Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; Translation_Entry has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/entry.php on line 14

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_Reader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 12

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_FileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 120

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_StringReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 175

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 221

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedIntFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 236

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; WP_Widget_Factory has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/widgets.php on line 544

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/load.php on line 585

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712 Home | Pension360 | Page 108 Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Chicago Public Schools (CPS) has for weeks been publicly questioning its financial ability to make its full pension payment ($634 million) by the June 30 deadline.

CPS, and Mayor Emanuel, have both stated that the payment couldn’t be made in full without big cuts in classrooms.

CPS recently turned to the state House for an extended deadline; however, House lawmakers this week were unable to agree on whether to let CPS make a late payment.

Illinois Democrats’ cross-party dispute in the state Capitol turned internal Tuesday when the majority party in the House failed to approve giving cash-strapped Chicago Public Schools a six-week reprieve on making a $634 million pension contribution.

Even with support from Republicans on a plan school officials said would avert classroom-spending cuts, the measure on delaying the pension payment failed 53-46, falling short of the 71 necessary.

[…]

House Majority Leader Barbara Flynn Currie of Chicago argued that her measure simply bought more time, allowing the district to collect summertime tax and state-aid receipts while working on an interim or permanent fix.

“We need our leaders to come together so that we have enough time to reach a solution,” interim schools CEO Jesse Ruiz said.

Republican Leader Jim Durkin of Western Springs collected 16 GOP votes requested for the measure, saying his party was ready to step up. Not everyone on his side was convinced.

“I don’t know what 40 days gets you,” said Rep. Dwight Kay, a Glen Carbon Republican, “and what I hoped I would have heard today is a strategic plan.”

Some Chicago Democrats did give the thumbs-down. Rep. Frances Ann Hurley said she opposed any “pension holiday” that puts off a payment, even for six weeks.

Democrats are pushing for another vote, but that can’t happen until early next week – June 30, the same day the pension payment is due.

Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

John Mauldin revisited the topic of U.S. public pensions in his latest comment: Live and Let Die:

When you were young and your heart was an open book

You used to say live and let live…

But if this ever-changing world in which we’re living

Makes you give in and cry… Say live and let die.

– Paul McCartney, the Bond movie theme, performed by Wings

I am not sure if my heart was ever that much of an open book, but I like to think I’m still relatively young. Nevertheless, I must admit that sometimes I want to “give in and cry.” This is especially so when I look at our nation’s public pension funds.

It’s not as if no one saw the problem coming. Experts, including your humble analyst, have been harping on it for decades. Politicians at all levels of government knew very well that a train wreck was inevitable and still did nothing. In some places, like Illinois, the politicians actually did something worse than nothing: they bought votes with promises of future benefits. Even worse, many states had their pension funds sell bonds, thinking they would be able to profit on the difference. Then along came the Great Recession. Oops. Stellar timing.

Now the future is here. Where are the benefits?

In this week’s letter we’re going to return to the worsening problem of public pensions. I offer an analogy between what is happening in Greece today and what will soon happen in Illinois. There are no easy solutions when you kick the can down the road, as politicians are going to find out.

This week we will look with fresh eyes at an old problem: US pension funds, both public and private, are underfunded; and the situation is getting worse. And the US taxpayer is going to get to fund the difference. The recent slew of data on pension funds suggests that little is being done to correct the huge and mounting problems I have written about for years. Even the recent market upturns of the past few years have not been as big a help as they should have been.

I doubt anyone would have noticed had I led with that same paragraph today. Every word is just as true now as it was then.

Pensions are still underfunded.

The situation is still generally getting worse (with some exceptions, thankfully).

Taxpayers are still going to fund the difference.

Recent market upturns have helped some, but not as much as you might think.

I’ve visited the topic of pensions repeatedly over the years. Some of my headlines are darkly amusing in hindsight:

Why have we not hit the wall yet? In that 2005 letter, I wrote this, referring to corporate pensions:

Let’s look at a typical 60% stock, 40% bond asset allocation mix. Let’s generously assume you can make 5% annualized on your 40% bond portfolio allocation in the next ten years. That means to get your 8% (assuming a lower average target) you must get 10% on your stock portfolio. Now, about 2% of that can come from dividends. That means the rest must come from capital appreciation.

Hello, Dow 22,000 in 2015. Care to make that bet with me? But pension plan managers are doing precisely that.

Here we are in 2015, and the Dow is at 18,115, not 22,000. The 10-year average annual total return (including dividends) in the SPDR Dow Jones Industrial Average ETF (DIA) was 7.99% as of 3/31/15. Stocks lagged about 2% per year behind what I thought pensions needed to see.

If stock performance didn’t bail out pensions, what about bonds? Was assuming a 5% annualized return back in 2005 a good move?

Actually, it was. The iShares Core US Aggregate Bond ETF (AGG) had a 4.77% 10-year average annual total return through 3/31/15. If you focused just on government bonds with the iShares 20+ Year Treasury Bond ETF (TLT), you had an average annual total return of 7.93%. However, you have to realize that the majority of those returns were capital gains and not actual interest income. Since rates really can’t drop all that much from here, and we are in a low-interest-rate environment for the foreseeable future, those types of returns are not going to happen in the next 10 years.

So, a balanced pension fund would have done better than expected in bonds, almost enough to offset the worse-than-expected return in stocks. That bought some time, assuming that the politicians provided the necessary contributions. As we will see, in many states they did not, so things have gotten decidedly worse even as the market has risen.

It is not the case that all pension funds stayed balanced for the whole decade. We had some severe bumps in 2008-2009. More than a few pension managers tweaked their strategies in response. Adding alternative investments to the mix has been a popular enhancement. The degree to which they enhanced your performance depends almost entirely on the alternative managers you picked. And if you were picking by means of hindsight, relying on past performance, you probably didn’t pick good managers for the recent environment.

So, to generalize, most pensions had “OK” investment returns in the last ten years but not enough to catch up without increasing contributions from governments, which in the main did not happen. However, those returns at least kept them on an even keel. Until the next recession, that is. But the modest performance managers eked out most certainly did not give legislators the luxury of promising even higher benefits to their retirees. But – you guessed it – many politicians made those promises anyway.

Spending Money You Don’t Have on Promises You Can’t Keep

Unless you are a national government and can print your own currency, and with enough effective means to discourage would-be foreclosure, you can run a spending deficit for only so long. Greece is presently learning this the hard way.

