Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Brett Shipp of WFAA reports, Dallas police, fire pension board facing disaster:

The past month has been an emotional roller coaster for Dallas police and firemen. Thursday afternoon, the bad news continued.

The Dallas Police and Fire Pension System is a billion dollars in the red, and the plan to bail the system out is already being called “unacceptable” by some.

The bailout plan, unveiled Thursday, is a proposal that police and fire employees knew was coming. But the fact is, the Dallas Police and Fire Pension System is actually closer to $2 billion in the hole.

If things keep going the way they are going, the pension fund will be broke by 2030. That’s why consultants unveiled the bailout plan, which one police veteran called so drastic he believes it will be voted down by rank-and-file.

The plan calls for dramatic reductions in cost-of-living adjustments and deferred retirement option plans, also known as the drop program.

What’s more, the City of Dallas would immediately have to contribute $600 million into the fund just to keep it solvent.

“There is no choice. There have to be deep cuts,” said pension fund board member and Dallas City Council member Phillip Kingston. “We tried to make them the least painful as possible. There have to be deep cuts and there is no guarantee the city is going to love contributing the amount that being asked.”

The pension fund got into trouble after former administrators made millions of dollars in risky real estate investments. Some of those administrators and advisors are reportedly now under federal investigation.

The pension system is in such bad shape pension system officials says dramatic cuts must be made beginning this October.

Tristan Hallman of the Dallas Morning News also reports, Can Dallas Police and Fire Pension fund be saved? Officials propose changes to head off insolvency:

Jim Aulbaugh, a battalion chief for Dallas Fire-Rescue, is skeptical of any attempts to save his and his colleagues’ pensions.

“I don’t think it will make any difference,” said Aulbaugh, a 33-year veteran. “It’s a sinking ship that can’t be saved.”

But Dallas Police and Fire Pension Fund board members still believe they can salvage the system. And on Thursday, they unveiled a new plan built mostly on big cuts, new revenue and the hope that the city will pump new money into the fund.

Firefighters and cops, who are rallying for higher salaries at City Hall, understand that their retirements are in jeopardy. The pension system, set back by significantly overvalued real estate investments, is hurtling toward insolvency by 2030.

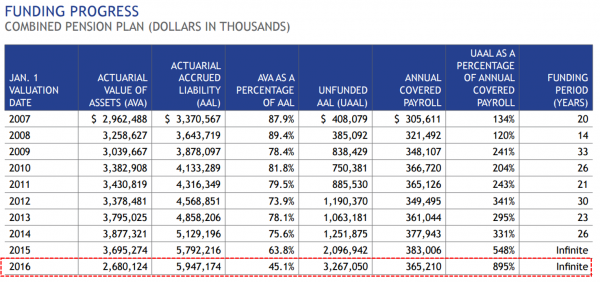

The fund has $3.27 billion in unfunded liabilities and less than $2.7 billion in assets — a funding ratio of 45 percent. Pensions are generally thought to be in danger if their funding ratio is less than 80 percent. The fund would need its members and the city to double their contributions to meet its requirements.

Texas Pension Review Board Chairman Josh McGee said the fund is “in a world of hurt” and is unaware of a state pension system in worse shape.

“It’s going to take shared sacrifice from all sides to actually fix the system,” he said. “That’s going to be difficult.”

The proposals represented pension system officials’ first concrete steps at comprehensive fixes.

Kelly Gottschalk, the system’s executive director, said the fund’s proposals would solve nearly two-thirds of the funding problem.

The most significant proposal is adding restrictions to the Deferred Retirement Option Program, better known as DROP. The program allows veteran officers and firefighters to “retire” in the eyes of the system, but continue working for their paychecks while their pension checks are sent to a separate investment fund. They pay a fee of 4 percent of their paychecks, less than the 8.5 percent contribution they’d make otherwise.

DROP gave recipients an 8 percent to 10 percent annual return even while the system earned significantly less. And actual retirees can keep their money in DROP indefinitely, accruing interest, and withdraw it whenever they want. That makes up $1 billion of the fund’s money.

The proposal won’t end that practice because the system needs the money. But it will tie it to Treasury bond yields.

That plan, if approved, will probably force cops and firefighters to either retire sooner or stay in the normal fund longer. Once in DROP, members could earn a 3 percent interest rate for seven years. Then, the money will earn nothing until they retire.

The plan will trim cost-of-living increases, base payments on a five-year highest-salary average rather than three years, and raise all members’ contributions to 9 percent. DROP recipients will have their contributions refunded when they withdraw.

Members must approve the plan. So officials also restored reduced benefits for officers hired in the last few years in return for the cuts.

