Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

The Wall Street Journal reports, Chicago Pension Nightmare:

The hits keep coming for Chicago Mayor Rahm Emanuel. On Thursday the Illinois Supreme Court struck down the city’s pension reform, which required city workers to chip in more to their retirement plans, raised the retirement age and cut back on cost-of-living adjustments. But there may be a silver lining for the fiscal basket case known as Illinois.

The Illinois court said Chicago’s 2014 reforms violate a provision of the state constitution that bans diminishing existing pension benefits. This is legally debatable, but the court’s ruling wasn’t surprising since it had already knocked down state pension reforms signed by previous Governor Pat Quinn.

The ruling further limits Mr. Emanuel’s fiscal options as pension payments take an ever-growing share of city revenues. On Thursday the gracious souls at the Chicago Teachers Union announced a one-day walkout on April 1. The CTU isn’t allowed to strike until this summer, but CTU president Karen Lewis told her members not to worry: “What are they going to do, arrest us all? Put us all in jail? There’s not 27,000 spaces in the Cook County Jail right now.” Ah, she cares so deeply for the children.

The ruling may be better news for Illinois Governor Bruce Rauner, who has been trying to reform the state pensions amid a hostile Democratic legislature. The court said in its Chicago ruling that a reform would be constitutional if workers had a choice to go into a modified or lower-benefit structure.

Mr. Rauner has endorsed the outline of a plan created by state Senate President John Cullerton that would let workers choose between capping their pensionable salary and collecting more generous cost-of-living increases during retirement, or collecting slightly lower cost-of-living increases during retirement based on a higher pensionable salary.

Mr. Cullerton has since distanced himself from his own handiwork under union pressure, but something will have to give or Illinois and the City of Big Unfunded Pension Obligations will go broke.

John O’Connor of the Associated Press also reports, Illinois Supreme Court strikes down Chicago pensions plan:

The Illinois Supreme Court dealt another devastating blow Thursday to the state’s impatient attempts to control ballooning public pension debt, striking down a law that would have cut into an $8 billion hole in two of Chicago’s employee retirement accounts and leaving officials searching for new options to shore up an already wobbly program.

The city had hoped that by pointing to the steep increase in taxpayer-fueled contributions the law required it would be able to sidestep a widely expected ruling that the plan violated the Illinois Constitution’s protection against reducing pension benefits.

But the court’s unanimous finding in favor of pension participants who pointed to reduced future benefits and higher contributions sends the city back to the bargaining table.

Republican Gov. Bruce Rauner used the ruling the tout a proposal by Democratic Senate President John Cullerton that would offer workers a choice of future cost-of-living increases based on current salary, or lowered increases tied to future pay raises. The idea is, benefits already collected don’t go away.

“We’ve got to stop changing and taking away peoples accrued pension benefits,” Rauner said at a stop in Paxton, according to audio released by his office. “Let’s propose changes for future work with ‘consideration’ so teachers or police officers or public places can choose different pensions for the future.”

An expert on Illinois finances said it’s time to amend the Illinois Constitution to make the pension protection language clear. Lawmakers vowed to keep trying.

To stave off insolvency by 2029, the law forced the city to significantly ramp up its annual contributions, but also cut benefits and required larger contributions from about 61,000 current and retired librarians, nurses, non-teaching school employees laborers and more.

Critics targeted the law from the start, in part because it addressed only two funds — civil servants and laborers. When including police and fire pension programs, the city’s total liability was $20 billion — not counting a $9.6 billion shortfall in the Chicago Public Schools teachers’ pension account. The City Council approved a $543 million property-tax increase last fall — to deal with shortages in police and fire funds.

The order came less than a year after the high court used the same reasoning to shoot down a separate pension bailout: the $111 billion deficit in state-employee retirement accounts.

And other cities are not far behind, facing similar shortfalls.

Laurence Msall, president of the Civic Federation, a Chicago-based tax policy and research group, suggested the iron-clad constitutional language threatens any proposal. He suggests a constitutional amendment that loosens its restrictions.

