Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Tito Boeri, Pietro Garibaldi, Espen Moen wrote a comment for Vox EU, CEPR’s policy portal, Increases in the retirement age and labour demand for youth (h/t, Suzanne Bishopric):

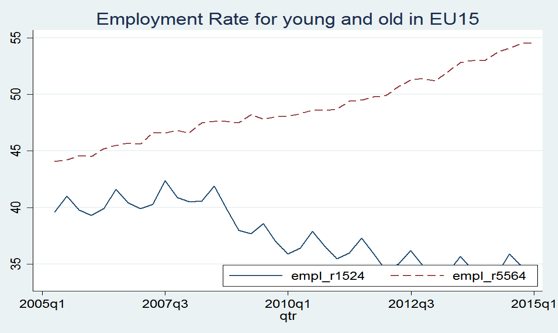

Most European countries have experienced a dramatic increase in youth unemployment since the beginning of the Great Recession in April 2008. For the Eurozone as a whole, employment for people aged between 15 and 24 fell by almost 17% in six years. In southern Europe, the smallest decline was 34% in Italy, and the largest was 57% in Spain. Other age groups suffered less: 3% for the Eurozone as a whole and, for all older age groups in all countries, between one-third and one-sixth of the employment decline for young workers.

In the Eurozone as a whole, employment for people in the 55-65 age group increased by approximately 10%. Demographic factors do not account for these changes. Both employment levels and employment rates moved in opposite directions for young and senior workers (Figure 1).

The strong increase of youth unemployment was predicted by the research on contractual dualism (Saint-Paul 1993, Boeri 2011). This predicts that youth unemployment will respond more strongly to cyclical fluctuations in countries with strict employment protection in permanent contracts and ‘fire-at-will’ for temporary contract workers (Boeri et al 2015). Boeri and Garibaldi (2007) predicted that immediate declines in youth unemployment after two-tier labour market reforms, even under slow growth scenarios, would be followed by youth disemployment when macroeconomic conditions deteriorate. Research on contractual dualism, however, does not explain why employment rates have diverged for young and old.

Figure 1. Employment rate for young and old workers in the EU15

Portugal in 2007, Spain in 2011, Greece in various stages between 2010 and 2016, and Italy in 2011 all increased the retirement age during the recession. So is the decline in youth employment related to changes in the retirement rules? Research on retirement is typically focused on the supply side. As a result, it ignores trade-offs between young and old workers on the demand side. Vestad (2013) used administrative data to estimate the impact of an early retirement programme on youth employment in Norway, but there is little other research on this topic.

The economics of pension reform and labour demand

The economics of a pension reform and labour demand is more subtle than a simple exogenous shift in labour supply. Most of the individuals involved are already employed and cannot be easily fired. Under a pension reform forcing firms to retain older workers, there are two effects at work.

- First, there is a negative scale effect, due to decreasing returns to scale. The reform forces some of the older workers to stay employed rather than retire. This tends to increase output, but with decreasing marginal returns to scale in production, the marginal product of young workers falls and so does youth hiring.

- Second, there is an effect that depends on the degree of complementarity between young and old workers: the stronger the complementarity, the more likely that the reform could positively affect youth employment.

Which one of the two effects – the scale or the substitution effect – prevails is ultimately an empirical matter.

Italy and the Monti Fornero reform

Italy provides an excellent case study of whether unexpected increases in retirement age can have adverse effects on youth employment. In the middle of a recession, labour markets are typically driven by the demand side. In Italy, employment rates for the 15-24 and 55-64 age groups were almost the same in 2005 (Figure 2). Ten years afterwards, the employment rate for the 55-64 age group was 45%, while the youth employment rate was approximately 12%. In this period, the normal retirement age increased, and the minimum contribution requirement for access to early retirement tightened. In December 2011, the Monti Fornero reform increased the retirement age by up to five years for some categories of workers. We use this policy experiment to estimate the impact of increases in retirement age on youth labour demand.

