Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Benefits Canada reports, Ontario Teachers’ acquires U.S. oil and gas assets:

The Ontario Teachers’ Pension Plan – along with RedBird Capital Partners and Aethon Energy Management – will acquire J-W Energy’s assets in north Louisiana and northeast Texas.

Redbird, a North American-based principal investment firm, and Aethon, a Dallas-based onshore oil and gas investor, have partnered with the pension plan to purchase oil and gas upstream and midstream assets. Additional assets obtained in the partnership will be combined with the J-W assets to form a joint group, Aethon United.

“We are looking forward to partnering with Aethon, a proven firm with an exceptional track record and strong alignment with Ontario Teachers’, as well as expanding our strategic relationship with RedBird,” said Jane Rowe, senior vice-president of private capital at Ontario Teachers’. “These assets are a strong fit with our private equity energy portfolio and represent a compelling investment opportunity with an established base of long-life proven reserves and attractive growth opportunities.”

The Texas and Louisiana properties comprise approximately 84,000 acres and 380 miles of gathering and processing infrastructure which, added to Aethon United’s existing assets, results in a 350,000 net acres, the other portion of which is made up from previous deals with Encana, Noble Energy and SM Energy.

Ontario Teachers’ put out a press release on this deal:

Ontario Teachers’ Pension Plan (“Ontario Teachers'”) RedBird Capital Partners (“RedBird”), and Aethon Energy Management (“Aethon”) today announced the acquisition of J-W Energy’s (“J-W”) oil & gas upstream and midstream assets located in northeast Texas and north Louisiana. Additionally, Haynesville and Rockies assets acquired in partnership by Aethon and Redbird are being consolidated with the J-W assets, forming a joint partnership (“Aethon United”).

Located in north Louisiana and northeast Texas, the J-W Energy assets comprise approximately 84,000 net acres and 380 miles of associated gathering and processing infrastructure. The collective reserve base of the J-W assets combines low risk, long life, and highly predictable production with attractive development opportunities.

With this acquisition, Aethon United now operates in excess of 350,000 net acres and 166 MMcfe/d of production. In addition to the J-W Energy assets, Aethon United operates approximately 91,000 net acres in the Haynesville previously acquired from SM Energy and Noble Energy, as well as approximately 181,000 net acres in the Wind River Basin of Wyoming previously acquired from Encana.

Albert Huddleston, Founder & Managing Partner of Aethon, commented, “We are excited to partner with Ontario Teachers’ and continue our long-standing partnership with RedBird to acquire J-W Energy’s high quality, low risk, unconventional assets, which continues to expand our acreage in the Arkansas-Louisiana-Texas area. The J-W Energy assets help to diversify and expand our existing portfolio, and highlights Aethon’s ability to identify attractive E&P assets, offering strong risk-adjusted returns in the current market environment and in the future. We are grateful for the confidence shown in the Aethon Energy team for the series of investments in partnership with us by noted investors Ontario Teachers’ and RedBird, which ratifies our 26 year track record.”

“We are looking forward to partnering with Aethon, a proven firm with an exceptional track record and strong alignment with Ontario Teachers’, as well as expanding our strategic relationship with RedBird” said Jane Rowe, Senior Vice President of Private Capital. “These assets are a strong fit with our private equity energy portfolio and represent a compelling investment opportunity with an established base of long-life proven reserves and attractive growth opportunities.”

“Aethon has been a tremendous partner with RedBird in the build-up of our collective energy investments, and we’re excited to expand this partnership with our friends at Ontario Teachers’ with whom we have a very strong strategic relationship,” said Hunter Carpenter, Partner at RedBird Capital. “This partnership is an example of RedBird’s unique ability to identify proven owners and entrepreneurs like Aethon Energy who are frequently unavailable to traditional institutional capital. Aethon Energy represents a rare combination of investing and operating expertise providing superior historical performance and operating skill.”

