Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; Translation_Entry has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/entry.php on line 14

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_Reader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 12

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_FileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 120

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_StringReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 175

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 221

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedIntFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 236

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; WP_Widget_Factory has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/widgets.php on line 544

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/load.php on line 585

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712 Defined Contribution | Pension360 | Page 2 Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

The country’s top universities have been hit with an onslaught of lawsuits the last 30 days over excessive fees related to the schools’ 401(k) plans.

At the heart of the trend is an interesting disparity, writes Stephen Mihm for Bloomberg:

On one hand, 401(k)s and their ilk would seem to shift the burden of making investment decisions onto employees, limiting the fiduciary duty of the employer. On the other, the regulatory apparatus that applies to 401(k)s derives from ERISA, whose ideas of trusts and equity law imposes some serious duties for sponsors of defined-contribution plans — ideas at odds with the notion that individuals have to take responsibility for their investment decisions.

This disparity informs the lawsuits over excessive fees. Schlichter is pushing courts to recognize that 401(k) and 403(b) sponsors are trustees with grave responsibilities toward their plan participants. Implicit in this line of argument is the idea employers can’t simply shove some investment brochures in front of their employees and let them choose. Rather, the employer needs to get the absolute best possible deal for their employees — the lowest fees for example — and select investments that yield an average or above-average rate of return (index funds are the obvious choice).

And in the past few years, courts have started to agree, counter to the ethos that informed the creation of the 401(k). In May, the Supreme Court overturned a lower-court ruling that would have let defined-contribution sponsors off the hook for monitoring the quality of the investment choices on an ongoing basis. In a rare unanimous opinion, the court declared that “under trust law, a trustee has a continuing duty to monitor trust investments and remove imprudent ones.”

This may well be true. But the ambiguity remains. We are caught between two very different philosophies of individual responsibility. On the one hand, workers are still expected to navigate the confusing world of retirement investments on their own. But much of the law governing those investments relieves employees of that responsibility.

Which is it? It may be time for Congress to wade into this mess and clarify, once and for all, the respective duties of employer and employee on the vexed question of retirement benefits.

A recent study of large versus small 401(k) plans shows that small plans perform as well – or better – than their larger peers. Judy Diamond Associates, a sister firm of BenefitsPro, culled data from about 52 million participants with $4 trillion in assets.

The study, about which more information is available here, compared plan size, industry, participate rates, levels of contributions, account balances, and returns.

After aggregating the results for all industries, the smallest plans, with one to 10 participants, posted a score of 62, the highest among eight levels of plan size…. By comparison, the largest plans, with 5,000 or more participants, which accounted for 1,793 total plans, posted an average score of 57, the third highest among the eight segments.

Digging the in the details, the study uncovered the following nuggets, via BenefitsPro:

More than 178,000 plans fall into [the small] size group, more than all other segments. The average account balance was $75,735, and participation rates averaged 89 percent, both tops by plan size. Average employee and employer contributions–$4,850 and $1,979 respectively—were also more than all other size segments.

The average account balance for the largest plans was $54,513, and the average participation rate was 73 percent. Employee and employer contributions averaged $3,067 and $1,424, respectively.

The rule that launched a thousand memos – the DOL fiduciary rule – is the subject of an excellent cheat sheet published by PlanSponsor. Read the whole thing here.

Among some of the helpful highlights:

– The rule redefines the term “fiduciary” as it applies to “investment advice” from advisers and retirement service providers. As a result, many service providers, particularly those who service participants, will become fiduciaries for either the first time or with respect to more of their activities. Under the old rules, some advisers (and service providers) were not subject to the fiduciary duties imposed by ERISA, the law governing retirement plans, or similar rules applicable to IRAs. Under the final rule, any individual receiving compensation for making investment recommendations that are individualized or specifically directed to a particular plan sponsor or fiduciary running a retirement plan (e.g., an employer with a retirement plan), plan participant, or IRA owner for consideration in making a retirement investment decision could be a fiduciary subject to the new rules (unless they satisfy certain exceptions from the rules).