“We’re not advocating for any specific plan,” Msall said. “We’re supporting the need for clarity in the constitution so those ideas can be legislated.”

Chicago Mayor Rahm Emanuel, who inherited the crisis, disagreed with the ruling but pledged to re-convene negotiations on a new framework.

“My administration will continue to work with our labor partners on a shared path forward,” the Democrat said in a statement.

The four unions representing the plaintiffs were more sanguine.

“This ruling makes clear again that the politicians who ran up the debt cannot run out on the bill or dump the burden on public-service workers and retirees instead,” the unions said in a joint statement.

Margaret Cronin Fisk, Elizabeth Campbell, and Janan Hanna of Bloomberg also report, Chicago’s Plan to Overhaul City Pensions Dashed by Top Court:

Chicago’s plan to ease its $20 billion public-worker pension deficit was ruled illegal by the Illinois Supreme Court, a decision that the city warned may lead to the funds’ running out of money and worsen its financial strains.

The Chicago plan, passed in 2014, violates the Illinois Constitution, which bars the diminishing of public pensions, the court said Thursday. The finding upholds a lower court decision from July and follows a similar ruling by the Illinois Supreme Court last May preventing changes to the state’s pension funds.

“It’s disappointing, but not unexpected,” said Paul Mansour, head of municipal research at Conning, which oversees $11 billion of state and local debt, including Chicago securities. “It will take longer to bring these costs under control absent the ability to enact common sense reforms that were negotiated.”

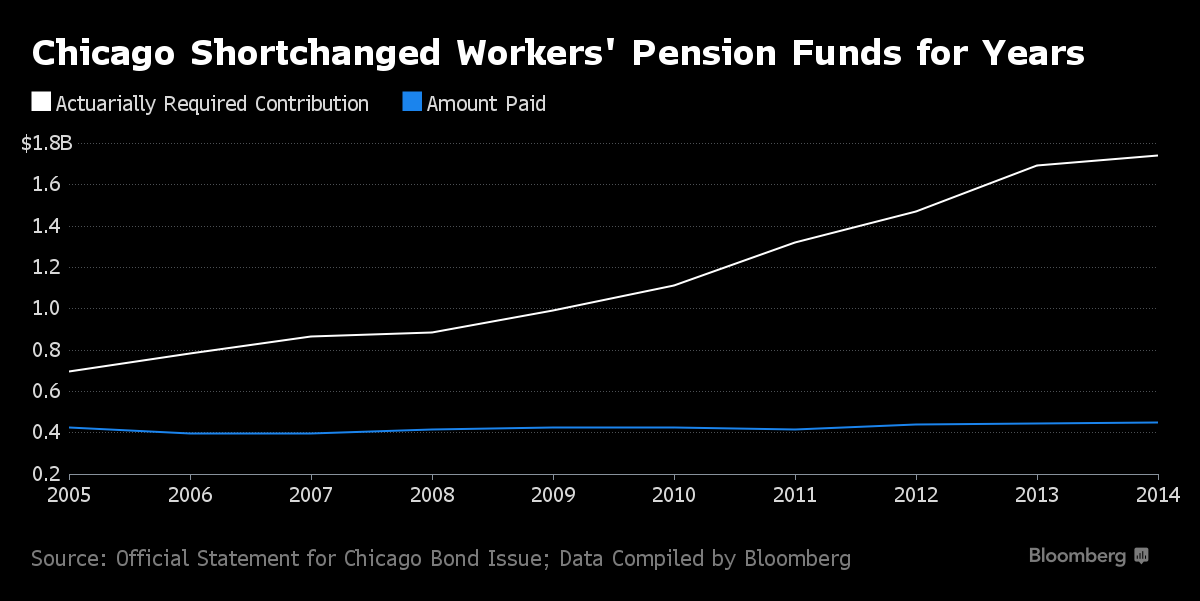

The city, the third-largest in the nation, shortchanged its pensions over the last decade, creating a shortfall that’s left it with a lower credit rating than any big U.S. city except once-bankrupt Detroit. Under the now void law, its projected annual payment of $886 million due this year to its four retirement funds was more than twice what it was a decade ago, spurring officials to adopt a record property-tax increase to ease the impact on the budget.