Officials hope the city will join them in a request to increase the contributions on both sides. That means millions more taxpayer dollars would be sunk into the fund. The city currently contributes the maximum allowed percentage, which will amount to roughly $118 million this fiscal year.

Jim McDade, president of the Dallas Fire Fighters Association, said he hopes members and the city will do what it takes. Benefits are important, he said. Dallas cops and firefighters don’t pay into or receive Social Security.

“In the end, we have to save our pension,” he said.

Police Lt. Ernest Sherman, a 26-year veteran, said he doesn’t mind the proposed cuts.

“If the changes have to be made for the betterment of the pension, I’ll be fine,” he said.

But he said pension officials should have been more frank about the pension fund’s troubles. He said the hopefulness sounded like all the other proposed fixes he has heard over the years.

And he fears that all the changes may not be enough. Gottschalk worries that the proposals will cause a run on the system by DROP members like Aulbaugh, the battalion chief, who said he’s considering it.

Even if there is no run, the pension fund may even have a difficult time meeting its now-lower annual investment return target of 7.25 percent. And another economic downturn could hurt the system further.

“I don’t know how you save a system like that except with steep cuts and big increases in contributions,” said Steve Malanga, a senior fellow who studies pensions at the conservative research group Manhattan Institute. “Even so, the risk will remain very high for years to come.”

Zero Hedge provided more background and analysis in its comment, Dallas Cops’ Pension Fund Nears Insolvency In Wake Of Shady Real Estate Deals, FBI Raid (added emphasis is ZH):

The Dallas Police & Fire Pension (DPFP), which covers nearly 10,000 police and firefighters, is on the verge of collapse as its board and the City of Dallas struggle to pitch benefit cuts to save the plan from complete failure. According the the National Real Estate Investor, DPFP was once applauded for it’s “diverse investment portfolio” but turns out it may have all been a fraud as the pension’s former real estate investment manager, CDK Realy Advisors, was raided by the FBI in April 2016 and the fund was subsequently forced to mark down their entire real estate book by 32%. Guess it’s pretty easy to generate good returns if you manage a book of illiquid assets that can be marked at your “discretion”.

To provide a little background, per the Dallas Morning News, Richard Tettamant served as the DPFP’s administrator for a couple of decades right up until he was forced out in June 2014. Starting in 2005, Tettamant oversaw a plan to “diversify” the pension into “hard assets” and away from the “risky” stock market…because there’s no risk if you don’t have to mark your book every day. By the time the “diversification” was complete, Tettamant had invested half of the DPFP’s assets in, effectively, the housing bubble. Investments included a $200mm luxury apartment building in Dallas, luxury Hawaiian homes, a tract of undeveloped land in the Arizona desert, Uruguayan timber, the American Idol production company and a resort in Napa.

Despite huge exposure to bubbly 2005/2006 vintage real estate investments, DPFP assets “performed” remarkably well throughout the “great recession.” But as it turns out, Tettamant’s “performance” was only as good as the illiquidity of his investments. We guess returns are easier to come by when you invest your whole book in illiquid, private assets and have “discretion” over how they’re valued.

In 2015, after Tettamant’s ouster, $600mm of DPFP real estate assets were transferred to new managers away from the fund’s prior real estate manager, CDK Realty Advisors. Turns out the new managers were not “comfortable” with CDK’s asset valuations and the mark downs started. According to the Dallas Morning News, one such questionable real estate investment involved a piece of undeveloped land in the Arizona desert near Tucson which was purchased for $27mm in 2006 and subsequently sold in 2014 for $7.5mm. Per the DPFP 2015 Annual Report:

In August 2014, the Board initiated a real estate portfolio reallocation process with goals of more broadly diversifying the investment manager base and adding third party fiduciary management of separate account and direct investment real estate assets where an investment manager was previously not in place. The reallocation process resulted in the transfer of approximately $600 million in DPFP real estate investments to four new investment managers during 2015. The newly appointed managers conducted detailed asset-level reviews of their takeover portfolios and reported their findings and strategic recommendations to the Board over the course of 2015 and into 2016. A significant portion of the real estate losses in 2015 were a direct result of the new managers’ evaluations of the assets.

Then the plot thickened when, in April 2016, according the Dallas Morning News, FBI raided the offices of the pension’s former investment manager, CDK Realty Advisors. There has been little disclosure on the reason for the FBI raid but one could speculate that it might have something to do with all the markdowns the pension was forced to take in 2015 on its real estate book. At it’s peak, CDK managed $750mm if assets for the DPFP.