– Many of the educational activities we currently have today will still be permitted, so that plan fiduciaries, sponsors and the entities who work with them will not risk becoming subject to the new fiduciary standard for advisers merely due to the fact that such education is provided. There was some concern that certain types of education that had previously been permitted—naming specific investment options in asset allocation models, for example—would no longer be permitted, but the final rule dropped such restrictions for plans (but not IRAs)—but there are certain requirements that apply.

– As for its effect on retirement plan fiduciaries and sponsors, there will be little direct effect, but those who advise retirement plan participants, and the firms who employ such individuals, are likely to be affected. Further, if you deal with more complex investments (if you are a larger plan), some of your investment structures could be impacted. For example, if your recordkeeper employs individuals who provide advisory services to participants, those recordkeepers could be affected.

As for 403(b) plans:

403(b) plans that are not subject to ERISA (i.e. governmental plans, church plans, and elective deferral-only plans utilizing the 29 CFR 2510.3-2(f) safe harbor) are not subject to the final fiduciary rule at all. However, rollover IRAs from these plans could be caught in these rules.

A federal judge recently slapped down City National Corporation for ERISA violations that allegedly arose from overcharges from in-house plan management.

When City National Corporation administered its employee retirement plan, it took fees from the plan and lumps from the court.

U.S. District Court Senior Judge Terry J. Hatter, Jr. found that City National and its subsidiaries violated ERISA by engaging in years of self-dealing. The court ordered the company to retain an independent, third-party fiduciary to assist in accounting for all compensation it received from the plan, in the form of mutual fund revenue from 2006 through 2012, plus lost opportunity costs, to correct its numerous ERISA violations. The department estimates this amount to exceed $6 million.

In its findings, the court agreed with the DOL City National failed to meet its duties as a plan fiduciary by accepting fees from the plan without any review or independent investigation into whether fees were reasonable; not reimbursing the plan upon discovering that it was charging unreasonably high fees; and not tracking any direct expenses for the plan.

A bit of background on the suit, from a 2015 PlanSponsorpiece:

The Department of Labor (DOL) says the fiduciaries of the City National Corp. Profit Sharing Plan caused the plan to lose more than $4 million by engaging in self-dealing and conflicted transactions that enriched themselves and their employer. According to a complaint filed in the U.S. District Court for the Central District of California Western Division, the self-dealing and conflicted transactions involving plan assets resulted in excessive fees going to City National Bank and its affiliates.

“All of this could have been avoided if the fiduciaries had simply reimbursed themselves in accordance with the law,” she [Crisanta Johnson, the Los Angeles regional director for the DOL’s Employee Benefits Security Administration (EBSA)] notes. “Instead, they created a payment scheme that drained plan assets.”

According to a recent poll by Gallup and Wells Fargo, most investors with a 401(k) plan are upbeat about their plan and their savings. Over 90 percent of investors, according to the study, are satisfied with the 401(k) plan for their retirement. Vladimir Putin couldn’t even stuff a ballot box that would generate this level of satisfaction.

Gallup announced the results of the survey, conducted with Wells Fargo, stating:

These findings are from the latest Wells Fargo/Gallup Investor and Retirement Optimism Index survey, conducted Jan. 29-Feb. 7, 2016, among 1,012 U.S. investors. Approximately 40% of U.S. adults meet the survey’s criteria as investors; these criteria involve having $10,000 or more invested in stocks, bonds or mutual funds, either in an investment or retirement account. Seven in 10 employed investors say their current employer offers a 401(k) — and of these, 88% say they participate.

Some generational differences among attitudes included the following:

…age-related differences in preference for receiving allocation advice underscore generational gaps in the use of digital versus traditional resources:

– A majority of investors younger than 50 (58%) versus a third of those aged 50 and older (35%) use online investment calculators.