Figure 2. Employment rate for young and old workers in Italy

We had access to a dataset on Italian firms before and after the reform compiled by the Italian social security administration (INPS). We looked at whether a sudden and unexpected increase in the contributory and age requirements for retirement, which forced firms to keep workers previously entitled to pensions to stay in the payroll, affected labour demand for young workers. We identified the population hit by the changes in retirement rules in each firm, and looked at the dynamics of net hiring in the same firms.

The results are clear. Before and after the reform, firms that were more exposed to the mandatory increase in the retirement age significantly reduced youth hiring compared to those who were less exposed to the reforms. We cannot rule out that the latter firms may have increased their hiring as a result of the reform, due to general equilibrium effects. Nevertheless, we argue that the reform was likely to reduce the labour market prospects of young workers.

We estimate that five workers locked in for one year mean the firm hires approximately one less young person. Firms with more than 15 employees lost 160,000 youth jobs in this period. Of these, 36,000 can be attributed to the reform. We performed robustness checks including rolling regressions across the size distribution, propensity score matching, and a falsification test on the pre-reform years.

Policy implications

Cautiously, we make two points.

Reducing the generosity of pensions in the middle of the European sovereign debt crisis was probably inevitable, despite the severe recession that southern European economies experienced. But this tightening could have been done by reducing pensions for workers who were retiring before the normal retirement age. This would have allowed firms to encourage the least productive older workers to retire. With hindsight (as well as the evidence above), much more should have been done by European policymakers to help and sustain young workers who were about to enter the labour market. The equilibrium for young and old workers in the southern European labour market was not what these policies set out to achieve. We risk a lost generation in Europe.

Also, the retirement age should be as flexible as possible. As far as Italy is concerned, the long-run defined contribution system is viable and sustainable. A system like this, though, has a prolonged transition phase. During the medium-run adjustment to the new system, policy should seriously attempt to increase actuarially neutral flexibility in retirement. From the perspective of broader fiscal coordination, our results suggest that short-sighted fiscal rules that force sudden increases in retirement age during major downturns may backfire. They may cause a prolonged and almost total freeze on new hires, particularly when older workers are locked in by the increase in the retirement age.

Fiscal rules should better focus on fiscal sustainability in the long run. A 2005 reform of the Stability and Growth Pact attempted this, but in words, not in practice. It stated that a short-run deterioration in the budget deficit could be tolerated if, at the same time, a government reduces its long-run liabilities. In practice, however, this principle can only be enforced by explicitly including in the pact any efforts that reduce the hidden liabilities associated with social security entitlements, the most important long-run liabilities in our ageing societies.

This means that a citizen could be given some freedom to retire when he or she wants, provided the size of the pension reflects age and life expectancy. More pensions could be paid under downturns without affecting long-term liabilities, because the additional pensions for early retirees would be lower than those paid to people who retiring later. Therefore this system could be budget-neutral and operate as an automatic stabiliser. A pact that allows for sustainable flexibility in retirement would also help countries facing the huge demographic shock that is associated with the current refugee crisis.

References

Boeri, T. (2011) “Institutional reform and dualism”, Handbook of Labor Economics 4b ed. D. Card and O. Ashenfelter. Elsevier.

Boeri, T. and Garibaldi P. (2007) “Two Tier Reforms of Employment Protection: a Honeymoon Effect?” The Economic Journal 117 (521), F357-F385

Boeri, T., Garibaldi, P. and E. R. Moen (2015) “Graded security from theory to practice”, VoxEU.org, 12 June.

Boeri, T. Garibaldi, P. and E. R. Moen (2016) “A Clash of Generations? “Increase in Retirement Age and Labor Demand for Youth”, CEPR Discussion Paper 11422 and WorkInps Paper 1.

Saint Paul, G. (1993) “On the Political Economy of Labor Market Flexibility”, NBER Macroeconomic Annual 151-192

Vestad, O. L. (2013) “Early Retirement and Youth Employment in Norway”, Statistic Norway.

The theme this week is the global pension crunch which is why I covered developments in China, Chile, Brazil and now looking more closely at the Eurozone’s pension woes.

Today’s comment happens to coincide with the ECB’s monetary policy decision (more on that below) and this was done purposely to demonstrate why Mario Draghi’s worst nightmare is far from over.