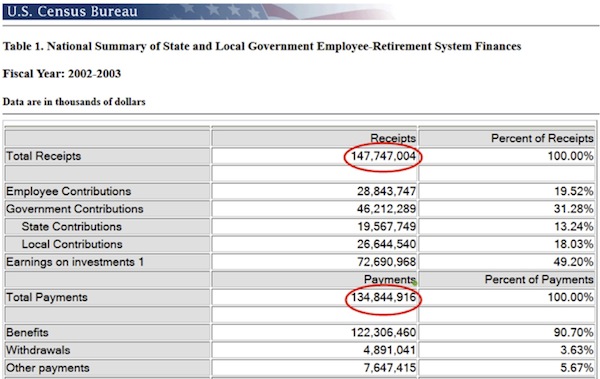

State and local governments in the United States must, by law (with the rare exception), somehow balance their budgets. So must their pension plans. As of ten years ago, they were generally succeeding. Here is Census Bureau data for FY 2002-2003 (click on image):

State and local pensions had total receipts of $147.7 billion that year and total payments of $134.8 billion. This is aggregate data, so any given plan might have done better or worse. Still, the overall picture doesn’t appear to be bad. Why was I so worried?

As my mother would often remind me, appearances can be deceiving. I was worried because we knew the next tens of millions of Baby Boomers would soon start retiring, driving payment obligations sharply higher. Simply doing the math told us that even given the robust assumptions that pension funds were making, many pensions were going to be massively underfunded in the future. And if you made more realistic assumptions, there were numerous pension plans that were going to be in serious trouble.

Notice too that about half the total receipts came from earnings on investments instead of employee or government contributions. That’s important, as any portfolio manager knows, because you can’t spend an entire year’s earnings if you also need to accrue long-term capital gains. You have to reinvest. In fact, the bulk of planned payments in 30 years don’t come from current contributions but come instead from compounding returns on current portfolios. If you are using those current portfolios to pay benefits today, the money clearly will not be there. And every dollar you pay out today that should be used for investing means that eight dollars will not be there 30 years in the future. And that’s assuming you get the better-than-7% returns everyone is projecting they will make.

Now, let’s fast-forward ten years from 2003. The Census Bureau changed its data format, but I believe this is a comparable data set for 2013 (click on image).

Apparently, the Census Bureau also decided to pull investment earnings out of the contribution subtotal. Total 2013 contributions were $153.8 billion. Total payments were up to $260.8 billion in 2013, thanks to my fellow Baby Boomers. That would seem to leave a big deficit. It didn’t, because the plans also had $383 billion in investment earnings. About $107 billion of that went immediately to pay retirees.

Again, the problem with these numbers is that there is no guarantee investment earnings will be this high in any given year. That number could even be negative, as it has been at times in the past. Then what?

In 2013, CalPERS managed $230 billion. The fund calculates that it is underfunded by $80 billion. The management arrives at this number by assuming they will make 7.5% (which they only recently dropped from 7.75%). In 2009, they estimated that the fund was underfunded by only $49 billion. That means they missed their target by $30 billion in a roaring bull market.

In a December 2011 study, former Democratic assemblyman Joe Nation, a public finance expert at Stanford University, estimated that CalPERS’s long-term pension debt is a sizable $170 billion if CalPERS achieves an average annual investment return of 6.2 percent in years to come. If the return is just 4.5 percent annually – a rate close to what more conservative private pensions often shoot for – the fund’s long-term liability rises to a forbidding $290 billion. (Steven Malanga)

Last year I was in Norway. It has a sovereign fund that is larger than CalPERS but that benefits from some of the best management in the world. My talks with people involved in the fund and those who are very familiar with it suggest that they would be very happy to get 4% over the next 5–10 years. CalPERS ranks in the bottom 1% of all pension fund managers. Given all the resources they have, they are spectacularly bad at managing money. And when I say “they,” I mean the board of directors.

Malanga points out that CalPERS is a wholly owned subsidiary of the government-employee trade unions that control the board. He painstakingly chronicles the extent to which the unions dictate policy and investment decisions, leaving the professional management shackled.

And this is the issue. Nearly every public pension plan dramatically overstates its future potential income and returns, which makes the unfunded liabilities look better than they actually are. In coming weeks we’re going to be exploring in depth why the next decade is going to provide, on average, lower returns for pension funds and individual investors who are mired in traditional forms of investing.

In May, Moody’s downgraded Chicago bonds to junk status. One of their examiners pointedly asked, why is Chicago any different in Puerto Rico? Why indeed? My friend Mish Shedlock believes that Chicago is not alone in its misery. He thinks at least seven Illinois cities are in serious and immediate trouble. Detroit was not the last major city that will have to default on its obligations.

Sidebar: I know that many people invest in municipal bonds. Many of these, in fact most, are solid investments. Then there are some real dogs that are going to be extremely problematic. You need to look at, or have someone who is knowledgeable look at, bonds in your portfolios. I’m sure there are some properly run cities in Illinois, but I think I would throw the baby out with the bathwater there. There is no telling what politicians are going to require taxpayers in cities to do. It wouldn’t be the first time they took from the have-cities and give to the have-nots. Sadly, to my great chagrin and embarrassment, we did exactly that in Texas when we were forced to do so by judges.

State and local pensions, in aggregate, are running severely negative present cash flow. If we get a bad market year (and we will), they will have to dip into their principal, cut benefits, turn to taxpayers, or borrow cash. Local governments can also file bankruptcy; states can’t, except in theory. We may see that theory tested in the next 10 years.

None of those choices are good. If pensions have to sell into a falling market, cash flow will fall even more. Such a scenario probably means the economy is weak and tax revenues are falling. That makes raising taxes and issuing bonds problematic.

Cutting benefits might be the only choice. But guess what: in many states, cutting benefits to current retirees is unconstitutional. Let’s look at the dilemma this poses for one state.

Hello, Illinois, Anyone Home?

Courtesy of Bloomberg, here are the ten most underfunded state pension plans as of 2013, the latest available data. Notice how poorly – one could almost use the word disastrously – these bottom 10 states have performed in what has essentially been a bull market for the last five years. Their funding ratios have dropped anywhere from 15% to 25%. And that was in good times! (click on image)

Illinois has had the questionable honor of leading this list every year since 2008. For whatever reason, the state seems to be generous to its retired workers but reluctant to set aside enough money to actually pay for this generosity.

The situation is Illinois is unique enough to make Salman Khan use it as an example in his Khan Academy civics curriculum. I highly recommend watching his 7-minute presentation. He explains very clearly how Illinois arrived at this point.

Now, in their defense, the Illinois legislature tried to avoid the train wreck. In December 2013 they passed a package of reform measures after what sounds like an ugly fight. Here is how the a described it at the time. (This attempt at reform bears review because what happened in Illinois may be coming to a state near you unless adequate action is taken immediately.)

The top leaders of both legislative houses, Democrats and Republicans, had cobbled together the bill and pushed strenuously for its passage, supported by the state Chamber of Commerce and the Illinois Farm Bureau. Union leaders and some Democratic lawmakers opposed it, just as strenuously, arguing that the bill fell too harshly on state workers who had paid into their pension plans over the years with the understanding that the benefits would be there when they retired. Some Republicans also opposed the bill, saying it did not trim enough to solve the state’s pension troubles.