– Older investors are twice as likely as those aged 18 to 49 to consult a financial call center (21% vs. 10%, respectively).

– Younger investors (50%) are also much more likely than older investors (30%) to turn to family or friends for allocation advice.

Looks like a kind of two parallel universes – some surveys saying that investors are terrified of poverty in retirement, but this one showing that the future is so bright they need sunglasses.

Within days after the new DOL fiduciary rule, Republic leaders in the Senate launched a resolution attempting to block the rules. Three GOP senators announced that the new rules would raise the bar for providing advice so high that small account holders would be left behind.

[U.S. Senators] Isakson, Alexander and Enzi today filed a resolution of disapproval under the Congressional Review Act to reject the administration’s new so-called “Retirement Advice Gag Rule.”

“I have worked to fight the implementation of this harmful rule since it was first proposed and promised to do all I could to overturn it before it can harm Georgia families. The introduction of this resolution is the next step in the battle,” Isakson, who is chairman of the Senate Health, Education, Labor and Pensions Subcommittee on Employment and Workplace Safety, said in a statement. “Like so many of this administration’s decisions, their new fiduciary rule harms the very individuals it seeks to protect and prevents those hardworking Americans who are trying to plan for retirement from having the opportunity to access retirement advice.

Georgia Senator Johnny Isakson is the chairman of the committee responsible for pensions and labor. He has already launched a salvo of proposed laws, including sponsoring or co-sponsoring the following, as recorded by 401k Specialist:

…the Affordable Retirement Advice Protection Act, which would require a vote by Congress before any final rule by the administration went into effect;

…the Retail Investor Protection Act, which would prohibit the Department of Labor from issuing its rule until the U.S. Securities and Exchange Commission has issued a final rule relating to standards of conduct for brokers and dealers and has satisfied additional reporting requirements; and

…the Strengthening Access to Valuable Education and Retirement Support (SAVERS) Act, which seeks to block the Department of Labor’s “harmful” fiduciary rule and provide a viable alternative …

The new fiduciary rule could trigger a slug-fest among consultants. A recent panel of broker dealers and registered investment advisors mused that the climatic changes of fiduciary responsibility could lead to the extinction of some of the less adaptable “generalist” advisors.

“We think there will be a lot of plans in play,” said J. Fielding Miller, chief executive of CAPTRUST Financial Advisors. “This is kind of like prime hunting season for our industry.”

As opposed to retirement “specialist” advisers, who derive most of their business from the defined-contribution-plan market, generalists, or “dabblers,” tend to derive most of their business through wealth management and may have only a handful of retirement plan business.

The Department of Labor’s new rule, which raises investment advice standard in retirement accounts, puts pressure on the dabblers to reconsider if they want to be in the retirement business, Mr. Miller said Tuesday morning at the National Association of Plan Advisors’ 15th annual 401(k) summit in Nashville.

INCREASED LITIGATION RISK. Several smaller firms will struggle to comply with the new rule, and the additional risk of private litigation action will “scare” some providers to turn away from the retirement business, according to Edward O’Connor, managing director of retirement strategy at Morgan Stanley.

Rolling Over the Rollover Shops

Additionally, Brokers that made lots of money on plan rollovers may be in for a rough ride.

The panelists also discussed the impact of the rule on rollover business, saying there will likely be less rollovers as fewer brokers and advisers recommend rollovers, and more participants will keep their money in-plan as a result.

Retirement assets staying in plan will be a boon to plan providers, the panelists said.

“This is definitely a tailwind for them,” according to Mr. Chetney. “There will be less ‘shysters’ trying to take money out on an unreasonable basis.”

Those firms for which rollovers represent a primary part of their economic model will have to rethink that business model, according to Mr. O’Connor. “Rollovers will become a less important part of anyone’s business model,” he said.

Among the many, many, many aftershocks of the new fiduciary rules is the application of the new Best Interest Contract Exemption to fixed indexed annuities. The Department of Labor produces millions of pages of rulings and rules, but only just determined that fixed indexed annuities were complicated.

