Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Keith Ambachtsheer and Edward Waitzer wrote an op-ed for the Globe and Mail, Ontario’s pension plan presents a game-changing opportunity:

There is evidence that an element of employer compulsion is required to ensure that Canada’s private-sector workers are covered by a functional workplace pension plan. That reality should be tempered by careful thought about strategies to minimize the potential negative impacts of compulsion.

One strategy is to encourage healthy private-sector competition through the “comparable plan” principle that Ontario has adopted in its Ontario Retirement Pension Plan (ORPP) initiative. Competition could foster much-needed innovation in workplace pension design and management in Canada, and is an opportunity for the financial sector to assert its social utility.

A 1994 World Bank study suggested that the ideal national retirement income system has three pillars: a universal pillar providing a basic pension to all, a workplace-based pillar providing supplementary retirement income and an individualized pillar permitting people to create their own “add-on” piece. This model flags a serious Canadian problem. More than three-quarters of Canada’s private-sector work force has no access to a well-designed, cost-effective workplace plan. This means many are undersaving and thus will not achieve their retirement income aspirations. Others will fall short because they are saving inefficiently through high-cost investment vehicles.

These consequences impose significant costs on future generations. One solution is to expand the Canada Pension Plan/Quebec Pension Plan or another provincial version. Specifically, Ontario’s ORPP initiative was announced in 2014 and the ORPP Act was passed in 2015. As an alternative solution, we proposed in 2011 requiring employers to enroll their employees into a qualifying pooled registered pension plan (PRPP) offered by an approved financial institution.

The ORPP Act contemplated these solutions by requiring Ontario employers to enroll workers into the ORPP or offer a “comparable plan.” Current wording leaves room for interpretation of what that is. This window creates a private-sector opportunity for competition with the ORPP. It could also pre-empt the need for future CPP/QPP expansion if other provinces also require “comparable plans.”

What should a 21st-century workplace pension plan look like? It has (a) the ability to compound returns over long investment periods to make a decent pension affordable, (b) the ability to provide lifetime payment assurance and (c) a transition mechanism that shifts plan participant exposure from return compounding emphasis to payment safety emphasis as they age.To date, very few countries have been able to offer access to this kind of workplace plan due to lack of innovation and outmoded legislation and regulation.

Fortunately, there is a global effort under way to address these barriers. Northern European countries, Britain and Australia have already made workplace pension-plan participation mandatory. Ontario leads the way in North America, but Saskatchewan has been offering its Saskatchewan Pension Plan since 1986. (The SPP offers most of the 21st-century plan features set out above, but because participation has been voluntary, it lacks the scale to be truly cost effective.)

Ontario’s commitment to the ORPP can be a game-changer for Canada. It creates the opportunity for financial institutions to offer SPP-type plans from coast to coast, and even beyond Canada’s borders. Let’s call them PRPPs. Here’s how they could compete with the ORPP:

The target pension benefit: A PRPP would be comparable to the ORPP’s target benefit at the ORPP’s 3.8-per-cent contribution rate. However, with the PRPP, the employer would have the option of choosing a higher target benefit with a higher contribution rate.

Risk mitigation: The PRPP design recognizes that the major risk facing workers is lack-of-return compounding risk, and the major risk facing retirees is payment-for-life uncertainty. This leads logically to its two-instrument approach. We understand that the ORPP design will not distinguish between the differing risk preferences of workers and retirees.

Wealth transfers: The PRPP design ensures that no systematic wealth transfers take place between current and future workers, retirees and taxpayers. To date, it is unclear how the ORPP will ensure this.

Open architecture: The PRPP will be able to accept already accumulated retirement savings and move them into the same return compounding-to-safety life-cycle process as will be used for new pension contributions. Our understanding is that the ORPP will not.

Surely employers and employees would benefit from the option of a PRPP with the features sketched out above.

