Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Timothy W. Martin, Georgi Kantchev and Kosaku Narioka of the Wall Street Journal report, Era of Low Interest Rates Hammers Millions of Pensions Around World (h/t Ken Akoundi, Investor DNA):

Central bankers lowered interest rates to near zero or below to try to revive their gasping economies. In the process, though, they have put in jeopardy the pensions of more than 100 million government workers and retirees around the globe.

In Costa Mesa, Calif., Mayor Stephen Mensinger is worried retirement payments will soon eat up all the city’s cash. In Amsterdam, language teacher Frans van Leeuwen is angry his pension now will be less than what his father received, despite 30 years of contributions. In Tokyo, ex-government worker Tadakazu Kobayashi no longer has enough income from pension checks to buy new clothes.

Managers handling trillions of dollars in government-run pension funds never expected rates to stay this low for so long. Now, the world is starved for the safe, profitable bonds that pension funds have long needed to survive. That has pulled down investment returns and made it difficult for funds to meet mounting obligations to workers and retirees who are drawing government pensions.

As low interest rates suppress investment gains in the pension plans, it generally means one thing: Standards of living for workers and retirees are decreasing, not increasing.

“Unless ordinary people have money in their pockets, they don’t spend,” the 70-year-old Mr. Kobayashi said during a recent protest of benefit cuts in downtown Tokyo. “Higher interest rates would mean there’d be more money at our disposal, even if slightly.”

The low rates exacerbate cash problems already bedeviling the world’s pension funds. Decades of underfunding, benefit overpromises, government austerity measures and two recessions have left many retirement systems with deep funding holes. A wave of retirees world-wide is leaving fewer active workers left to contribute. The 60-and-older demographic is expected to roughly double between now and 2050, according to the United Nations.