The DOL likened FIAs to variable annuities in their cost and complexity. “Given the risks and complexities of these investments, the Department has determined that indexed annuities are appropriately subject to the same protective conditions of the Best Interest Contract Exemption that apply to variable annuities,” the final BICE text said. FIAs have gotten even more complex in recent years, especially with the introduction of hard-to-value “hybrid” indices that allow issuers to offer supposedly “uncapped” gains even though the gains of FIAs are by design strictly limited. But it’s not clear if this trend influenced the DOL.… The DOL said that it put FIAs under BICE because they’re so complicated and hard to understand. “Retirement Investors are acutely dependent on sound advice that is untainted by the conflicts of interest posed by Advisers’ incentives to secure the annuity purchase, which can be quite substantial.

It may be a case that one man’s level playing field is another man’s valley of death. Says Retirement Income Journal:

In addition, the DOL said that it wanted to create a “level playing field” for FIAs and VAs, and to avoid “a regulatory incentive to preferentially recommend indexed annuities,” as the original proposal could have created. But, arguably, the DOL has chosen to provide a disincentive to recommend VAs and FIAs, and gives an implied encouragement to the sale of fixed deferred and fixed income annuities, including single premium immediate annuities, deferred income annuities, and qualified longevity annuity contracts.

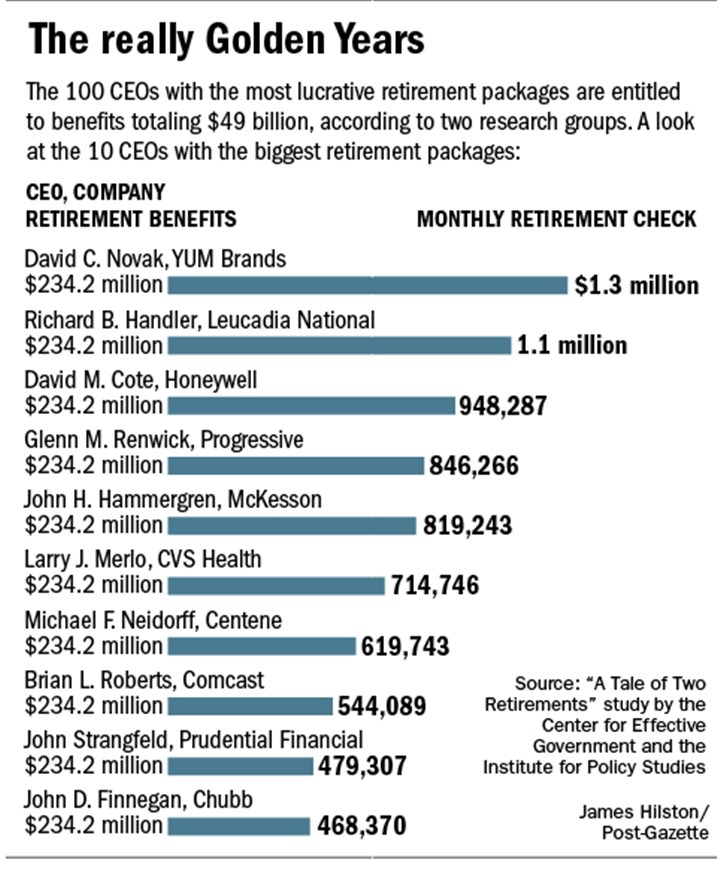

The CEOs of the largest companies in America have accumulated retirement savings – through pension benefits, 401k accounts and more – that equal the savings of 50 million Americans, according to a new study.

The study, carried out by the Center for Effective Government and the Institute for Policy Studies, analyzed the retirement packages of 100 CEOs by looking at compensation disclosures filed with the SEC, as well as Federal Reserve data.

