Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Lucinda Shen of Fortune reports, Eton Park Closing Shows How Hedge Funds Are Dying at an Alarming Rate:

While doors are opening all over the White House for Goldman Sachs alumni, another one is being closed by one of its former shooting stars.

Eton Park Capital Management, helmed by Eric Mindich, is shutting down and returning its capital to investors, the hedge fund told its clients in a letter Thursday. It’s a disappointing end for the hedge fund, which opened in 2004, riding on Mindich’s financial pedigree and reputation as a wunderkind. At the time, Eton Park was said to be the biggest-ever hedge fund launch, with $3.5 billion in capital commitments, according to the New York Sun.

But now, its holdings, which once ballooned to $14 billion, have withered down to $7 billion, after the hedge fund made several bad stock bets, accelerating the exodus of investors who have lost faith not only in Eton Park, but also in the industry.

“Recently, a combination of industry headwinds, a difficult market environment and, importantly, our own disappointing 2016 results have challenged our ability to continue to maintain the scale and scope we believe necessary to pursue our investment program consistent with our founding principles,” Mindich wrote in a letter to investors.

Mindich is not alone. The challenges he has faced are well known to the 9,893 hedge funds left in the $3 trillion industry.

Not only were markets choppy in the early months of 2016, but increasingly, investors have begun questioning whether the high fees charged by hedge funds are justified. Research, along with an experiment by legendary investor Warren Buffett, have shown that low-cost stock market index funds have generally outperformed hedge funds.

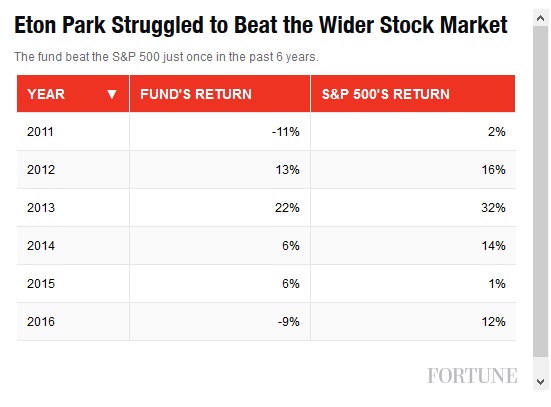

Eton Park lost 9% in 2016. Not only did Mindich’s returns lag behind the S&P 500—they also underperformed the overall hedge fund industry’s 5.5% return last year, according to Hedge Fund Research. Eton Park’s underperformance also wasn’t contained to just 2016. It beat the S&P 500 just once in the last six years, and has been relatively flat in 2017 (click on image).

It’s the largest hedge fund fund closure of 2017, and points to more troubling trends for the industry now struggling to keep its customers.

In a bid to keep their clients happy, funds such as Och-Ziff Capital have hacked away at their fees, while others including Paul Tudor Jones have dealt with investor redemptions by cutting staff in recent years.

But those methods don’t seem to have stymied the outflow of clients from the industry. Roughly $70.1 billion in assets were redeemed last year—the highest level since 2009.

Perhaps more alarmingly, 2016 continued on a six-year trend of fewer and fewer new hedge funds opening—and a three-year trend of more and more hedge fund closures. That’s resulted in a decline in the overall number of hedge funds from their peak in 2015, with 147 fewer hedge funds in operation by the end of 2016.

In fact, 2016 had the highest level of hedge fund closures and lowest level of openings since 2008, the year of the financial crisis. And for the second year in a row, the rate of hedge fund closures outpaced that of hedge fund openings, with 1,057 hedge funds closing in 2016,while 729 hedge funds were launched, according to HFR.

So will hedge funds have another rough year in 2017? It’s possible that select funds will do well, though the industry as a whole has underperformed the market every year since 2008. The rising frustration among investors over high fund fees and inconsistent returns? That’s not likely to go away any time soon.

You can read more about Eton Park shutting down in Reuters, the New York Times and the Wall Street Journal. You can also read about the fund’s terrible 2016 performance in Institutional Investor.