The ruling in the Chicago case impairs Mayor Rahm Emanuel’s efforts to pare a deficit that threatens the city’s solvency. The defeat leaves officials racing to devise new ways to shore up retirement system, though it will also save money in the short term because the overhaul required the city to boost contributions to its municipal and laborers funds. The two cover about 60,000 workers and retirees.

“My administration will continue to work with our labor partners on a shared path forward that preserves and protects the municipal and laborers’ pension funds, while continuing to be fair to Chicago taxpayers and ensuring the City’s long-term financial health,” Emanuel said in an e-mailed statement.

Workers hailed the decision for eliminating the risk that promised benefits will be scaled back. “Today’s ruling strengthens the promise of dignity in retirement for those who serve our communities, and reinforces the Illinois Constitution, our state’s highest law,” city unions said in a joint statement.

The court’s ruling comes almost 11 months after it unanimously struck down a 2013 law to alter Illinois’s retirement system, saying the changes to solve the state’s $111 billion pension shortfall violated constitutional protections of workers’ benefits. That holding led Moody’s Investors Service to cut Chicago’s credit rating to junk in May, citing the increased risk that the city’s law would also be thrown out.

Moody’s, which has a negative outlook on Chicago’s Ba1 rating, one step below investment grade, said it would continue to assess its plans to fix pensions in the wake of the ruling.

Ruling Expected

Before the ruling, Moody’s said the city could get hit with another downgrade if the court sided with unions and officials don’t develop and enact an alternate plan. Unlike cities such as Detroit, Chicago can’t file for bankruptcy protection to cut its debts because Illinois law doesn’t allow it.

There was little trading in Chicago bonds after the verdict, which investors had predicted would not go in the city’s favor.

The ruling was an “expected setback for the city,” said John Miller, co-head of fixed income in Chicago at Nuveen Asset Management, which oversees about $110 billion in munis, which includes Chicago debt. The city has a growing and diverse economy, he said, citing increasing corporate relocations and a rise in assessed valuations among other positives.

“They have time and they have strength to pull from,” Miller said. “I think other reform models that could pass muster are still being worked on. They tried one type, and that one type didn’t work, so they got to try another model.”

Chicago argued that its plan was different from the state version because it increased city funding of the municipal workers’ and laborers’ pension funds, essentially protecting benefits by ensuring the funds don’t go broke. The plans for fire and police retirees weren’t covered by the overhaul.

Accrued benefits shouldn’t be changed, Illinois Governor Bruce Rauner told reporters on Thursday. He reiterated the importance of his agenda, stalled in the Democrat-led legislature, to bolster the state economy through limits on unions and property tax relief.

“I’m not going to bail out Chicago, but our reforms structurally will allow Chicago to solve a lot of its own problems,” Rauner said.

The affected plans cut future cost-of-living raises. Lawyers for unions sued the city, arguing that any reduction in benefits was illegal. The court agreed.

“The statutory funding provisions are not a ‘benefit’ that can be ‘offset’ against an unconstitutional diminishment of pension benefits,” the opinion reads.

The city’s measures were intended to make the laborer and municipal worker pensions 90 percent funded by the end of 2055. The municipal workers’ pension was only 42 percent funded, and the laborers only 64 percent funded, at the end of 2014, city documents show.

Unfunded liabilities are increasing each day by an average of $2.48 million, city lawyers said in court papers. One fund will be out of money within 10 years, the other in 13, they said. The court rejected that as a justification for reducing benefits.

“To put it simply, in 10 years, the members of the Funds will be no less entitled to the benefits they were promised,” the opinion reads. “Thus the ‘guaranty’ that the benefits due will be paid is merely an offer to do something already constitutionally mandated by the pension protection clause.”

The case is Jones v. Municipal Employees Annuity and Benefit Fund of Chicago, 119618, Supreme Court of Illinois (Springfield).