Based on their math, the 100 CEOs are entitled to $4.9 billion in retirement benefits. That’s an average of $49.3 million each, or enough to provide a monthly check of $277,686 for the rest of their lives. (The paycheck estimate is based on an annuity calculator at www.immediateannuities.com.)

“The CEO-worker retirement divide turns our country’s already extreme income divide into an even wider economic chasm,” the report states.

The 10 CEOs with the biggest retirement accounts are all white males whose retirement benefits total $1.4 billion. The 10 female CEOs with the most lucrative retirement benefits are only entitled to $280 million collectively, while the total for the 10 largest CEOs of color is $196 million.

[…]

The two groups have some ideas for closing the retirement pay gap, including ending the ability of executives to contribute as much as they want to tax-deferred compensation plans. The plans work like 401(k) accounts and include money contributed by the executive and their company.

They’d also like to eliminate tax deductions that companies enjoy for pension and retirement costs — if the companies have frozen worker pension plans, closed pension plans to new hires or have pension plans that are not at least 90 percent funded.

In this 45 minute video interview Leo Kolivakis discusses the importance of a good pension system with strong governance being critical in insuring the average persons retirement security. Pension liabilities are going up while bond yields are going lower which is going to create a huge amount of stress on pensions!

Contributory Pensions and 401Ks have proven to be a failure compared to Defined Benefits programs. History will eventually show that the transition from Defined Benefits to Contributory Benefits was in fact is detrimental to the global economy.

Structural Issues

Leo Kolivakis believes we have entered a period of long deflation due to six major structural issues:

The global jobs crisis

Aging demographics

The global pension crisis

Rising inequality

Technological Advances

High and unsustainable debt all over the world

Each of these structural factors is significantly contributing to global deflation. Together they are a domino effect, exacerbating deflationary headwinds in the world. They are causing rates to remain ultra low and will continue to for years to come.

I embedded our conversation below and thank Gordon Long for giving me another opportunity to discuss pensions, rising inequality and how it’s impacting aggregate demand.

Let me give you a little background on all this. For years, I’ve been arguing to prepare for global deflation. I still see a deflation tsunami coming our way but there is a huge battle going on as central banks desperately try to fight it off.

Right now, central banks are the only game in town and this is why we’re seeing negative interest rate policies springing up all over the world, all part of the new negative normal. Again, central banks are desperately trying to stoke inflation expectations to thwart deflation because once it becomes entrenched, it will be here for a very long period.

Negative bond yields and ultra low bond yields for years present serious challenges to individuals trying to retire on a fixed income and pensions trying to make their actuarial target rate of return. In effect, people will need to work longer to be able to retire and pensions will need to take increasingly more risk in private markets and hedge funds to make their bogey.

