

Both of the state’s major pension plans are dangerously underfunded, but the KERS Non-Haz plan is among the unhealthiest in the country, with a funding ratio of 21 percent. KTRS is 52 percent funded.

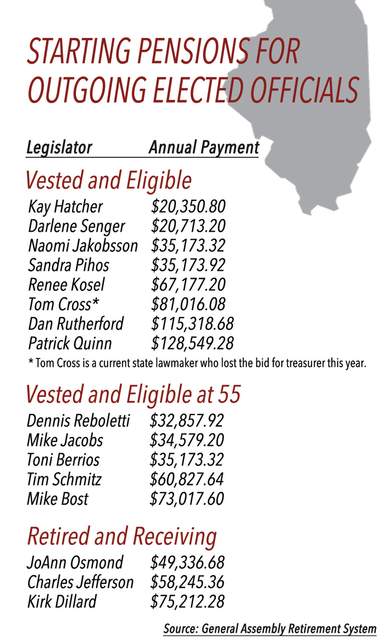

Here’s a rundown of the eligible pensions of Illinois elected officials due to leave office in 2015. In addition to the above pension benefits, any lawmaker who served 4 years in the state’s General Assembly — and was elected before 2011 — can receive free health insurance for their rest of their lives.

Graphic credit: Scott Reeder at the Journal-Courier

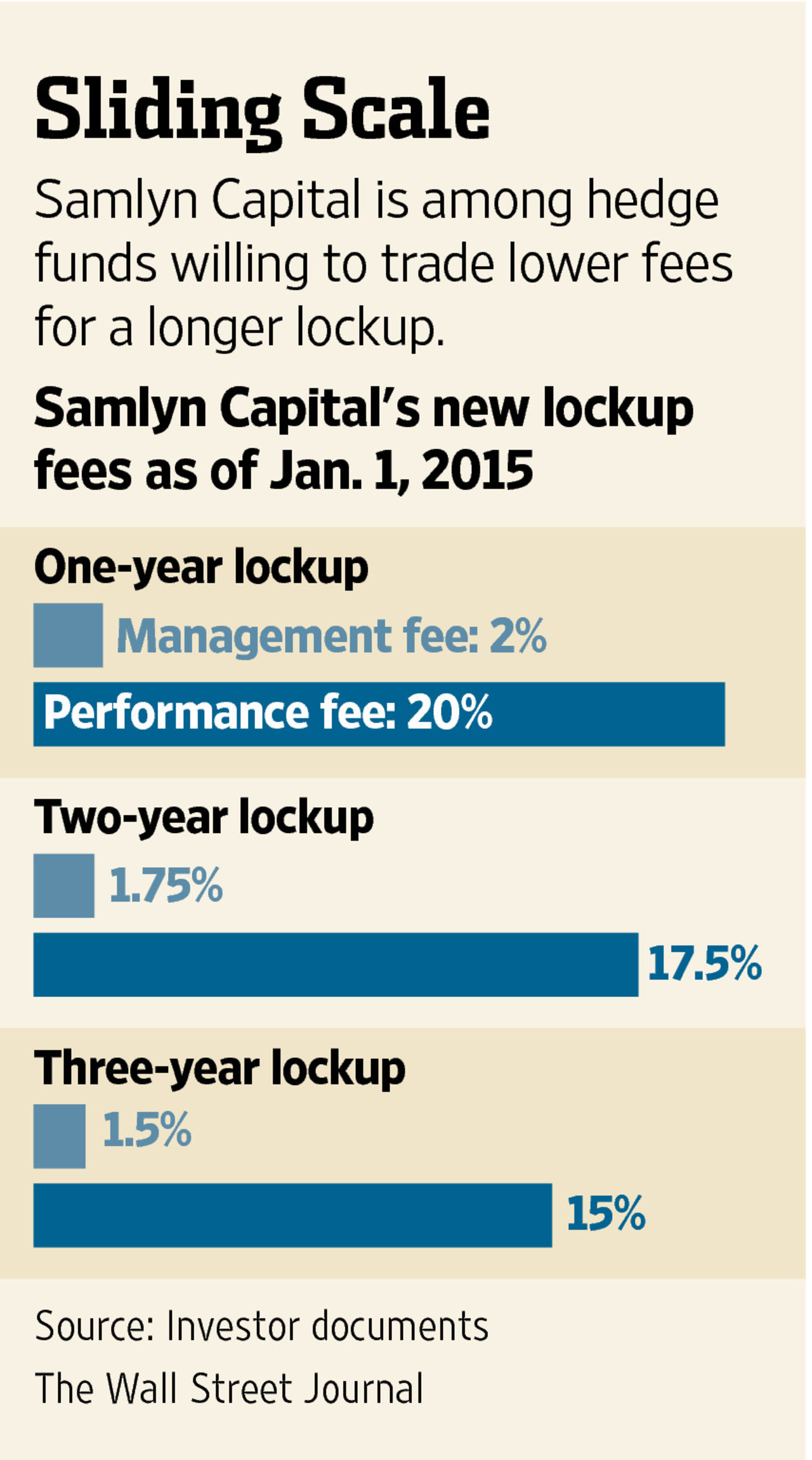

Hedge funds are looking to lock up investor funds for longer periods of time — 66 percent of hedge funds aimed to lock up funds for one year or more in 2013, according to a survey by eVestment.

In exchange, funds are willing to revise their fee structures downward.

From the Wall Street Journal:

Managers say tying up investor money for a year or more enables them to buy less easily tradable but potentially more profitable assets. It also reduces the pressure from monthly or quarterly redemption requests when performance wanes.

Extending the term also allows managers to distinguish themselves from the growing cadre of “liquid alternative” mutual funds that try to replicate hedge-fund-style trading but must allow daily redemptions.

[…]

Two-thirds of new hedge funds demanded a lockup of one year or more in 2013, a 30% increase from the previous year, according to the most recent data available from research firm eVestment. The average fund has a lockup of 377 days, eVestment said. Those pushing for longer terms include funds managed by industry stalwarts like Fir Tree Inc., GoldenTree Asset Management LLC, Trian Fund Management LP and Viking Global Investors LP, said people with knowledge of the funds.

The fact that investors have been receptive to longer lockups could indicate higher confidence:

That investors are agreeing to the extended terms, or lockups, demonstrates a significant shift in confidence since the financial crisis, when trust was shaken by rapid market losses and some fund managers prevented investors from withdrawing their money. That was quickly followed in late 2008 by Bernard Madoff ’s admission he had been running a Ponzi scheme, causing billions of dollars in losses for his investors.

“As we move further and further from 2008, people are getting more comfortable,” said Spiros Maliagros, president of $3 billion hedge-fund firm TIG Advisors LLC.

But some investors are skeptical of longer commitments:

Some observers warn that investors should be careful about allowing a manager to keep their money for so long, pointing back to the crisis when some hedge funds—particularly those holding less-liquid assets— halted withdrawals. Some investors still haven’t been paid back.

“People have forgotten a lot of the lessons from the crisis,” said Andrew Beer, chief executive of Beachhead Capital Management, which invests in hedge funds.

Several investors said they were skeptical that many hedge funds, particularly those that invest in markets that are easily traded such as stocks, need the extra leeway. Some pointed to the recent underperformance of these equity-focused funds relative to their benchmark markets as a risk of extended lockups.

View the graphic at the top of this page to see how hedge funds are changing their fee structures for longer commitments.

North Carolina’s state-level pension funds, jointly managed by the state Treasurer, collectively declined 1 percent in the 3rd quarter after the funds’ stock portfolio turned in weak returns.

North Carolina’s state-level pension funds, jointly managed by the state Treasurer, collectively declined 1 percent in the 3rd quarter after the funds’ stock portfolio turned in weak returns.

From the News Observer:

The slight decline was largely the result of losses in the fund’s stock portfolio.