About Aethon Energy Management

Aethon Energy Management LLC is a Dallas-based private investment firm that has managed and operated over $1.6 billion of assets, and is focused on direct investments in North American onshore oil & gas. Since its inception in 1990, Aethon has maintained a focus on acquiring under-appreciated assets where opportunities exist to add value through lower-risk development, operational enhancements and Aethon’s proprietary technical knowledge. Aethon’s 26-year track record spans multiple energy cycles and has consistently provided compelling asymmetric returns for its institutional and high net worth investors through disciplined buying and value creation. For more information, go to www.AethonEnergy.com.

About Ontario Teachers’

The Ontario Teachers’ Pension Plan (Ontario Teachers’) is Canada’s largest single-profession pension plan, with $171.4 billion in net assets at December 31, 2015. It holds a diverse global portfolio of assets, 80% of which is managed in-house, and has earned an annualized rate of return of 10.3% since the plan’s founding in 1990. Ontario Teachers’ is an independent organization headquartered in Toronto. Its Asia-Pacific region office is located in Hong Kong and its Europe, Middle East & Africa region office is in London. The defined-benefit plan, which is fully funded, invests and administers the pensions of the province of Ontario’s 316,000 active and retired teachers. For more information, visit www.Otpp.com and follow us on Twitter @OtppInfo.

About RedBird Capital Partners

RedBird Capital Partners is a North America based principal investment firm focused on providing flexible, long-term capital to help entrepreneurs grow their businesses. Based in New York and Dallas, RedBird seeks investment opportunities in growth-oriented private companies in which its capital, investor network and strategic relationships can help prospective business owners achieve their corporate objectives. RedBird’s private equity platform connects patient capital with business founders and entrepreneurs to help them outperform operationally, financially and strategically. For more information, go to www.RedBirdCap.com.

J-W Energy Company also put out a press release on this deal:

J-W Energy Company is pleased to announce the closing on July 1, 2016 of the sale of substantially all of the oil and gas assets owned by J-W Operating Company and substantially all of the midstream assets owned by J-W Midstream Company to affiliates of Aethon United LP. The assets included in the transaction are located mainly in the North Louisiana and North Texas areas and are comprised of approximately 95,000 net acres and 380 miles of associated gathering and processing infrastructure. The sale is an exit from the upstream and midstream business by J-W Energy Company, which will continue to own the largest privately-held compression fleet in the U.S. through its wholly-owned subsidiary, J-W Power Company. Over the past ten years, J-W Energy has exited from its drilling, valve manufacturing, gas measurement and wireline businesses as well, as part of a planned reallocation of company resources.

“This exit from the upstream and midstream businesses will allow J-W Energy Company to focus on our compression business, which has been less capital intensive than the upstream and midstream businesses. Despite this sale marking the end of J-W Energy’s long and successful history in the upstream and midstream businesses, we are confident that the dedicated employees of J-W Operating and J-W Midstream will be instrumental in the future success of this endeavor,” said David A. Miller, President of J-W Energy Company.

Wells Fargo Securities, LLC served as the exclusive financial advisor to J-W Energy on the transaction.

You can also read more about J-W Midstream Company here:

J-W Midstream Company is a natural gas gathering and processing company that has been active in the gathering, dehydration, treating, processing and transmission of natural gas for over thirty years. With that experience, we understand the producer’s need for high quality, cost-effective, completely reliable services.

From engineering and construction to contract gathering and processing, J-W Midstream Company is committed to providing a continuously uninterrupted flow of gas to our customers and real value to their bottom lines.

J-W Midstream Company operates more than 400 miles of natural gas pipeline systems in Louisiana and Texas, as well as processing facilities that range from small refrigeration and J-T skids to 25 MMSCFD cryogenic units.

Through an affiliate company, J-W Midstream Company can supply outsourced gas sales and other gas management functions.

So, what is this deal all about and why is Ontario Teachers’ partnering up with Aethon Energy and RedBird Capital to buy J-W Energy Company’s upstream and midstream businesses?

This is how private equity works. J-W Energy is a private company which is an industry leader in the leasing, sales and servicing of natural gas compression equipment, in both standard and custom packages. It has been leasing compressor and compressor/maintenance packages for more than 40 years.