“Today, we have won,” Gov. Pat Quinn, who made overhauling the pension system a focus of his administration, said in a statement after the vote. “This landmark legislation is a bipartisan solution that squarely addresses the most difficult fiscal issue Illinois has ever confronted.” He is expected to sign the legislation on Wednesday.

We Are One Illinois, a coalition of labor unions that opposed the bill, issued a very different assessment. “This is no victory for Illinois,” it said in a statement, “but a dark day for its citizens and public servants.”

The battle now turns to the courts, where union leaders have promised to take the legislation. Some opponents have asserted that it violates the State Constitution by illegally lowering pension benefits.

The plan’s architects said the measures would generate $90 billion to $100 billion in savings by curtailing cost-of-living increases for retirees, offering an optional 401(k) plan for those willing to leave the pension system, capping the salary level used to calculate pension benefits, and raising the retirement age for younger workers, in some cases by five years. In exchange, workers were to see their pension contributions drop by 1 percent. The measure also calls for the state to increase payments into the system by $60 billion to $70 billion.

As expected, the battle then moved into court. On May 8 of this year, the Illinois Supreme Court ruled unanimously that the changes violated the state constitution. That leaves Illinois back where it started.

In their written opinion, the seven justices showed zero sympathy for the state’s legislative branch. I thought this was outcome actually a bit refreshing. More from the NYT:

The court’s decision on Friday had long been predicted by legal experts here. In a 38-page written opinion, the justices sounded an unsympathetic note to suggestions that the state was forced to take drastic action when faced with what amounted to a financial emergency. The court noted that state lawmakers had, over decades, delayed or shorted what they should have contributed into the system, which covers state workers, teachers outside Chicago and others.

The General Assembly may find itself in crisis, but it is a crisis which other public pension systems managed to avoid,” Justice Karmeier wrote. He added later, “It is a crisis for which the General Assembly itself is largely responsible.”

Anyone who has raised teenagers will recognize this tone. Faced with the consequences of failing to plan ahead, they look to Mom and Dad for a bailout. The Illinois justices put the onus back where it should have been all along.

(I’ll quibble with Justice Karmeier on one point. In fact, many other public pension systems haven’t managed to avoid this problem. In many cases, politicians and other states have elected to do the same thing that Illinois did and have simply postponed the inevitable. Most of them will find themselves in the same sort of crisis at some point.)

Illinois must now go to Plan B, which is not going to be much easier. Governor Bruce Rauner wants to amend the state constitution to allow pension reforms. Passing such a bill will take a three-fifths majority of both the state house and senate, and then a minimum six-month wait before it can go to voters in the next general election. Then it has to get 60% in favor.

That process will almost certainly take years. In the meantime, the state has to keep paying benefits it can’t afford, which will force it to raise taxes and/or reduce other spending. Any of the choices will probably make the state less attractive to potential new residents and businesses, putting downward pressure on property values and tax revenue. There was an interesting chart in the Khan Academy presentation showing that pension benefits are now absorbing 50% of the Illinois budget for education, and the amount keeps rising every year. Either school taxes have to go up, or an already stressed system will become even more stressed. (On a side note, I have never understood why a seemingly sane man like Rahm Emanuel wanted to be mayor of Chicago. It’s like volunteering to be captain of the Titanic just as the ship scrapes into the iceberg.)

As I said, all the options are bad. Very bad. Be very careful before you throw stones at Illinois, however. Your state, county, or city may not be far behind. Especially if you are in California. And sadly, there are some parts of Texas that are going to be just as bad as Illinois within 10 years unless action is taken soon.

How Many Trillions Did He Say?

The problem will not solve itself. Something has to change. Let me note that some 12 years ago I was writing about how US pension funds were underfunded by $2 trillion. I was considered alarmist by many. It turns out that once again I was overly optimistic instead. Wharton Business School called the pension funding problem the “invisible crisis” in a recent report:

Wharton finance professor Robert Inman provided this cautionary perspective: … researchers who have studied this crisis have “corrected a fundamental flaw in the way that people were thinking about these unfunded liabilities.” The bottom line, Inman said, was that there were $3 trillion worth of unfunded pension liabilities at the state level, and $400 billion of unfunded liabilities at the large-city level. That turns out to be about $10,000 per American citizen. (emphasis mine)

When you throw in all counties and cities, it gets even worse! If you were to use what I think of as more realistic 10-year return numbers (which assume at least one recession) and a low-interest-rate environment for at least half that time, that number gets to be over $4 trillion!!!

Stop here a second. In the 2005 letter I quoted above, I pointed to research that the public pension shortfall could be $2 trillion in 10 years. I added exclamation points then, too, because the number was so alarming.

Here we are ten years later. After the rather impressive bull market that began in 2009, we now find that unfunded liabilities have doubled. Does anyone seriously think that the Dow is going to 50,000 by 2025? Or that long-term rates are going back to 5–6%? And even if both of those things were to happen, unfunded liabilities would still be significantly worse in 2025 than they are today.

But there are pockets of problems that simply cannot go without a solution until 2025. Inman noted, for example, that Chicago’s unfunded liabilities are 10 times its revenues. “Just assume that they’re going to have to pay 5% of that [number annually]. That means you’re looking at 50% of their cash that will have go to pensions.” Philadelphia, Boston, New York, Houston, and other major cities will face similar challenges. “What does it mean for cities to do this?” Inman asks. “If that number is 50%, then $1 has to get you back at least twice the benefits [you spend].” That’s a very high threshold for city services to have to meet.

It is obvious to me that there are no good solutions. Current taxpayers will wind up having to pay higher taxes and/or receive a lower level of services in return for their contributions. That means more potholes, fewer new roads, and less money for education and parks and all those things that make up a city. Or, as Inman noted, the “solution” can come in the form of lower property values. Higher taxes mean the value of your home declines relative to the cost of the taxes. That’s just a fact.

The ultimate losers will be the people who own those properties whose value declines. As Inman notes, there is no way that businesses and households “are going to move into a city unless they are absolutely certain that they will get dollars back for every dollar they spend.” Who wants to move into a city where 50% or more of your tax dollars are used to pay the pensions of people who were working and retiring well before you moved in?

Politics being what it is, the losing groups will be the most diffuse, unorganized ones: taxpayers and property owners. Until they revolt. There will be a backlash. You can only squeeze blood from a turnip for so long before the turnip gets annoyed.

Illinois residents are already getting squeezed. Their state taxes are high and going higher. Their home values may also be high; but, at the very least, growth in the value of those homes is going to slow down. Illinois homes may well lose value in the next few years, and possibly a lot of value.

Put yourself on the other side of the trade. Would you buy Illinois real estate right now? Not unless you can get it at a steep discount. If you’re a business owner, would you expand into Illinois, knowing you and your workers will payer higher taxes for reduced public services?