Stock investments, which accounted for 43 percent of the portfolio, declined 2.9 percent in the third quarter and are up 10.9 percent over the past year. Returns are calculated after deducting fees paid to money managers hired by the state.

Fixed-income investments, which account for 30 percent of the portfolio, gained .4 percent in the quarter and have returned 5.9 percent over the past 12 months. Other 12-month returns for the portfolio: real estate, 17.9 percent; alternatives such as hedge funds, 17.5 percent.

The pension fund’s assets at the end of the third quarter were valued at 88.4 billion, down from $90.1 billion at the end of its fiscal year in June.

The pension fund provides retirement benefits for more than 900,000 workers, including teachers, state employees, firefighters and police officers.

The state Treasurer’s office manages assets for the Teachers’ and State Employees’ Retirement System, the Consolidated Judicial Retirement System, the Firemen’s and Rescue Workers’ Pension Fund, the Local Governmental Employees’ Retirement System, the Legislative Retirement System, and the North Carolina National Guard Pension Fund.

A Star-Gazette investigation has revealed that retirees are leaving New York due to high cost of living and taxes – and since 2004, the fleeing retirees have cost the state over $20 billion in lost tax revenue.

More from the Star-Gazette:

Between 2004 and 2011, Internal Revenue Service data that tracks taxpayers moving in and out of states showed that New York lost $20.5 billion in total income with nearly 40 percent of that income flowing to Florida, a state that assesses no income tax. Not all that sum can be attributed to retirees, but it indicates that New York is losing both retirees and a share of its working core.

In 2012, more Boomers left New York — after accounting for those coming and those going — than any other state in the nation.

While New York’s retirees have long been been fleeing to Florida and other warmer states to escape the cold weather, the outflow is increasing. Now, even those retirees who would have preferred to stay in New York with the cold winter weather are moving south for a more hospitable tax climate.

“Economically speaking, the Baby Boomers are a powerhouse group, and they’re heading for the hills,” said David Irwin, communications manager for AARP in New York.

Retirement planners say they are seeing an increasing trend among Baby Boom retirees opting to leave New York. The movement that should alarm policymakers because it poses a potential for drastic shortfalls in state income tax revenue in future years, say economic experts.

More numbers on the migration out of New York reveal it’s not just retirees that are leaving:

Retiree migration is part of a larger issue for New York: The state is losing the competitive battle for all residents.

During the 12 months ended July 1, 2013, the Census Bureau estimated New York lost 104,000 residents to other states, according to data compiled by the Empire Center, The number was the largest net domestic migration loss sustained by any state, according to Empire Center calculations.

“I’m not sure it’s on the radar as much as it needs to be,” said Assemblywoman Donna Lupardo, D-Endwell, who has expressed concern that by the time state reacts to boomer flight it may be too late. “Hopefully, we can add some urgency to the issue.”

[…]

A recent survey by New York’s AARP chapter estimated that 60 percent of the state’s Baby Boomers expecting to retire in the coming years have plans to move from the state, exporting more than $105 billion in income annually.

View the graphic below to see the states retirees are going to.

The Virginia Retirement System (VRS) has committed $100 million to a Blackstone real estate fund that will invest in large office, retail, and apartment properties.

From IPE Real Estate:

The Virginia Retirement System (VRS) has allocated $100m (€80.1m) to the core-plus Blackstone Property Partners fund.

The open-ended fund, which invests in a combination of core, value-added and opportunistic strategies, is targeting returns of between 9% and 11%.

[…]

The pension fund is the third to commit to the Blackstone vehicle, following $100m in overall commitments from the Arizona State Retirement System and the Texas Permanent School Fund – the latter being one of the first to invest in the fund.

Blackstone is co-investing $75m in the fund, which will be 50% leveraged.

The manager will buy larger properties and portfolios across the office, industrial, retail and apartment sectors.

Blackstone, traditionally an opportunistic fund manager, can buy either directly or invest in real estate operating companies.

VRS, which has no targeted allocation to real estate, had a total $6.84bn in its real assets category as of September.

VRS manages $66.1 billion in assets.