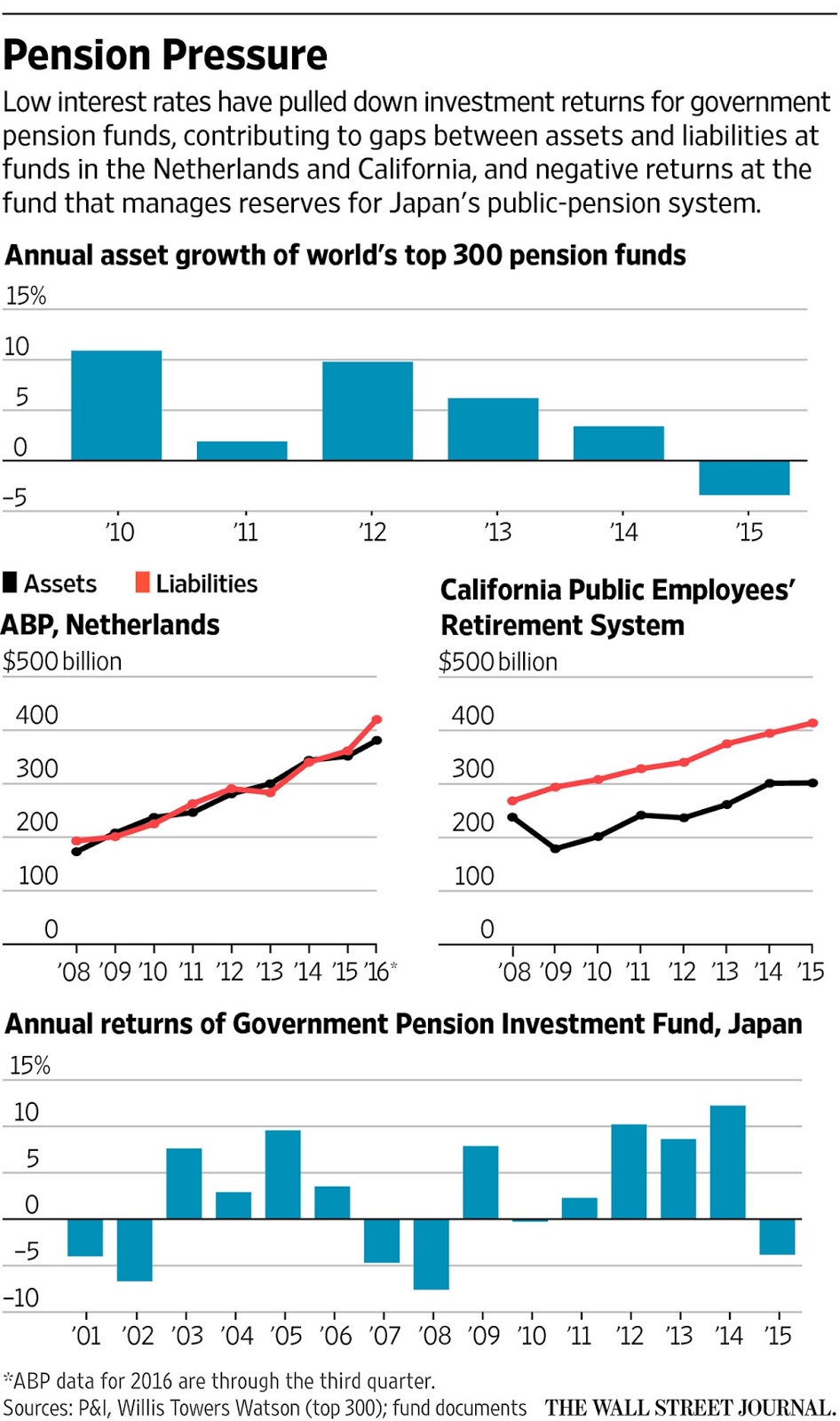

Government-bond yields have risen since Donald Trump was elected U.S. president, though few investors expect a prolonged climb. Regardless, the ultralow bond yields of recent years have already hindered the most straightforward way for retirement funds to recover—through investment gains (click on image).

Pension officials and government leaders are left with vexing choices. As investors, they have to stash away more than they did before or pile into riskier bets in hedge funds, private equity or commodities. Countries, states and cities must decide whether to reduce benefits for existing workers, cut back public services or raise taxes to pay for the bulging obligations.

“Interest rates have never been so low,” said Corien Wortmann-Kool, chairwoman of the Netherlands-based Stichting Pensioenfonds ABP, Europe’s largest pension fund. It manages assets worth €381 billion, or $414 billion. “That has put the whole system under pressure.” Only about 40% of ABP’s 2.8 million members are active employees paying into the fund.

Pension funds around the world pay benefits through a combination of investment gains and contributions from employers and workers. To ensure enough is saved, plans adopt long-term annual return assumptions to project how much of their costs will be paid from earnings. They range from as low as a government bond yield in much of Europe and Asia to 8% or more in the U.S.

The problem is that investment-grade bonds that once churned out 7.5% a year are now barely yielding anything. Global pensions on average have roughly 30% of their money in bonds.

Low rates helped pull down assets of the world’s 300 largest pension funds by $530 billion in 2015, the first decline since the financial crisis, according to a recent Pensions & Investments and Willis Towers Watson report. Funding gaps for the two biggest funds in Europe and the U.S. have ballooned by $300 billion since 2008, according to a Wall Street Journal analysis.

Low rates helped pull down assets of the world’s 300 largest pension funds by $530 billion in 2015, the first decline since the financial crisis, according to a recent Pensions & Investments and Willis Towers Watson report. Funding gaps for the two biggest funds in Europe and the U.S. have ballooned by $300 billion since 2008, according to a Wall Street Journal analysis (click on image).

Few parts of Europe are feeling the pension pain more acutely than the Netherlands, home to 17 million people and part of the eurozone, which introduced negative rates in 2014. Unlike countries such as France and Italy, where pensions are an annual budget item, the Netherlands has several large plans that stockpile assets and invest them. The goal is for profits to grow faster than retiree obligations, allowing the pension to become financially self-sufficient and shrink as an expense to lawmakers.

ABP currently holds 90.7 cents for every euro of obligations, a ratio that would be welcome in other corners of the world. But Dutch regulators demand pension assets exceed liabilities, meaning more cash is required than actually needed.