The answers are obvious, and not just for Illinois. What we see there will be only the dress rehearsal for similar problems in other states with underfunded pensions. They won’t all have the constitutional barrier that is gumming up the works in Illinois, but it won’t be fun anywhere.

For what it’s worth, the five states with the best 2013 pension funding ratios, according to Bloomberg, are Wisconsin, South Dakota, North Carolina, Washington, and Tennessee. Note that these are not all “red states.” Proper fiscal controls can happen under liberal politicians as well. In a previous letter I went through the data on underfunded cities. Many of those were, surprisingly, cities you would have thought of as conservative. Local politics being what it is, and given how surprisingly few people actually get involved in local politics, budget shenanigans can happen anywhere.

Why Illinois Is the Next Greece

Pension shortfalls are a thorny problem. I have great sympathy for people who devoted their careers to civil service and counted on a certain level of benefits. Depending on the city or state backing those benefits, many will not realize them in full. I have sympathy also for homeowners who aren’t going to see their investments pay off, and for average citizens who will have to suffer through traffic that is heavier and lines that are longer than they should be. We’re all going to feel this.

The one group I don’t sympathize with is the governors and legislators who approved pension deals they had to know were wildly unrealistic. Even worse are the consultants who told them the deals would work. A plague on both their houses. These politicians used public goods to buy votes and thought they could kick the can down the road forever. They were wrong.

Illinois is going to have a “come to Jesus moment” within the next few years. They will either have to amend their constitution to allow for reduced benefits, with all the weeping and wailing and gnashing of teeth that will accompany such a move, or the judges will force them to raise taxes or to reduce spending on other essential services, which will again be accompanied by weeping and wailing and gnashing of teeth by those being asked to pay ever-higher taxes for reduced services. You’re going to continue to see companies leave Illinois, when they can move across the state line and be more competitive.

The federal government will not come to the aid of Illinois. You will not be able to find a majority in the Senate willing to vote to bail out Illinois. That vote won’t fly back in their home states.

So why is Illinois like Greece? Because Germany and the rest of the “northern” countries have basically told Greece to get its budgetary act together and to do so on the backs of its own people. Tsipras is negotiating as hard as he can, but he simply has nothing to negotiate with. The Europeans are no longer scared that Greece might leave the EU. However, if Greece were to leave, it would owe some €95 billion against bank balances of what may now be less than €120 billion, as money flies out of the country.

Remember Cyprus? Its bank depositors were, in many cases, simply wiped out. 100%. Some banks were able to negotiate a $100,000 insured deposit, but not the largest banks, and only if they were allied with a non-Cypriot bank. Basically, that is what Draghi is going to tell the Bank of Greece: “If you default, we will take all the collateral, and that means the deposits, too.” That is precisely what they are allowed to do under the rules. And while the Eurozone is working towards implementing deposit insurance, those rules have not yet taken effect. I’ve seen estimates that Greek depositors could lose as much as €.95 on the euro.

That would of course mean a return of the drachma and immediate economic collapse, with even higher unemployment than the current 25%; and the government would almost immediately be thrown out. But of course, if Tsipras does what he will have to do, which is to accede to European (read German) demands, then there will almost immediately be a vote of no confidence, and he will not be reelected. Tsipras is a dead politician walking.

Germany and its counterparts are using Greece as a moral object lesson for the rest of the periphery. You can bet that Portugal, Spain, and Italy (and France!) are watching and realizing they have to become far more serious in their reforms. Not that they are not already trying, but they are going to need to double down on reforms.

Illinois is going to provide the same object lesson to the rest of the 49 states. You can look at the table we highlighted earlier and see whether your state is headed in the wrong direction. Many states are in relatively good shape, and a few reforms can make them even better. There are some cities that are disaster zones, and they will be sad cases; but a serious majority can fix their problems if their politicians start to take action now. Pension reform will not be popular with the unions; but, as we can see from Illinois, even relatively modest changes were unpopular, and now the state is careening towards a civic financial collapse.

On the other hand, the Democratic leadership in Rhode Island actually pursued and got reform. Other states and cities are doing the same. If your state is in pursuing reform and using more realistic assumptions about future returns, then it is up to you to support such moves.

A lot of people will choose simply to move rather than stay and fight the good fight. Sad, but true. The data clearly shows that there is a general tendency to move from high-tax states to lower-tax states. While my former governor Rick Perry likes to take credit for all the jobs that have been created in Texas, the real growth factor was corporations fleeing high-tax states to come to Texas. It was the Texas state legislature that was the driver on low taxes. For sure, Perry was the evangelist and took advantage of their wisdom. But there are many other low-tax states, and nearly all of them are benefiting.

I enjoy reading Mauldin’s comments on U.S. public pensions as he raises important points on just how unsustainable the current course is and why U.S. public pension funds are delusional.

Nonetheless, he has the typical conservative spin on things which leads him to conveniently ignore the real origins of this looming crisis and how to properly address it.

Importantly, unlike Mauldin and others, I take a more balanced approach when discussing public pensions. Dismantling public pensions and replacing them with ineffective defined-contribution plans will only exacerbate America’s retirement nightmare.

American policymakers love treating public pensions as an evil. To be sure, just like in Greece, there are abuses that are a flagrant travesty, but the real reasons behind America’s public pension problem is lack of proper governance and state governments that have failed to top up their pensions over the years (so they can spend money elsewhere!). Also, Americans need to introduce shared-risk in their public pension plans once and for all, so that all the stakeholders feel the pain when the plans are underfunded.

And as I’ve repeatedly stated on this blog, the cure to the “public pension disease” is often worse than the disease. For example, very few policymakers and economists understand the brutal truth on defined-contribution plans and how they exacerbate pension poverty. Even worse, politicians and economists just don’t understand the social and economic benefits of defined-benefit plans.

Take the time to listen to Mish as he echoes a lot of what John Mauldin discusses above. Unfortunately, just like John, he misses the bigger picture on why America needs to enhance defined-benefit plans and Social Security for all Americans. But first they need to get the governance and risk-sharing of these public pensions right!!!

Even as companies across the country drop traditional pensions in favor of 401(k)s, corporate defined-benefit plan assets currently sit at an all-time high, according to Federal Reserve data.

The value of investments held by corporate defined-benefit plans—those that guarantee retirees a set payout—totaled $3.1 trillion at the end of 2014, according to the Federal Reserve.

That’s 5% more than a year earlier and more than five times as much as 30 years ago.

[…]

“It’s counterintuitive that assets are rising,” said Michael Moran, a managing director at Goldman Sachs Asset Management. But the math is simple, he added.

Pension-plan assets have grown by an average of between 9% and 13% a year for the past three decades.

Yet, the plans have only used between 6% and 8% of the assets to pay off retirees. That’s led to persistent growth.

The equation could change soon, however. More companies are considering pension transfers, and more baby boomers are retiring, Mr. Moran said.