In its editorial, the Chicago Tribune laments, Pension ruling another blow to Chicago taxpayers — and Emanuel:

The Illinois Supreme Court ruled unconstitutional another pension reform law on Thursday, this one affecting Chicago and splashing more red ink on fragile, debt-ridden city finances.

The court’s decision to toss Chicago’s pension reform law, which the Illinois legislature approved in 2014 as an attempt to rescue pension funds for municipal workers and laborers, was not a surprise. Nor is its ripple effect: As the opinion states and unarguable math attests, those two funds remain on track to go insolvent “in about 10 and 13 years, respectively.”

The court previously had twice ruled that an Illinois Constitution pension clause protects retirement benefits promised from a worker’s start of public employment. The law the justices rejected had required certain city of Chicago workers to pay more toward their pensions, scaled back cost-of-living increases upon retirement, and raised the retirement age. The court ruled that those changes violate the constitution’s provision that membership in any pension or retirement system “shall be an enforceable contractual relationship, the benefits of which shall not be diminished or impaired.”

The decision repudiates Mayor Rahm Emanuel’s strategy for salvaging a vastly underfunded Chicago pension system that also covers public safety workers — police and fire — and Chicago teachers. Emanuel persistently has argued that because 28 of 31 unions affected by the 2014 reform law had agreed to it. Emanuel said that because the law would shore up the funds in the long run and thereby protect benefits for retirees, it would meet constitutional muster.

But the Supreme Court disagreed. In a 2015 ruling rejecting a pension reform law affecting state lawmakers, the justices faulted state lawmakers for not making adequate payments into their pension system. Thursday’s ruling similarly blamed city leaders for failing to make adequate payments into City Hall’s pension funds: “The pension code continued to set city contribution levels at a fixed multiple of employee contributions. This contribution level had no relationship to the obligations that the funds were accruing.” To rule in favor of the law would mean that the court would have to “ignore the plain language of the constitution.”

Translation: City and state politicians have known well that they were awarding pension benefits that Illinois governments cannot afford. Rather than properly fund pension systems, the politicians have spent on other priorities the tax revenues they should have set aside to fulfill all the generous retirement promises they made to their friends in public employees unions.

Justice Mary Jane Theis wrote the 5-0 opinion. Justices Anne Burke and Charles Freeman did not take part in the decision.

We supported this pension reform law, and the state law, for a number of reasons, including getting language before the courts for a decision. We now have it.

For city taxpayers, the impact of Thursday’s ruling is menacing. In essence the court is saying that the responsibility to deliver benefits the politicians have pledged to public workers falls on taxpayers’ shoulders. Barring some major reforms that do meet constitutional tests — or the long overdue government streamlining and cost-cutting that city and state pols chronically resist — taxpayers will have to bail out not only these pension funds for municipal workers and laborers, but also the similarly endangered funds for police officers, firefighters and teachers.

Add in taxpayers’ liabilities for Cook County workers, whose pension system is listing. Emanuel and Cook County Board President Toni Preckwinkle already have backed huge tax hikes to help address their respective pension shortfalls.

And don’t forget the underfunded pension systems for state workers, downstate teachers, university workers, retired lawmakers and some suburbs’ workers.

With the Supreme Court sticking to its rigorous interpretation of the pension clause — the justices even protected health care for retirees in a 2014 decision — there seems to be little room to extract from public workers that “shared sacrifice” the politicians love to talk about.

No, unless Illinois pols institute massive reforms to the cost of governance, taxpayers can expect to bear the brunt of the pension crisis our elected officials have created in their name.

The taxation required to support the huge enterprise of Illinois government already is monumental — and now it’s likely to grow. Blame decades of mismanagement at all levels of representation.

Borrowing to pay for operating expenses has been the path to ruin. This new City Hall obligation comes on top of billions of borrowing throughout city, county and state governments.

As you prepare to vote in the November general election, remember: Piling debts upon debts can no longer be the way Illinois and Chicago operate.

Piling debts are going to keep piling in Chicago. Progress Illinois reports, Chicago Takes Out $220 Million Loan For Pension Payments:

The city of Chicago borrowed $220 million for a police and fire pension payment due by the end of the year.