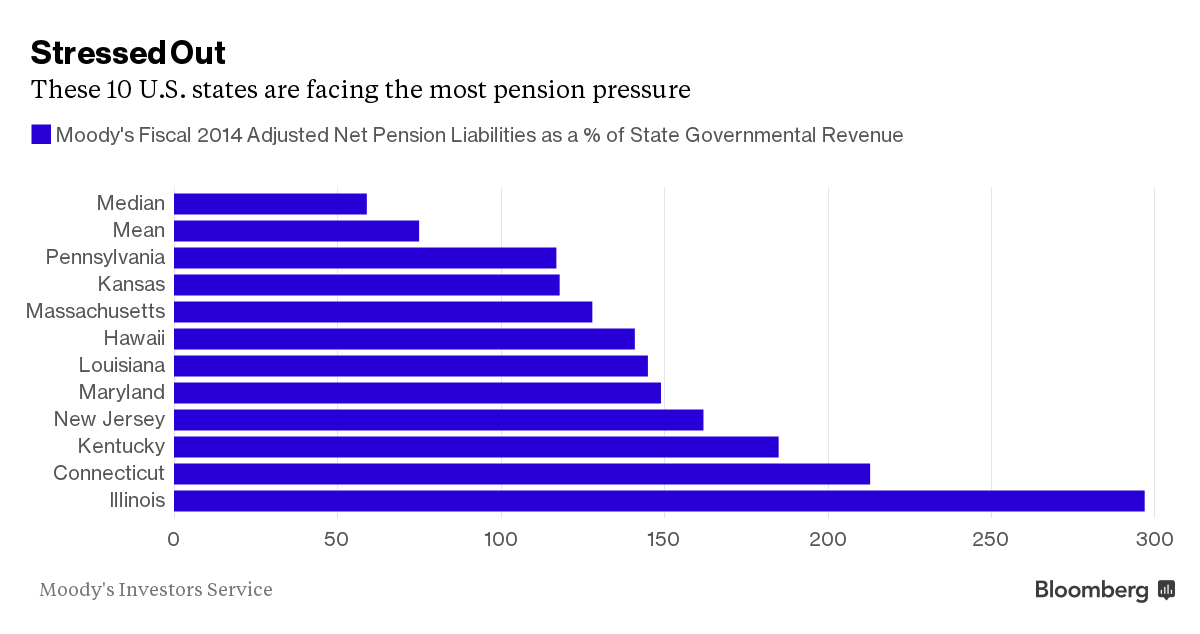

Meanwhile, many state pensions are also at risk. Moody’s released some interesting data last month regarding the adjusted net pension liabilities of U.S. states. Bloomberg then spun that data into the chart below (click on image; h/t Pension 360):

As those of you who follow the CalPERS soap opera may recall, California Governor Jerry Brown pushed for the giant pension fund CalPERS to lower its assumed investment return from 7.5% to 6.5%. Given that the world is headed towards deflation and that CalPERS earned only 2.4% for the fiscal year ended June 30, 2015, Brown’s request seemed entirely reasonable. Instead, the board approved a staff proposal to move to the 6.5% target over 10 years.

One of the things that is perverse about pension accounting is that the convention is that the liabilities, that is, what the pension fund expects to pay out over time, are discounted at the same rate as the assumed returns. However, for a government pension plan, where taxpayers are on the hook for any shortfalls, the risk of CalPERS beneficiaries getting their money is not the risk measured in terms of what CalPERS projects in terms of future employee contributions, expected returns, and expected payouts; it’s ultimately California state risk, which means the liabilities should be discounted at California’s long term borrowing rate. With California rated S&P AA3, Moody’s Aa-, and 20 year AA muni yields 2.75% and A at 3%, no matter how you look at it, the discount rate on the liability side is indefensibly high.

This matters on the estimation of liabilities because the lower the discount rate, the larger the amount (in current terms) that has to be paid out. Remember, this is the mirror image of “inflation can help bail out underwater borrowers” scenario. High discount rates erode the value of future commitments; low ones increase them. This is why we have been warning that ZIP and QE, which explicitly sets out to lower long-term interest rates, is a death sentence to long-term investors like life insurers and pension funds. And investors like CalPERS are trying to finesse that problem by continuing to pretend that they can earn a higher rate of return than is attainable without taking batshit crazy risks.

The fact that our members are living longer is a sobering reminder that we have a growing obligation to provide for their pensions. Just a decade ago the ratio of active workers to retirees was over 2 to 1. That ratio is now 1.3 workers to every retiree, and we pay out more in benefits than we receive in contributions.

In response, our Board approved a policy designed to reduce the discount rate, our 7.5 percent assumed rate of return on investments, over time. The result will help pay down the pension fund’s unfunded liability and reduce risk and volatility in the fund.

Huh? This is utterly backwards. What will reduce CalPERS’ unfunded liability is higher contributions or higher earnings. A lower discount rate, while a reflection of current reality, exposes that it will be harder, not easier, to meet this objective.

The worst is that given the level of finance acumen I’ve seen after watching hours of Investment Committee hearings is that the odds are high that this is not an obfuscation misfire but evidence of an utter lack of understanding of finance basics. And worse is that CalPERS staff, which had to have reviewed this text, didn’t see fit to correct this glaring error. Do they also not get it or did they assume that beneficiaries were too clueless to catch it?