That could mean pension-plan assets today are near their high water mark.

Amazon, HSBC, Ford and Citibank’s India offices just got a new landlord: The Canada Pension Plan Investment Board (CPPIB), which agreed this week to buy a 2.7 million square ft. “IT Park”.

Canada Pension Plan Investment Board (CPPIB) and Shapoorji Pallonji Group’s joint venture company SPREP has acquired SP Infocity IT Park in Chennai for $220 million.

[…]

The IT Park, located on the Old Mahabalipuram Road, has close to 2.7 million square feet of operational space, which is leased to firms such as HSBC, Amazon, Ford, Siemens, Citibank, AT&T and Hapag Lloyd.”

“SP Infocity IT Park is a high-quality property and is an excellent first acquisition for SPREP,” said Andrea Orlandi, Managing Director, Real Estate Investments, CPPIB. “Through this investment by SPREP, CPPIB continues to demonstrate our long-term commitment to the Indian real estate market.

In 2013, CPPIB and Shapoorji Pallonji had entered into a strategic alliance to acquire foreign direct investment (FDI)-compliant, stabilised office buildings in the major cities of India. CPPIB owns 80% of the venture with an initial equity commitment of $200 million and the venture is supported locally by Shapoorji Pallonji Investment Advisors.

The deal has been in the works since April or earlier. CPPIB has invested nearly $1.5 billion in India since 2010.

Photo by sandeepachetan.com travel photography via Flickr CC License

The plan calls for the state to make its full payment of $3.1 billion in 2016; Christie’s budget proposal called for a partial payment of $1.3 billion.

The proposal would be funded by shifting 2015’s excess tax revenue to 2016, and by levying a tax on millionaires.

Democrats have pledged to increase the pension contribution in Gov. Chris Christie’s proposed budget from $1.3 billion to $3.1 billion.

“The state should balance its budget and fully fund its pension obligation, and this prepayment is part of our efforts to fix these problems and move the state’s economy in the right direction,” state Assembly Speaker Vincent Prieto (D-Hudson) said in a statement.

Calling it a 2016 prepayment, Democrats have opted to count the additional, new $300 million, which it attributed to “stronger-than-expected June tax collections,” toward the contribution in the fiscal year beginning July 1.

“Making the payment upfront, rather than next June, will generate more than $21 million in additional investment income over the course of the fiscal year,” state Senate President Stephen Sweeney (D-Gloucester) said in a statement. “It is important that we get every dollar we can into the pension system because every $1 we put in now saves us $3 in the future.”

It’s not clear whether lawmakers can actually take 2015’s $300 million in excess revenue and shift it into the next budget.

Photo credit: “New Jersey State House” by Marion Touvel – http://en.wikipedia.org/wiki/Image:New_Jersey_State_House.jpg. Licensed under Public domain via Wikimedia Commons

The Chicago Public School system (CPS) is required to make a $634 million pension payment on June 30. But as CPS runs dangerously low on cash, Mayor Rahm Emanuel is pushing for the pension fund to accept a partial payment.

Emanuel is cautioning that the full payment would come at the expense of classrooms, and the teachers and children that occupy them.

Chicago Public School finances are “at the breaking point,” Mayor Rahm Emanuel said Monday, arguing the cash-strapped school district cannot afford to make a $634 million teacher pension payment due June 30 — at least not in full.

“If you make that pension payment in its completion, which has been done four years in a row for the first time in a long time … we could no longer make that payment and not have it impact the school building and the classroom,” the mayor said.

[…]

A partial payment would be a dubious and dangerous first that could trigger a pension fund lawsuit and a further drop in a CPS bond rating already reduced to junk status.

The audit concluded CPS will “run out of cash as early as this summer” and be unable to meet payroll, pension and debt payments without “third-party intervention.” School could open late, class sizes could skyrocket and sports could be eliminated.

If CPS does miss the payment, it would be the first time in history it did so without permission from lawmakers.

Kentucky lawmakers spent much of the last legislative session considering the issuance of a proposed $3.3 billion pension bond, which would be used to shore up the funding of the state’s Teachers’ Retirement System.

KTRS officials warn that if the system doesn’t get an influx of cash, the state’s contribution will increase from $107 million in this fiscal year to more than $802 million in 2020. That number would only grow to $408 million with the $3.3 billion bond measure, officials say.

The system has $18.1 billion in assets. But [executive director] Harbin said between 2014 and the end of 2016, KTRS will have sold $1.3 billion to meet current obligations.

“This is really strapping our investment strategy, we’re pulling money away from good managers that are doing good jobs for us, selling assets in order to meet payroll,” Harbin said.

The system is also bracing itself for an influx of baby boomer teachers retiring and collecting pension checks instead of contributing to the system.

“The bottom line is you’re going to be under this pressure for a period of time and without some relief, your status in the next five or 10 years is going to become critical,” said Rep. Brent Yonts, a Democrat from Greenville. “The boiler’s going to blow up if we don’t give you a solution.”

KTRS estimates that the $3.3 billion bond would boost the system’s funding ratio from 53 percent to 66 percent.

Photo credit:”Ky With HP Background” by Original uploader was HiB2Bornot2B at en.wikipedia – Transferred from en.wikipedia; transfer was stated to be made by User:Vini 175.. Licensed under CC BY-SA 2.5 via Wikimedia Commons

A proposed overhaul of the U.S. military’s pension system, endorsed by the Pentagon last week, has now hit a roadblock.

The overhaul was one piece of a much larger military bill that included banning the use of torture.

The Senate passed the bill on Thursday, and then threw up an obstacle. From the New York Times:

The Senate on Thursday passed a $600 billion defense policy bill that would rein in pension costs, ban the use of torture and authorize lethal offensive weapons for Ukraine. But it then immediately rejected a measure to pay for it, the first battle in a spending fight that could end in a government shutdown this fall.

The blocking of the military appropriations bill was the first in a series of rejections Democrats have promised as they try to force Republicans into reopening budget talks.

Democrats — and many Republicans — want to lift spending limits imposed in 2011 that are just now being applied across an array of government programs. Absent new bipartisan budget talks — the sort that have often failed in Congress before — President Obama has pledged to veto spending bills if Democrats do not kill them on the Senate floor first.

The defense bill was a particular thorn to Democrats because as written, the Defense Department would be authorized to shift an extra $38 billion in war funds into its regular operating budget. Democrats and the White House have denounced that as a gimmick designed to let the military get around spending restrictions other federal agencies must abide.

As mentioned above, the blocking of the bill has little to do with the retirement overhaul portion of the measure.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com.

A pension reform initiative filed last week requires voter approval of termination fees, the big upfront payment demanded by CalPERS when a plan is closed to new members.

CalPERS says it needs the money to ensure payment of the pensions promised members who remain in the closed plan. The termination fee is calculated by dropping the pension fund earnings forecast from the current 7.5 percent to as low as 2.98 percent.