This spring, ABP officials had to provide government regulators a rescue plan after years of worsening finances. ABP’s members, representing one in six people in the Netherlands, haven’t seen their pension checks increase in a decade. ABP officials have warned payments may be cut 1% next year.

“People are angry, not because pensions are low, but because we failed to deliver what we promised them,” said Gerard Riemen, managing director of the Pensioenfederatie, a federation of 260 Dutch pension funds managing a total of one trillion euros.

Benefit cuts have become such a divisive issue that one party, 50PLUS, plans for parliamentary-election campaigns early next year that demand the end of “pension robbery.”

“Giving certainty has become expensive,” said Ms. Wortmann-Kool, ABP’s chairwoman.

That is tough to swallow for Mr. van Leeuwen, the Amsterdam language teacher. Sitting on a bench near one of the city’s historic canals, he fumed over how he had paid the ABP every month for decades for a pension he now believes will be less than he expected.Japan is wrestling with the same question of generational inequality. Roughly one-quarter of its 127 million residents are now old enough to collect a pension. More than one-third will be by 2035.

The demographic shift means contributions from active workers aren’t sufficient to cover obligations to retirees. The government has tried to alleviate that pressure. It decided to gradually increase the minimum age to collect a pension to 65, to require greater contributions from workers and employers and to reduce payouts to retirees.A typical Japanese couple who are both 65 would collect today a monthly pension of ¥218,000 ($2,048). If they live to their early 90s, those payouts, adjusted for inflation, would drop 12% to ¥192,000.

The Japanese government has turned to its $1.3 trillion Government Pension Investment Fund for cash injections six of the past seven years. That fund, the largest of its kind in the world, manages reserves for Japan’s public-pension system and seeks to earn returns that outpace inflation. The more it earns, the more it can shore up the government’s pension system.

In February, Japanese central bankers adopted negative interest rates for the first time on some excess reserves held at the central bank so commercial banks would boost lending. The pension-investment fund raised a political ruckus in August when it said it lost about ¥5.2 trillion ($49 billion) in the space of three months, the result of a foray into volatile global assets as it tried to escape low rates at home.

The fund’s target holdings of low-yielding Japanese bonds were cut to 35% of assets, from 60% two years ago, and it has added heaps of foreign and domestic stocks. It is now considering investing more in private equity.

The government-mandated target is a 1.7% return above wage growth. “We’d like to strive to accomplish that goal,” said Shinichiro Mori, a deputy director-general of the fund’s investment-strategy department.

The fund posted a loss of 3.8% for the year ended in March because of the yen’s surge and global economic uncertainty. It was its worst performance since the 2008 global financial crisis. Mr. Mori said performance “should be evaluated from a long-term perspective,” citing returns of ¥40 trillion ($376 billion) since 2001.

Mr. Kobayashi, the former Tokyo government worker, said the government’s effort to boost returns by making riskier investments was supposed to “increase benefits for everyone, even if only slightly. It didn’t turn out that way…And they are inflicting the loss on us.”

Mr. Kobayashi joined roughly 2,300 people who marched in downtown Tokyo in October to protest government plans to cut pension benefits further.

In the U.S., the country’s largest public-pension plan is struggling with the same bleak outlook. The California Public Employees’ Retirement System, which handles benefits for 1.8 million members, recently posted a 0.6% return for its 2016 fiscal year, its worst annual result since the financial crisis. Its investment consultant recently estimated that annual returns will be closer to 6% over the next decade, shy of its 7.5% annual target.

Calpers investment chief Ted Eliopoulos’s strategy for the era of lower returns is to reduce costs and the complexity in the fund’s $300 billion portfolio. He and the board decided to pull out of hedge funds, shop major chunks of Calpers’ real-estate and forestry portfolios and halve the number of external money managers by 2020.

“Calpers isn’t taking a passive approach to the anticipated lower return rates,” fund spokeswoman Megan White said. “We continue to reassess our strategies to improve performance.”