Regular readers of my blog will recall that I called checkmate for Europe’s pensions back in March and basically haven’t changed my mind on the dismal prospects and huge challenges Eurozone’s pensions have to contend with.

As far as the findings of the academics above, I’m hardly impressed. They are basically arguing that increasing the retirement age in Greece, Italy, Portugal and Spain after the Great Recession exacerbated youth unemployment in southern Europe and we risk seeing a lost generation in Europe because of these retirement reforms.

Being good academics, the authors claim they “performed robustness checks including rolling regressions across the size distribution, propensity score matching, and a falsification test on the pre-reform years.”

It all sounds so legitimate and “robust”. Unfortunately, it’s mostly academic nonsense and the primary reason why I stopped reading a lot of academic literature on economics.

Do you want to know the real reason why youth unemployment is soaring in Greece and southern Europe? It’s not because they followed the rest of the developed world and increased the retirement age. It’s because of archaic labor laws that basically protect powerful interest groups and virtually make it impossible to introduce real labor market competition in these countries.

I am going to talk about Greece because I know what that country extremely well. Very bright Greeks, mostly Greeks living outside Greece (and some living there), know exactly what Greece needs in terms of meaningful reforms.

Much has been made lately about how the IMF screwed up with Greece — and to be sure, it did — but little attention is being placed on how successive Greek governments refuse to implement much needed reforms to finally break the bloated public sector which is crippling their economy.

Let me be clear, I have nothing against a well managed and strong public sector but any country that experiences a sovereign debt crisis and keeps expanding its public sector is doomed to fail.

And let me take it a step further and state this: any country that relies on the primacy of its public sector is doomed to fail. I don’t care if it’s Greece, Italy, Spain, Portugal, France or even Canada, a thriving public sector at the expense of a dwindling private sector is a recipe for disaster.

I mention this because in Greece, it’s business as usual as Prime Minister Alexis Tsipras recently announced plans to overhaul the Constitution in order to hire 20,000 civil servants.

You read that right, bankrupt Greece wants to increase its bloated public sector after it went through a major sovereign debt restructuring.

Not surprisingly, Greece is facing another bailout standoff with its creditors amid reports that Eurozone countries will refuse to release additional funds to it this month.

None of this surprises those of us who know Greek politicians all too well. They are crooked, crony liars who will do anything, and I mean anything, to stay in power which is why even in the face of disaster, they succumb to the demands of powerful public sector unions.

The biggest tragedy inflicted upon Greece over the last forty years was this insane expansion of its public sector to epic proportions. It all started with Andreas Papandreou but each successive Greek government since then caught on to the game of handing out goodies to public sector unions to ensure their hold on power.

That’s why I can’t take any Greek politician seriously, whether it’s Yanis Varoufakis peddling his memoirs on Europe’s crisis or even George Papaconstantinou, another former finance minister who rightly notes in his memoirs that it’s game over for Greece.

[Note: My biggest beef with Varoufakis is not that he’s a shameless self-promoter looking to sell his books. In fact, I highly recommend you read his best book, The Global Minotaur. My biggest beef with him is that he’s a master of half truths and was never able to admit that Greece’s bloated public sector was crippling its economy and continues to do so till this day.]

What does all this have to do with Europe’s lost generation and the Eurozone’s pension policy? Europe is a huge structural mess and no matter what the ECB does, it’s losing its battle against deflation.

And while Nobel laureates like Joe Stiglitz discuss the real issues in the Eurozone and how to solve them, I personally believe this fragile union is living on borrowed time and the real issue is how to stop European and Asian deflation from ravaging the global economy.

This is why I can’t take clowns warning of a bond bubble seriously. What world do they live in? Do they not realize how Brexit was Europe’s Minsky moment and the increasingly likely disintegration of the Eurozone will drive US Treasury yields to uncharted territory?

I don’t know, maybe there’s something I’m missing, but from a macro perspective I’m more worried than ever that the global deflation tsunami is gaining steam and unless there is a massive and coordinated fiscal response (by implementing major infrastructure projects all over the world), it’s going to wreak havoc on the global economy for decades (I think it’s already too late).

And when that happens, we’re not going to be talking about Europe’s lost generation, we’re going to be fretting over the entire world’s lost generation.

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712