It’s particularly important because if a closed plan does not have enough assets to pay promised pensions, CalPERS has the power under current law to cut the pensions to the level covered by the assets.

A series of state court decisions, a key one in 1955, are widely believed to mean that the public pension offered on the date of hire becomes a “vested right,” protected by contract law, that can only be cut if offset by a comparable new benefit.

But as U.S. Bankruptcy Judge Christopher Klein probed state pension law during the Stockton bankruptcy trail in May last year, David Lamoureux, CalPERS deputy chief actuary, described in detail how CalPERS pensions can be cut outside of bankruptcy.

Ruling that CalPERS pensions can be cut in bankruptcy, Klein said a termination fee that boosted the Stockton pension debt or “unfunded liability” from $211 million to $1.6 billion was a “poison pill” if the city tried to move to another pension provider.

The CalPERS board is said by some to be dominated by public employee union members and their allies. But under the state constitution, CalPERS has a fiduciary duty to give pension protection priority over minimizing taxpayer costs.

Pensions and taxpayers had equal standing until voters approved labor-backed Proposition 62 in 1992, a constitutional amendment giving public pension systems sole control of their assets and actuarial functions after a state “raid” on CalPERS funds.

The initiative filed last week by a bipartisan group is a constitutional amendment that requires voter approval of a “defined benefit pension plan” for new state and local government employees hired on or after Jan. 1, 2019.

Depending on the votes for everything from giant statewide CalSTRS and CalPERS school plans to six-member cemetery district benefits, some current plans could be closed to new members, triggering a termination fee.

If voters then reject a large CalPERS termination fee, would pensions be cut to the level covered by plan assets or would there be a lengthy legal battle?

Vallejo and San Bernardino officials said a CalPERS threat of a costly legal battle, possibly all the way to the U.S. Supreme Court, influenced their decisions not to try to cut pensions in bankruptcy. Stockton officials, on the other hand, said from the outset they wanted to protect pensions.

VOTER EMPOWERMENT ACT OF 2016

g) Retirement boards shall not impose termination fees, accelerate payments on existing debt, or impose other financial conditions against a government employer that proposes to close a defined benefit pension plan to new members, unless voters of that jurisdiction or the sponsoring government employer approve the fees, accelerated payment, or financial conditions.

Critics sometimes say of CalPERS, borrowing from an old “roach motel” pesticide commercial and the “Hotel California” pop song: “You can check in, but you can’t check out.”

Several small plans considered leaving CalPERS but did not after looking at a large termination fee. Democrat Chuck Reed, a leader with Republican Carl DeMaio of the bipartisan group that filed the initiative, has first-hand experience with the termination fee.

While he served as mayor of San Jose, Reed and the city council voted unanimously three years ago to explore switching their own retirement plan from pensions to 401(k)-style individual investment plans.

Most San Jose employees are in two large city-run plans. The council considered terminating its own CalPERS plan as a share-the-pain gesture after voters in June 2012 approved a Reed-backed reform that, among other things, cut pensions for new hires.

The small plan created in 1998 for mayors and the city council had about 30 members, 10 retired. The plan had 72 percent of the projected assets needed to pay future pensions, with a pension debt or “unfunded liability” of $976,000.

“CalPERS said, ‘You can write us a check for $5 million,’” Reed said last week.

The price tag was far too high. Reed, barred by term limits from running for re-election, left office in January and receives a CalPERS pension, a benefit that would have been unchanged even if the small plan had switched to 401(k) plans for new hires.

Two small cities, Pacific Grove and Canyon Lake, have looked at leaving CalPERS but balked at the high termination fees. Villa Park officials asked for a termination fee estimate to publicize the high CalPERS termination fee.

The Orange County city, population 5,800, has 30 members in its CalPERS plan, seven active, and contracts for police and firefighter services. The updated Villa Park minimum CalPERS termination fee was $3.7 million.

“We don’t have the money, and we are not going to borrow money,” Villa Park Mayor Diana Fascenelli said in a report last March in the Orange County Register.

For some, the big termination fee for plans closed to new members brings to mind a “Ponzi scheme,” where money needed to pay earlier investors comes from new investors. Reed and a former Villa Park mayor, Rick Barnett, made the comparison.

Gov. Brown had the same reaction to a CalPERS analysis of his proposal to give new hires a federal-style “hybrid” plan, combining a smaller pension with a 401(k)-style plan, that was rejected by the Legislature.

“When I read the PERS analysis they say if you close the system of defined benefit (pensions) and don’t let any more people in, then the system would become shaky — well, that tells you you’ve got a Ponzi scheme,” Brown told legislators in 2011.

During the Stockton bankruptcy trial, Lamoureux, the CalPERS chief deputy actuary, explained why the city had a $1.6 billion termination fee. A low bond-based earnings forecast was used to discount the future pension debt.

After the termination fee is paid, CalPERS becomes responsible for the pension debt and cannot get more money from the local government employer if funds fall short as pensions are paid during the lifetime of the retirees.

If a city cannot pay all of the debt owed for a terminated plan, the CalPERS board has the power to evenly cut pensions to an amount that would be covered by what the city was able to pay.

But after the payment has been made and responsibility for the plan shifts from the city to CalPERS, if the terminated agency pool falls short the funds of all of the state and local government plans in the system could be used to cover the shortfall.

CalPERS keeps a healthy surplus, and a lot of risk-free bond investments, in its Terminated Agency Pool. As of June 30, 2013, the pool had about 90 small plans, $78 million in future pension obligations, $194 million in assets and was 249 percent funded.

For the first time, the CalPERS board was given a detailed annual valuation report of the Terminated Agency Pool last month in addition to the usual briefing on the status of the fund.

The plight of 79-year-old Athenian Zina Razi and thousands like her strikes at the heart of why talks between Greece and its creditors have collapsed. She lives off a pension system that helps to consume a huge proportion of state spending and can appear overly indulgent – but still she’s broke.

Razi barely keeps up with her power and water bills, and since her middle-aged son lost his job, supports him as well. “I am always in debt,” she said. “I can’t even imagine going to the cinema or the theatre like I did in the past.”

This paradox goes a long way to explain why the leftist-led government and its creditors at the European Union and IMF have failed to bridge their differences over a cash-for-reform deal, leading to Sunday’s breakdown of talks.

Five years of austerity policies imposed at the creditors’ behest have helped to turn a recession into a full-blown depression, and still they want more. Athens has flatly refused to achieve further savings by raising value-added tax on essential items or, crucially, slashing pension benefits.

As it inches closer to default and a potentially calamitous exit from the eurozone, the government has dismissed such demands as “absurd” or designed to pummel Greeks’ morale.

To the lenders, the pension system is still too generous compared with what the country can afford. Greece spent 17.5 per cent of its economic output on pension payments, more than any other EU country, according to the latest available Eurostat figures from 2012. With existing cuts, this figure has since fallen to 16 per cent.