With that background, it’s not that difficult to believe that DPFP’s actuary recently found the plan to be in serious trouble with a funding level of only 45.1%. At that level the actuary figures DPFP will be completely insolvent within the next 15 years. Plan actuaries estimate that in order to make the plan whole participants and/or the City of Dallas would need to contribute 73% of workers’ total comp for the next 40 years into the plan…seems reasonable.

According to an article published by Bloomberg, a subcommittee of the pension’s board recently submitted a proposal that would at least help prolong the life of the fund. The subcommittee proposal calls for cost of living adjustments to be reduced from 4% to 2% while participants would be expected to increase their contributions to the plan. Of course, taxpayers were asked to also provide “their fair share” equal to roughly $4mm in extra plan contributions per year, a request that would likely require the approval of the Texas legislature. If approved, the proposal is anticipated to keep the plan solvent through 2046…at which point we assume they’ll go back to taxpayers for more money?

A quick look at the plan’s 2015 financial reports paints a pretty clear picture of the plan’s issues.

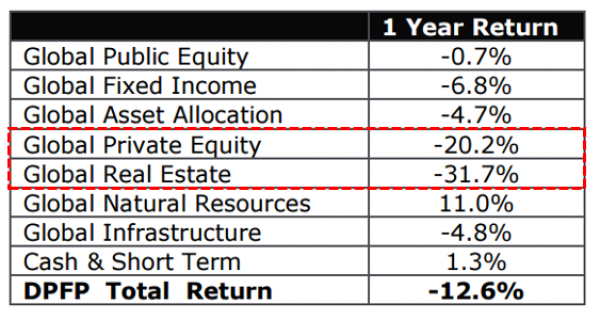

Starting on the asset side of the balance sheet, and per our discussion above, DPFP was forced to mark down it’s entire real estate book by 32% in 2015. Private Equity investments were also marked down over 20% (click on image).

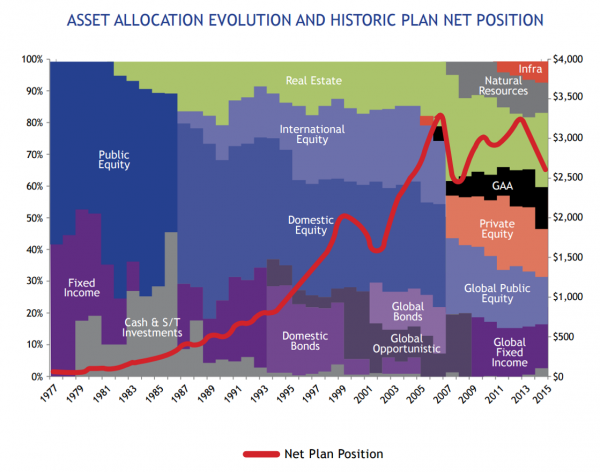

This came as over 50% of the assets were diverted into illiquid real estate and private equity investments back in 2006 (click on image).

But asset devaluations aren’t the only problem plaguing the DPFP. As we recently discussed at great length in a post entitled “Pension Duration Dilemma – Why Pension Funds Are Driving The Biggest Bond Bubble In History,” another issue is DPFP’s exposure to declining interest rates. Per the table below, a 1% reduction in the rate used to discount future liabilities would result in the net funded position of the plan increasing by $1.7BN (click on image).

And of course the typical pension ponzi, whereby in order to stay afloat the plan is paying out $2.11 for every $1.00 it collects from members and the City of Dallas effectively borrowing from assets reserved to cover future liabilities (which are likely impaired) to cover current claims in full. This “kick the can down the road” strategy typically ends badly for someone…like most public pension ponzis we suspect this one will be most detrimental to Dallas taxpayers.

All of which leaves the DPFP massively underfunded…an “infinite” funding period seems like a really long time, right?

Since when did Zero Hedge become experts on pensions? Some of the stuff they write in their analysis is spot on but other stuff is totally laughable, like pensions causing the biggest bond bubble in history (Note to Zero Hedge: There’s no bond bubble, it’s called deflation stupid! And go back to school to understand the evolution asset-liability management and why in a deflationary environment, bonds are the ultimate diversifier).

Unlike Zero Hedge, I don’t take issue with the asset allocation of the Dallas Police and Fire Pension (DPFP) but rather in the shady, non-transparent way that they run their operations.

I can sum up the biggest problem at DPFP in three words: Governance, Governance and GOVERNANCE!!!!!!!!!!

I’m sick and tired of covering US public pensions with such awful governance and when disaster strikes, everyone blames public pensions and wants to dismantle them.

Folks, the pension Titanic is sinking, and what we’re seeing in Dallas, Chicago, Detroit, Tampa Bay, will be playing out in many US cities when the chicken comes home to roost.