The city took out the loan with a 3 percent interest rate in order to have the pension funds ready by a state-mandated March 1 deadline, officials said Monday.

Chicago Mayor Rahm Emanuel’s 2016 budget included a $588 million property tax hike for police and fire pensions and school construction. Still, the mayor’s spending plan depends on the state for pension funding changes, which have cleared both legislative chambers but have not yet been sent to Republican Gov. Bruce Rauner. The governor has called for the Chicago pension to bill to be included “as part of a larger package of structural reform bills.”

The pension funding changes would give the city more time to make its pension payments, cutting pension costs due this year by $219 million.

With the pension changes in place, the state could return the $220 million it borrowed from its $900 million short-term credit line.

In other pension-related news, the Illinois Supreme Court is expected to hand down a decision Thursday regarding Chicago’s 2014 overhaul of its Municipal and Laborers pension funds.

Last July, a Cook County Judge deemed the city’s pension overhaul unconstitutional. The city appealed the lower court ruling to the Illinois Supreme Court.

The Cook County judge’s ruling against Chicago’s pension measure was guided by a May decision from the Illinois Supreme Court involving a state pension reform law.

The state’s high court struck down the state pension measure on the grounds that it violated the Illinois Constitution’s pension clause, which states that contractual pension benefits cannot be reduced.

Chicago’s pension nightmare has come full circle. As Zero Hedge rightly notes, the countdown for insolvency begins for Chicago’s pensions. This pension problem has been festering for years not just in Chicago but in the entire state of Illinois which has one of the worst funded state plans.

What are my thoughts? I’ve been warning all of you that U.S. public pensions are doomed and the worst ones are at the city and local levels. These unfunded public pension liabilities are going to crush taxpayers through higher property taxes and make it increasingly more difficult for people to afford homes in the United States, not that they are affordable right now.

And while I understand the state’s high court ruling — after all, Chicago mismanaged its pensions for decades, failing to top them up so they it can spend lavishly and foolishly elsewhere — I am increasingly worried that public sector unions fail to understand that unless they agree to adopt a shared risk model and agree to some pension reforms, their city will go the way of Greece and Detroit where the bond market extracted a pound of flesh from public pensions.

In other words, Illinois’ Supreme Court can interpret the law any way it wants, in the end it’s the bond market which will impose drastic cuts to public pensions because already stretched taxpayers aren’t in a position to bail out grossly mismanaged public pensions.

I’ve gone through this already when I discussed New Jersey’s COLA war:

In the U.S., you don’t have such shared risk plans at state pensions, which is why you see massive confrontations on public pensions and terrible solutions to the state pension crisis (like shifting out of defined-benefit into defined-contribution plans).

So who is going to win New Jersey’s COLA war? I don’t know. I feel for a lot of public sector employees getting screwed but the reality is New Jersey and other U.S. states are already screwed when it comes to their pension promise and unions and politicians will need to agree on very difficult cuts to shore up these public pensions. You can only kick the can down the road so far before the chicken comes home to roost.

One thing I do know, however, is that defined-contribution plans are not the solution to America’s ongoing retirement crisis. We can debate COLAs but there’s no debating that bolstering defined-benefit plans is the best way to bolster a country’s retirement system. You just need to get the governance right and introduce a shared-risk model at public pensions like New Brunswick did to tackle its pension deficit.

What is important for all of you to keep in mind when I discuss Chicago’s pension nightmare, U.S. public pensions being doomed, Europe’s pension problem or the $78 trillion global pension disaster is that the global pension crisis is deflationary and it will be with us for a long time.

Let me explain this further. When it comes to unfunded public pensions, either you increase the retirement age and contributions or you cut benefits or you ask taxpayers to bail them out. That last option is political suicide but let’s say politicians are able to ram this through.

What do all these options mean? Less spending for the economy by consumers and less spending on much needed infrastructure projects. And less personal spending on goods and services as well as less government spending on goods, services and infrastructure is very deflationary. Period.

Photo by bitsorf via Flickr CC License