The company was looking to exit its upstream and midstream businesses to focus on its core business which is the compression business. Once this opportunity presented itself, Aethon, RedBird and Ontario Teachers’ pounced to act quickly and acquire these assets.

This was a co-investment where Teachers’ invested a substantial amount alongside its partners and didn’t pay any fees. Along with Atheon and RedBird, Teachers’ will look to develop J-W Energy’s upstream and midstream businesses and because it’s a pension with a very long investment horizon, it doesn’t have the pressure that a traditional private equity fund has to unlock value of these business units during three or four years.

In other words, the deal is a win for J-W Energy Company and if Teachers’ and its partners succeed in improving the operations of the upstream and midstream businesses over the next five to ten years, it will be a win for them, the employees of these businesses and of course, Teachers’ contributors and beneficiaries.

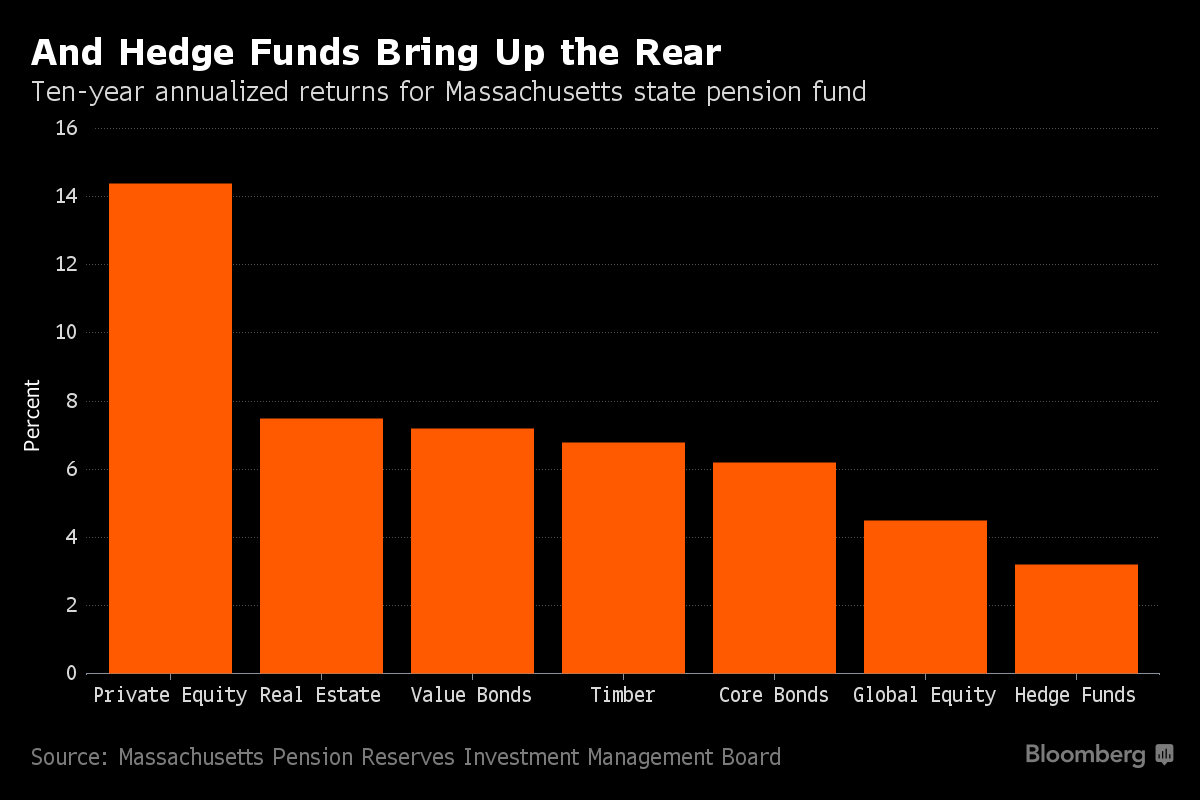

Why invest in energy now? Last December, I wrote a comment on why Canada’s pensions are betting on energy and in November of last year, I met up with AIMCo’s president Kevin Uebelein here in Montreal on the day they announced a major transaction buying a $200M stake in TransAlata’s renewable energy business.