However, one person familiar with the talks said wages and pensions together still eat up 80 per cent of primary state spending, before debt servicing costs. “The remaining 20 per cent is already cut to the bone, indeed too far,” he said. “Civil servants have no pencils to write with, buildings in need of maintenance are crumbling. It’s not possible to make public finances sustainable without working on wages and pensions.”

Despite years of reforms, many Greeks can still retire early, especially workers in the public sector and professions classified as hazardous such as the army.

One high profile example is Fofi Gennimata, who became the leader of the opposition PASOK party last weekend. She is a former bank clerk with three children who applied for a pension last year aged just 51. Her office says she has stopped taking the pension payment since becoming a member of parliament.

Greece’s state spending on pensions is three times’ higher as a proportion than Germany’s, and critics accuse Greece of wanting a soft life at somebody else’s expense.

UNHELPFUL DEMOGRAPHICS

Demographics haven’t helped Greece. The number of pensioners has been rising since 2009. That’s either because the state has offered incentives to workers to retire as part of efforts to cut wage costs, or because workers themselves rushed to do so before the government raised the retirement age.

To many Greeks, not least the Syriza party that stormed to power in January promising to push the clock back on austerity, the creditors’ demands are yet another way to clobber vulnerable people needlessly.

The lenders have denied asking for specific pension cuts. But the Greek side said among their suggestions was slashing a top-up payment that supports some of the poorest pensioners. For Razi, that would mean losing 180 euros ($203) out of her 650-euro monthly pension. The average Greek pension is 833 euros a month. That’s down from 1,350 euros in 2009, according INE-GSEE, the institute of the country’s largest labor union. Moreover, 45 per cent of pensioners receive monthly payments below the poverty line of 665 euros, the government says. With more than a quarter of Greek workers jobless, many rely on parents and grandparents for financial support.

“They can take our money, but they cannot take our hearts and souls. We live for our dignity,” Razi said.

CHRISTMAS BONUS

Pension reform is a vexed issue for many European countries with aging populations that can no longer support a generous entitlement system. Italy raised the retirement age under unpopular reforms in 2012.

With pension spending equivalent to 14 per cent of economic output, France’s pensions advisory council estimates the system will run a deficit of 9.2 billion euros by 2020 despite reforms decided already. Attempts by Greece’s EU neighbour Bulgaria, where some public sector workers can retire in their forties, to raise the pension age recently provoked protests.

But Athens is running out of time to find savings acceptable to the European Commission, European Central Bank and International Monetary Fund to seal a deal on unlocking aid it needs to repay 1.6 billion euros to the IMF at the end of June.

Both sides have agreed on a budget surplus Greece should target but not on how to achieve it. The lenders want Greece to make savings on pensions equivalent to about 2 billion euros a year. Greece offered cuts of only 71 million, the lenders said.

Giving ground on pensions would force Prime Minister Alexis Tsipras into a U-turn that could prompt calls for new elections or a referendum. One of Tsipras’s campaign promises was restoring a Christmas bonus for low-income pensioners, although that plan may be postponed.

Previous governments have tackled the problem. Pensions have been cut by an average of 27 per cent between 2010-2014 and by 50 per cent for the highest earners. The average retirement age was raised by two years in 2013 and Greece has said it is willing to curb early retirement benefits further.

On average Greek men now retire at 63 and women at 59, according to government data. In Germany, the average retirement age for those receiving an old age pension in 2014 was 64 years. But that figure goes down to 61.3 years once those taking early retirement on health grounds is taken into account, according to 2013 data.

Five years ago, Sissy Vovou’s pension was €1,330 (£953) and landed in her back account 14 times a year: you used to get, she wistfully recalls, a full extra month at Christmas, plus a half each at Easter and for the summer.

Now it is a monthly €1,050 – and there are only 12 months in the Greek pensioner’s year. “In all,” she said, “I’ve lost 30% of my income. And I’m one of the lucky ones. I’m in the top fifth; 80% of Greek pensioners are worse off than me.”

Vovou, 65, who began work at 17 in the publishing industry and ended her career at the state broadcaster, ERT, is also lucky because her son, now 40, has a good job and a regular salary. She does not need to help him out.

Eleni Theodorakis, on the other hand, retired in 2008 from her job as an administrative assistant in a regional planning service, aged 55. “My pension is €942 euros a month – not too bad, really,” she said, almost shamefacedly, fishing the statement out of her handbag.

“Fortunately my son is all right, just about, though sometimes he gets paid late. And once or twice, not at all. But my daughter’s husband has been unemployed for four years now. They have a baby … I give them what I can. It isn’t easy. Thankfully, my sister has a big garden. We grow things.”

There are many like Theodorakis among Greece’s 2.65 million pensioners. According to a study last year by an employer’s association, pensions are now the main – and often only – source of income for just under 49% of Greek families, compared to 36% who rely mainly on salaries. With a jobless rate of about 26% – youth unemployment is at 50% – and out-of-work benefits of €360 a month generally paid for no longer than a year, pensions have become “a vital part of the social security net for many, many people,” said Vovou. “Retired parents are having to help their adult children everywhere. And now they’re demanding we cut them even more? It’s just so very wrong.”

Pensions have become arguably the biggest hurdle in the tortuous, on-off negotiations between the leftwing government of the prime minister, Alexis Tsipras, and Greece’s creditors: its eurozone partners, the European Central Bank and the International Monetary Fund.

Before they will release €7.2bn in aid that Greece needs to pay public-sector salaries and pensions and repay €1.6bn in IMF loans, those lenders want further reforms to the pensions system, including penalties to put people off taking early retirement and more cuts to even the lowest pensions.

Tsipras is so far refusing to implement the measures, aimed at shaving the equivalent of 1% of GDP off the country’s pension bill, arguing they will do nothing to help Greece emerge from a slump that has seen the country’s economy shrink by 25%, and may only deepen its humanitarian crisis.

There is little doubt Greece’s pensions system needed reform. The EU’s most expensive, at about 17.5% of GDP, it was made up of more than 130 different pension funds and hid widespread abuse: a pension census ordered in 2012 as part of the country’s bailout conditions turned up more than 90,000 entirely bogus claimants – mostly the relatives of long-dead pensioners – and 350,000 more inconsistent claims.

Greece also had a remarkable 580 professions deemed hazardous or strenuous enough to qualify for early retirement: firemen and construction workers, certainly, but also hairdressers (because of the chemicals), wind instrument players (gastric reflux) and radio presenters (microbes in microphones).

But some reforms are under way: those 130 funds have shrunk to 13, the standard retirement age for men has been lifted to 67, and, above all, since 2010 public and private sector pensions have been severely pruned, on a scale ranging from a 15%-cut for the very lowest (under €500 a month) to as much as 44% for highest (more than €3,000).