When disaster struck Greece, and there was no money left to pay public pensions, they had to drastically cut benefits. Of course, this being Greece, it’s business as usual for Tsipras et al. as his government is increasing the civil service and turning a blind eye to undeclared income which now stands at 25% of GDP (I think it’s more like 50%).

In the United States, once public pensions go insolvent, sure, benefits will be cut and contributions will be increased but taxpayers will also be called upon to shore them up in the form of soaring property taxes and utility rates.

Instead of amalgamating city and municipal pensions at the state level and fixing the governance to manage more assets in-house, they’re introducing one Band-Aid solution after another.

As far as Dallas Police and Fire Pension, it’s a disaster and a real shame because not only is police morale low following the heinous shootings that rocked that city, now a lot of police officers and fire fighters are asking themselves whether they can count on their pension to be there when they retire.

I love Dallas. It’s a beautiful city. I visited it on a business trip back in 2004 when I was working at PSP Investments. I went with Asif Haque who now works at CAAT pension and Russell (Rusty) Olson, the former pension director of Kodak’s pension fund and author of. We visited funds there and then drove to Houston which was nice but nowhere near as nice as Dallas (in my opinion).

Anyways, I don’t know how Dallas is now but it’s sad to see their police and fire pension on the verge of insolvency. In my opinion, this pension desperately needs the services of a Rusty Olson (don’t know if he’s still alive and kicking), a Ted Siedle (aka the pension proctologist) or even Harry Markopolos, the man who exposed the fraud at Madoff’s multi-billion hedge fund Ponzi and author of No One Would Listen (great book, a must read).

At the very least — and this is friendly, unsolicited advice — the DPFP should contact my friends at Phocion Investment Services and make sure their performance, risk and operations are being run properly and compliant with the highest standards.

In fact, if I was the sponsor or member of this pension plan, I would be demanding a comprehensive investment and operational risk audit of all activities at the Dallas Police and Fire Pension by an independent and qualified third party. And I’m not talking about the standard audit from a chartered accounting firm that basically signs off on activities.

[As an aside, back in 2004, I was elected to sit on the Board of the Hellenic Community of Montreal and the first thing I demanded was to hire a forensic accounting firm to go over all the books. I trusted nobody and refused to sign off on anything if the books weren’t properly audited by real experts who know how to uncover shady dealings. Things drastically improved since then, or so I hear.]

As far as investments go, one infrastructure expert shared this with me when it comes to the infrastructure investments at the Dallas Police and Fire Pension:

“[It’s] a true ‘mess’ in the US pension world. I met one of their investment team a couple years ago and learned that their infrastructure allocation was being used to fund extremely risky managed lanes toll roads in Dallas. Speaks to importance of picking the right advisors and investments when making an illiquid allocation”

When I pressed him on what exactly he meant by “extremely risky managed lanes toll roads in Dallas,” he elaborated and shared this with me:

As of 2015, their infrastructure investments were as per below (click on image).

Notwithstanding allocating all your infrastructure allocation investments to one manager (JPM is good but 1 – too much manager concentration, 2 – maritime and Asian infra are high risk strategies that should only form a small part of a diversified infra/real asset program), their co-investments in LBJ Express and North Tarrant are in managed lanes.

Managed lanes utilize variable tolling, to optimize traffic flow. They are constructed next to the free alternative and will change their tolls on a frequent basis based on prevailing traffic conditions on the free alternative. For example, if there is an accident or it is during rush hour, these lanes will increase their tolls as more drivers want to use them.

As anyone in infrastructure knows, forecasting traffic for regular toll roads or airports is much more of an art than a science so you could surmise just how extremely difficult it is to forecast and manage these types of managed lane investments. Definitely not for beginners or inexperienced US plans such as Dallas Police.

http://www.bloomberg.com/news/articles/2015-09-17/drivers-decry-rise-of-toll-lanes-as-texas-s-lbj-expressway-opens

Given what the article above mentions regarding Dallas’ real estate investments, I am not surprised. Scary to think about though and by the time it gets back to the Police, they are the losers and it is not fair. See the attachment on them selling their stakes in these investments, probably at the worst possible time.

If you would like to quote, please keep anonymous. When I read about this though it reinforces if US plans think they are going to make wise illiquid infrastructure investment decisions without someone experienced on their side or in house, they will prove disappointed. And the traditional GPs are definitely not fully on their side.

This person knows what he’s talking about and he’s right, the traditional GPs are definitely not on their side.

If you would like to contact me to discuss this comment, feel free to shoot me an email at LKolivakis@gmail.com and I’ll be happy to discuss my thoughts.

Lastly, you can read The Long-Term Financial Stability Sub-Committee’s presentation to the full Board at the August 11th Board Meeting by clicking here.