You might be thinking “so what, who cares?”, it’s just another hedge fund charging huge fees delivering sub-beta performance. And you’re right, except in this case, Eton Park isn’t just any hedge fund, it’s a $7 billion well-known multi-strategy hedge fund, one of the elite hedge funds that has succumbed to an increasingly brutal market environment.

And investors are taking note. As I explained in a recent comment on No Luck in Alpha Land, fed up of paying excessive fees for mediocre returns, investors continue to squeeze hedge funds on fees or they are just abandoning them altogether.

Now, you might think it’s noble of Eric Mindich to return capital to his investors realizing his fund can’t deliver the goods in terms of performance but I assure his decision is based on selfish business reasons, not altruism toward his investors.

One former hedge fund allocator put it this way:

“All these greedy guys converting to family offices so they don’t have to make their investors money back… the same money that paid them all those fees they became wealthy off of. It’s really sad. The only other reason is avoiding prosecution because regulators getting too close.”

Got it? The number one reason a multibillion dollar hedge fund closes shop and returns money to its investors after suffering poor returns is to avoid having to make up the money it lost. The managers know their fund is so much underwater that it’s extremely hard to make back the losses to surpass their high-water mark and start charging performance fees again. Without performance fees, they risk losing their top traders and it just isn’t worth keeping the fund open.

For elite managers, they simply close shop, get to manage their own billions as a family office and if things go well, they can come back in a few years and open up a new fund under a new name, and start charging 2 & 20 all over again.

It’s a great gig, one that most struggling hedge funds and fund managers don’t get to enjoy, but when you reach superstar status, you can pull it off.

Think about it. You’re an elite hedge fund manager charging 2 & 20 on billions under management. If you don’t perform well, you’re still collecting a 2% management fee on billions of assets under management in good and bad years and if things go downhill, you just close up shop, convert to a family office, manage your billions and aim to open up a new fund down the road under a new name.

It’s enough to drive investors crazy but most investors are stupid and they have short memories. They just look at pedigree and don’t ask the tough questions that need to be asked.

Trying to capitalize on investors’ frustrations, some hedge funds are taking a win-or-die approach to their fee model to lure money into their fund but I predict they will die before attaining their bogey.

Honestly, I am watching all the nonsense going in the hedge fund industry and also watching various markets closely and I’m hardly surprised that big and small hedge funds are closing shop.

No matter what you’re trading, it’s a very hard environment, and this is especially true if you’re a huge hedge fund that needs scale to move the needle.

I just finished writing a comment on why I wouldn’t read too much into the greenback’s recent slide and remain long US dollars. After talking to a buddy of mine who trades currencies and manages his own hedge fund, I updated that comment to give my readers some more insights into understanding why I remain long US dollars.

But my buddy was telling me that it’s increasingly harder to make money trading currencies because “ranges are tight and the algos are front-running your every move.” He added: “If humans were doing what algos are doing, they’d be prosecuted, but because algos and high-frequency currency platforms supposedly add to liquidity and price discovery, nobody raises a peep.”

He was even more blunt: “The only hedge funds making money in currencies in this market are those that have insider information. You see leaks going on all the time and some big funds making big bets prior to a major announcement and wonder what did they know that I don’t know?”

Good point, sometimes you see major moves in currencies just prior to a major announcement and wonder who knew what and when. The F/X market is still the Wild West but regulators don’t touch it because it’s the number one profit center for big banks which rake retail and corporate clients on fees for each currency transaction (up to 3% for retail clients and up to 20 pips for corporate clients, and all those fees add up and go straight to banks’ profits).

Anyway, whether you are a currency hedge fund, a multi-strategy hedge fund, or a Long-Short hedge fund, these are difficult times and a few well-known funds are reeling (only hedge fund quants seem to be escaping the carnage and doing relatively well, for now).

For example, Reuters reports that hedge fund Pine River Capital Management LP is losing two more partners following a difficult year that involved a restructuring and major decline in assets.

Again, these aren’t your run-of-the-mill crappy hedge funds, these are well known “elite” hedge funds managing billions which are struggling and closing up shop.

And we’re not even experiencing a financial crisis yet. Wait till that hits the industry and many more top players close up shop. It’s a disaster and it will have knock-on effects in terms of employment on Wall Street and the Manhattan, Connecticut and London real estate markets.

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712