Yet the Sacramento-based plan still has just 68% of the money needed to meet future retirement obligations. That means cash-strapped cities and counties that make annual payments to Calpers could be forced to pay more.

That is a concern even for cities such as affluent Costa Mesa in Orange County, which has a strong tax base from rising home prices and a bustling, upscale shopping center.

The city has outsourced government services such as park maintenance, street sweeping and the jail, as a way to absorb higher payments to Calpers. Pension payments currently consume about $20 million of the $100 million annual budget, but are expected to rise to $40 million in five years.

The outsourcing and other moves eliminated one-quarter of the city’s workers. The cost of benefits for those remaining will surge to 81 cents of every salary dollar by 2023, from 37 cents in 2013, according to city officials.

The mayor, Mr. Mensinger, is hopeful for a state solution involving new taxes or a benefits overhaul, either from lawmakers in Sacramento or from a California ballot initiative for 2018 that would cap the amount cities pay toward pension benefits for new workers.

Weaker cities across California could face bankruptcy without help, said former San Jose Mayor Chuck Reed, who oversaw a pension overhaul there in 2012 and is backing the 2018 initiative that would shift onto workers any extra cost above the capped levels. “Something is broken,” he said. “The plans are all based on assumptions that have been overly optimistic.”

Costa Mesa resident James Nance, 52, worries the city’s pension burden will affect daily life. “We could use more police,” said the self-employed spa repairman. “I’d like to know the city is safe and well protected, but I know there have been tremendous cutbacks.”

Costa Mesa ended the latest fiscal year with an $11 million surplus, its largest ever. But that will soon disappear, Mr. Mensinger said, as pension costs swallow up $2 of every $5 spent by the city.

“We have this gigantic overhead cliff called pensions.”

This is an excellent article which gives you a little glimpse of what lies ahead as global pensions confront an era of low growth and ultra low rates which are here to stay.

Or are they? Ken Akoundi of Investor DNA (subscribe for free here to receive his daily email with links to interesting articles like the one above) also posted a link to a free Stratfor report, Inflation Makes a Comeback in the Global Economy, which states assuming recent signals in the market are not false alarms, the world’s economies may be in for a big readjustment in 2017.

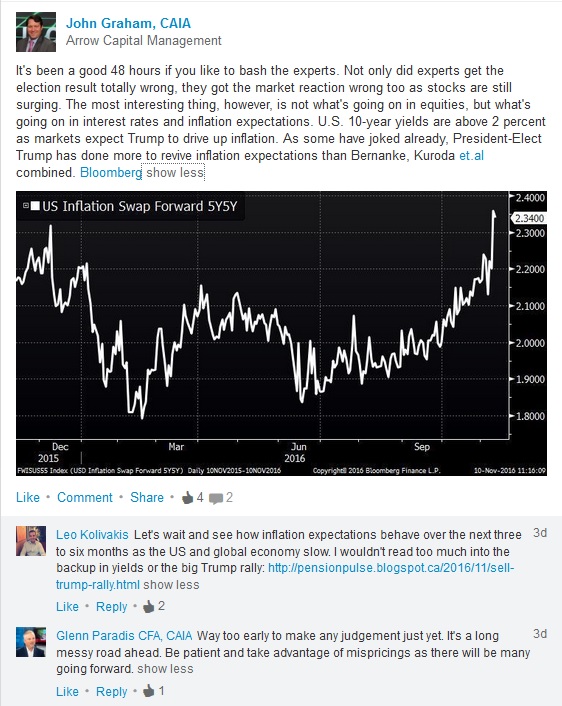

What I find quite amazing is how Trump’s victory has done more to raise inflation expectations than all the world’s powerful central bankers combined, something John Graham of Arrow Capital Management noted on LinkedIn last week after the election (click on image):

You’ll notice my comment to his post and that of Glenn Paradis basically questioning how sustainable the rise in inflation expectations is going forward.

Why is this important? Because as I noted in my recent comments on sell the Trump rally and whether Trump is bullish for emerging markets, it’s far from clear what Trump’s election means for global deflation going forward.