A final thought. Leadership by policy makers and financial institutions can help demonstrate that regulation is about more than protecting consumers from deceptive products and practices. Rather, it is to ensure that society is well served and that consumers get “value for money” – a fair deal. This should encourage financial innovation (as a substitute for government market intervention) and a better articulation of public stewardship responsibilities throughout the financial services supply chain.

*** Keith Ambachtsheer is director emeritus of the International Centre for Pension Management at the Rotman School of Management, University of Toronto. Edward Waitzer holds the Jarislowsky Dimma Mooney Chair in Corporate Governance, is director of the Hennick Centre for Business Law at Osgoode Hall Law School and the Schulich School of Business, York University, and is a senior partner at Stikeman Elliott LLP.

This article is based on a KPA Advisory Services paper.

Keith Ambachtsheer and Edward Waitzer have written an interesting article but I have one big beef with it which I will come to shortly.

First, I agree with them, the Ontario Retirement Pension Plan (ORPP) is a game changer but not for the main reasons they cite. I think it’s a game changer because absent a push by all provinces to enhance the CPP once and for all, Ontario is right to introduce a new supplementary pension plan which can use the same successful model of other large Ontario plans to provide a supplementary pension to all Ontarians.

My biggest beef with this article is that it focuses too much on how the ORPP will encourage more private sector competition, neglecting to mention that when it comes to pensions, there is no private sector pension solution that can effectively compete with Canada’s Top Ten pensions.

Ambachtsheer and Walzer are both very smart, they know their stuff when it comes to pensions, but they missed a golden opportunity here to explain why the ORPP makes great long-term sense and why it will benefit the entire population and economy for years to come.

To be fair, they mention it en passant but then move right away to obsessively focus on how it will promote private competition. No it won’t, the ORPP will kill its private sector competitors over a very long period. Why? Because they won’t be able to do half the things the ORPP will be doing at a fraction of the cost. That is the honest truth and both Ambachtsheer and Waitzer know it.

Go back to read my comment on less bang for your CPP buck where I rip apart the latest study from the Fraser Institute to make the point why enhancing the CPP is the only real option to bolstering Canada’s retirement system.

Absent an enhanced CPP, it makes sense for Ontario to introduce a new supplementary pension plan, but not for the main reason cited by the authors above. We already have something in Canada that works, let’s build on the success of our large, well-governed defined-benefit plans and drop the notion (more like charade) that the private sector can effectively compete against them. It can’t and the sooner we realize this, the better off all Canadians will be.

You can watch a BNN clip of Ontario Finance Minister Charles Sousa discussing why the ORPP is an important initiative at the end of the Globe and Mail article here. Great discussion, listen to his comments.

Below, Ron Mock, CEO of Ontario Teachers’ Pension Plan, Canada’s largest single profession pension plan, talks about the fund’s investment strategy in a recent interview on CNBC.

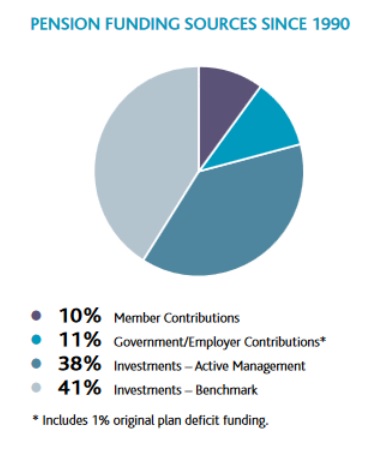

As I stated in my comment when I went over Ontario Teachers’ 2015 results, there is one chart I really like in the Annual Report, one that exemplifies Teachers’ long-term performance (click on image):

When people ask me why I’m such a stickler for large, well-governed defined-benefit plans, I point out charts like the one above to make my case. If you’re looking for a solution to the global retirement crisis, this is it, right there in that chart.

Trust me, no PRPP can compete with OTPP or Canada’s Top Ten when it comes to producing great long-term returns on a cost efficient basis. The sooner we recognize this, the better off all Canadians will be.