Greek pensions are now, on the whole, far from exorbitant: social security ministry figures show the average main pension is €713 a month, and the average top-up pension – typically funded by an industry retirement scheme – €169 per month. Some 60% of pensioners get less than €800 gross a month, and 45% live on less than the monthly poverty limit of €665.

The problems the system faces now are closely related to the country’s particular plight – and Athens is not alone in arguing that further flat, across-the-board pension cuts of the kind envisaged by its creditors are unlikely to accomplish much beyond hurting pensioners even more. The record-high unemployment rate, for example, means the pensions system is running a big deficit: contributions coming in are forecast, this year, to be roughly €2bn less than benefits going out.

With unemployment among the over-55s at about 20%, compared to just 6% five years ago, “I felt it was the wisest thing to do,” said Ioannis Konstatinidis, who retired four years early from a large, now privatised bank in 2012.

“People were losing their jobs, salaries were being cut, and there was so much uncertainty I just thought it was better to be sure of getting at least something.” Konstatinidis has ended up getting nearly 40% less than he had counted on, however. “Our retirement will not be quite as comfortable as we’d thought. But we’re luckier than lots of people.”

They are. Among the pension cuts being proposed is the abolition of the EKAS, a variable supplementary payment made to nearly 200,000 Greek pensioners to bring their monthly income up to €700 a month. (Other suggestions made by Greece’s creditors would hit people like that particularly hard: a hike in the tax on electricity, for example, from 13% to 23%).

Few Greeks think further pension cuts will achieve anything. They may also be illegal: the country’s highest court has already ruled that the private-sector pension cuts pushed through in 2012 were unlawful because they “deprived pensioners of the right to decent life”.

Unsurprisingly, the country’s pensioners’ unions have called for a major demonstration against further cuts on 23 June. “The government must absolutely not give in,” said Anastassios Georgiadis, of the retired postal workers’ association. “And Europe has to understand that it is not by making us even poorer that Greece will emerge from this crisis.”

I recently discussed the plight of Greek pensioners in my comment on a Greek suicide, referring to articles from CNBC and Bloomberg, but also referring to comments Greek finance minister Yanis Varoufakis made in Germany in his keynote speech:

I am often asked: “Be that as it may, why have you not concluded the negotiations with the institutions? Why are you not agreeing with them quickly? There are three reasons why.

First, the institutions are insisting on economically unsustainable macroeconomic numbers. Consider three such crucial numbers for the next seven years: The average growth rate, the average primary surplus and the average magnitude of fiscal measures (e.g. new taxes, benefit or pension reductions). The institutions propose to us actual numbers that are inconsistent with one another. They begin by assuming that Greece should achieve an average growth rate of about 3%. That’s fine and good. But then, in order to remain consistent with their ‘goal’ of showing that our debt can come down to 120% of our national income by 2022, they demand primary surpluses in excess of 3%, with large fiscal measures to achieve these primary surpluses. The trouble here, of course, is that if we were to agree to these numbers, and impose upon our weak economy these highly recessionary fiscal surpluses, we will never achieve the above 3% growth rate that they assume. The end result of agreeing with the institutions on their unsustainable fiscal numbers is that Greece will, yet again, fail miserably to achieve the promised growth targets, with appalling effects on our people and on our capacity to repay our debts. In other words, the past five years of spectacular failure will continue into the future. How can our new government consent to this?

Secondly, we may be an ideological government of the Radical Left but, unfortunately, it is the institutions that carry ideological fixations that make it impossible to reach an agreement. Take for example their insistence that Greece should be a labour protection-free zone. Two years ago, the troika and the government of the time disbanded all collective bargaining. Greek workers are left to their own devices to bargain with employers. Labour rights that took more than a century to win were swept away in a few hours. The result was not increased employment or a more efficient labour market. The result was a labour market in which more than one third of paid labour is undeclared, thus condemning pension funds and the government’s tax take to permanent crisis. Our government has tabled a highly sensible proposal: To take the matter to the International Labor Organization and to have them help us draft a modern, flexible, business-friendly piece of legislation that restores collective bargaining to its rightful place in a civilised society. The institutions rejected that proposal, branding our stance “backtracking from reforms”.

The third reason why we have not been able to agree with the institutions are the social unjust and unsustainable measures that they insist upon. For example, the lowest of pensions in Greece amount to 300 euros, of which more than 100 euros are made up by what is known as ‘solidarity pension’, or EKAS. The institutions insist that we eradicate EKAS while at the same time proposing that we push value added taxes on pharmaceuticals (that pensioners relay upon) from 6% to 12% and electricity from 13% to 23%. Put simply, no government that has a smidgeon of sensitivity toward the weakest of citizens can ever agree with such proposals.

“Of course this pension system is not sustainable,” Finance Minister Yanis Varoufakis said in Berlin on June 8. “Any butcher can take a cleaver and start chopping things down. We need surgery. We need to find ways of eliminating early retirements, of merging pension funds, of reducing their operating costs, of moving from an unsustainable to a sustainable system, rationally and gradually.”

Additional wage cuts will not help export-oriented companies, which are mired in a credit crunch. And further cuts in pensions will not address the true causes of the pension system’s troubles (low employment and vast undeclared labor). Such measures will merely cause further damage to Greece’s already-stressed social fabric, rendering it incapable of providing the support that our reform agenda desperately needs.

I partially agree with Varoufakis but as I’ve previously stated, he conveniently ignores to mention the single biggest problem with Greek pensions, namely, the total lack of proper governance which introduces real transparency and accountability. Instead, the people running these pensions are political appointees or union hacks who are completely and utterly clueless on proper pension governance.

Pension governance, or lack of, is the true cancer of the Greek pension and economic system. If Greek pensions weren’t forced by law to buy Greek bonds, maybe they wouldn’t have taken a huge hit when Greece restructured its debt in 2012.

Instead, you have a bunch of clowns that are politically appointed by the ruling government du jour running a number of public pensions that should have been consolidated a long time ago. No Greek government has ever taken pension management seriously. If they did, they would scour the globe to hire the best and brightest Greek pension managers, pay them properly and protect them from political patronage.

Who are these people? There are plenty of extremely sharp Greeks in finance and some of them have experience running large pension funds. One example is Theodore Economou, someone I’ve profiled on my blog and think very highly of. There are many others working all over the world.

But before Greece starts hiring “the best and brightest,” it should change its laws, introduce real governance like nominating a qualified independent board of directors, making public pension funds more transparent and a lot more accountable.

Of course, no Greek government wants to do this because good governance is anathema to the Greek way of life where corruption and inefficiency run rampant.

Keep all this in mind as the endgame for Greece and Europe plays out once again. I still maintain Greece will get some form of debt relief, but I’m worried that the country I love so dearly has fallen so far behind that no matter what deal it gets, it’s doomed for decades of economic weakness.

Photo jjMustang_79 via Flickr CC License

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712