As I keep warning, another crisis in emerging markets is deflationary, and investors need to keep an eye on the surging US dollar index (DXY) which just crossed 100, a key level of resistance (click on image):

I warned my readers to ignore Morgan Stanley’s warning that the greenback was set to tumble back in August and think the trend is continuing in large part due to Trump’s campaign proposal to slash taxes on cash US companies have stashed outside of the country, all part of his corporate repatriation plan.

The key thing to keep in mind is the surging greenback has the potential to disrupt and wreak more deflationary havoc on emerging markets (especially commodity producers) and clobber the earnings of US multinational corporations.

A surging US dollar will also lower US import prices, effectively importing global deflation to the United States, and if it continues, it might jeopardize that much anticipated Fed rate hike in December, especially after October’s Fed game changer which signaled the US central bank is ready to err on the side of inflation, staying accommodative for far longer than markets anticipate.

I think a lot of attention is spent on Trump’s fiscal plan to stimulate the US economy through massive infrastructure program, which is a great idea, especially if he attracts US, Canadian and global pensions into the mix, lowering the cost of this program.

A lot less attention is being placed on what Trump’s presidency means for emerging markets, the US dollar and global deflation going forward. Admittedly, I’m struggling to make sense of all this because it’s not entirely clear to me that President Trump will follow through with a lot of his more contentious campaign proposals regarding trade agreements.

In fact, like millions of others, I watched President-elect Trump on 60 Minutes Sunday evening, and found him a lot more sober, serious, subdued — and dare I say, a lot humbler — than the brash and arrogant candidate we were accustomed to.

At one point, he and his daughter Ivanka emphasized the needs of the country are far more important than the “Trump brand.” I made the mistake of tweeting my thoughts on the interview and got all these die-hard Hillary Clinton supporters on my case (click on image):

Even my mother called from London this morning to tell me “how terrible it is that Trump was elected” and that “Hillary was so much better than him in the debates.”

Like a good son, I listened patiently as she went on and on praising Hillary Clinton but at one point I had enough and politely interjected: “Mom, it’s over, for a lot of reasons Hillary Clinton lost and Trump will be the next US president. Take the time to watch his 60 Minutes interview, you’ll see his focus is on jobs and the economy, not on abortion and other divisive issues” (as I predicted).

[Note: My brother and I believed Bernie Sanders had a much better chance than Hillary Clinton to defeat Trump because he too tapped into voters’ anxieties about jobs and trade deals and he had a full-blown grass roots movement which was gaining momentum. But it will be a day in hell before America’s power elites accept a “socialist” like Bernie as their next leader; they’d rather a “nut” like Trump in power as he will cut taxes and bolster their power hold.]

One thing that is for sure, last week was a great week for savers, 401(k)s and global pensions. The Dow chalked up its best week in five years and stocks in general rallied led by banks and my favorite sector, biotechs which had its best week ever.

More importantly, bond yields are rocketing higher and when it comes to pension deficits, it’s the direction of interest rates that ultimately counts a lot more than any gains in asset values because as I keep reminding everyone, the duration of pension liabilities is a lot bigger than the duration of pension assets, so for any given move in rates, liabilities will rise or decline much faster than assets.

Will the rise in rates and gains in stocks continue indefinitely? A lot of underfunded (and some fully funded) global pensions sure hope so but I have my doubts and think we need to prepare for a long, tough slug ahead.

The 2,826-day-old bull market could be a headache for Trump but the real headache will be for global pensions when rates and risk assets start declining in tandem again. At that point, President Trump will have inherited a long bear market and a potential retirement crisis.

This is why I keep hammering that Trump’s administration needs to include US, Canadian and global pensions into the infrastructure program to truly “make America great again.”

Trump also needs to carefully consider bolstering Social Security for all Americans and modeling it after the (now enhanced) Canada Pension Plan where money is managed by the Canada Pension Plan Investment Board. One thing he should not do is follow lousy advice from Wall Street gurus and academics peddling a revolutionary retirement plan which only benefits Wall Street, not Main Street.