At the local and municipal level, the problems are even worse. The Financial Times just published an article on Philadelphia’s $5.7 billion ‘quiet crisis’ and these problems are going on all over U.S. where city, local and municipal pensions have been mismanaged for decades.

The central problem at U.S. public pensions remains governance, or more precisely, lack of proper governance. I wrote a comment for the New York Times back in 2013 discussing the need for independent, qualified investment boards that operate at arms-length from the government.

Instead, you have way too much political interference, and a bunch of underpaid public pension fund managers that are outsourcing investments to external asset managers, including hedge funds getting crushed and private equity funds that are way past their golden age.

[Interestingly, Bloomberg reports that two years after buying it, Carlyle Group LP will shut down its hedge fund-of-funds manager, Diversified Global Asset Management or DGAM of Toronto.]

And even though there are efforts to reduce fees of hedge funds and private equity funds, the sad truth is that quantitative easing, ultra low rates, negative rates and more volatility in public markets will force public pensions to increase their allocations to these alternative investment funds that have become nothing more than glorified asset gathers.

This is all part of the financialization of our economies. In my discussion with Gordon below, I recommend a book I’m currently reading by FT columnist and British economist John Kay, Other People’s Money. You can read the introduction here.

But there is something else out there that a lot of authors examining inequality are not particularly aware of. Public pensions taking increasing risks in alternative asset classes are enriching a new class of hedge fund and private equity billionaires which then use their extraordinary wealth to fund Super PACs against progressive candidates like Bernie Sanders (Bernie should rework Bill Clinton’s old campaign slogan and turn it into “It’s about inequality, stupid”).

Rising and perverse inequality is a huge problem and it’s deflationary. In his recent TED talk, Capitalism Will Eat Democracy, Greece’s now defunct former Minister of Finance Yanis Varoufakis talks about the twin peaks: the global glut of savings from billionaires and corporations hoarding cash and the debt crises that many nations face.

In effect, he’s right, this mismatch is one reason why the structural unemployment rate of many developed nations remains stubbornly high. This is part of the global jobs crisis and pension crisis which is related to rising inequality. Of course, Varoufakis and Tsipras lacked the courage to implement real and much needed reforms in Greece which is why that country remains a basket case (after Brexit, Grexit will resurface this summer or later this year).

So what are the solutions to this? I talk about some solutions with Gordon, including bolstering well-governed defined-benefit plans, enhancing Social Security and modelling after the Canada Pension Plan Investment Board, introducing risk sharing in state plans, amalgamating local and municipal plans at the state level. I forgot to mention that we basically need to go Dutch on pensions all around the world.

I continue to defend well-governed defined-benefit plans and believe they are part of the solution to addressing rising inequality which threatens aggregate demand. The benefits of DB plans are greatly under-appreciated by everyone, including policymakers who lack a comprehensive vision of what the real problems are and how we can address them.

I also discussed the need to spend on infrastructure and how pensions which need yield can help cash strapped governments on revitalizing Canada’s and America’s crumbling infrastructure.

Below, take the time to listen to my conversation. As you can tell, I’m not really a “Skyper” and make a few mistakes here and there but the main message is there and I thank Gordon Long for giving me an opportunity to speak with him on these important issues which politicians tend to ignore.

I also embedded another recent interview I liked from the Financial Repression Authority, featuring another Greek, John Charalambakis, the Managing Director of Black Summit Financial Group, discussing risk mitigation and capital preservation. I don’t agree with everything he says but he’s extremely intelligent and this is a great interview.

Listen to us Greeks, we know a thing or two about where the world is heading. In all seriousness, I thank Gordon for this opportunity to speak on these issues and hope we can continue the conversation in the future. I’d also like to see other experts debate pension policies on his show in the future and forwarded him a list of people to talk with on this important and often ignored topic.

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712