When it comes to energy, focus on what Jane Rowe said in the press release: “These assets are a strong fit with our private equity energy portfolio and represent a compelling investment opportunity with an established base of long-life proven reserves and attractive growth opportunities.”

When you are a pension the size of an Ontario Teachers’ you will seek attractive opportunities in down-beaten sectors across public and private markets and use your long investment horizon to realize big gains. This is a competitive advantage all of Canada’s large pensions have over traditional private equity funds, namely, they have very deep pockets and a much longer investment horizon to ride out short-term cyclical swings.

Teachers’ isn’t the only large Canadian pension looking to capitalize on energy opportunities. Lincoln Brown of Oilprice.com reports, Two Pension Fund Groups Bid for TransCanada’s $2B Mexican Pipeline:

A TransCanada Mexican pipeline is drawing significant interest from pension funds. Canada Pension Plan Investment Board, Public Sector Pension Investment Board and Borealis Infrastructure Corp. have created a consortium in order to purchase up to 49.9 percent of the business, which has been estimated to be worth some US$2 billion.

Caisse de Depot et Placement du Quebec’s new Mexican joint venture, CKD Infraestructura Mexico SA, are also interested in purchasing stakes, along with three other unnamed businesses.

That information comes from a source with knowledge of the situation who spoke to Bloomberg but asked not to be identified. TransCanada spokesman Mark Cooper has confirmed the company is seeking investors but would not comment beyond that. The Calgary-based company is trying to sell its minority stake in the pipeline, along with power plants in the northeastern United States to generate cash to buy Columbia pipeline Group Inc. That deal is estimated at US$10.2 billion.

Mexico is increasingly drawing the attention of investors. The country recently began a US$411 billion plan for its infrastructure, focusing on transportation and energy. Canada Pension and the Ontario Teacher’s Pension Plan already made an investment last month in a toll road operator in Mexico.

In June, the company announced it would build and operate a US$2.1 billion natural gas pipeline in Mexico. The company said it would parent with Sempra Energy’s IEnova unit, with TransCanada owning a 60 percent stake in the venture. The effort will be backed by Mexico’s state-owned power company and is expected to be in service by 2018. TransCanada recently made news in the United States when it announced a lawsuit against the state because of the suspension of the controversial Keystone XL pipeline project.

Lastly, Benefits Canada recently reports, Ontario Teachers’, PSP increase stakes in sustainable investment firm:

The Ontario Teachers’ Pension Plan and the Public Section Pension Investment Board will buy out Banco Santander’s interest in Cubico Sustainable Investments. The three firms launched the London-based renewable energy and water infrastructure company in May 2015.

After the acquisition, PSP Investments and Ontario Teachers’ will each own 50 per cent of Cubico’s shares.

Cubico’s initial portfolio included 18 water, wind and solar infrastructure assets with a net capacity of 1.2 gigawatts. The company has since acquired four new assets, bringing its net capacity to 1.62 gigawatts. Cubico’s 22 assets are in Brazil, Italy, Ireland, Mexico, Portugal, Spain, United Kingdom and Uruguay.

“Our increased participation in Cubico is aligned with PSP Investments’ long-term investment approach and strategy to leverage industry-specific platforms and develop strong partnerships with liked-minded investors and skilled operators,” Guthrie Stewart, senior vice-president and global head of private investments at PSP Investments, said in a release.

“Cubico’s flexible investment and acquisition approach fits well with Ontario Teachers’ approach to private investments,” Andrew Claerhout, senior vice-president of infrastructure at Ontario Teachers’ said in the release.

As you can see, Canada’s large public pensions have been busy hunting for traditional and alternative energy deals all around the world. They’re using their internal expertise and their expert network of partners to capitalize on opportunities as they arise, and that is why they are way ahead of their global counterparts when it comes to opportunistic, long-term investing.