All around the country, employers are funneling new hires into 401(k)-type retirement plans instead of traditional pension schemes.

But the members of one Illinois fund are given the choice of participating in a defined-benefit or defined-contribution plan–and more than ever, they’re choosing 401(k)s. From Illinois Policy:

Today, more than 13 percent of all active employees in the State Universities Retirement System, or SURS, participate in a 401(k)-style plan instead of a traditional pension plan run by the state. These state-university workers control their own retirement accounts and aren’t part of Illinois’ increasingly insolvent pension system.

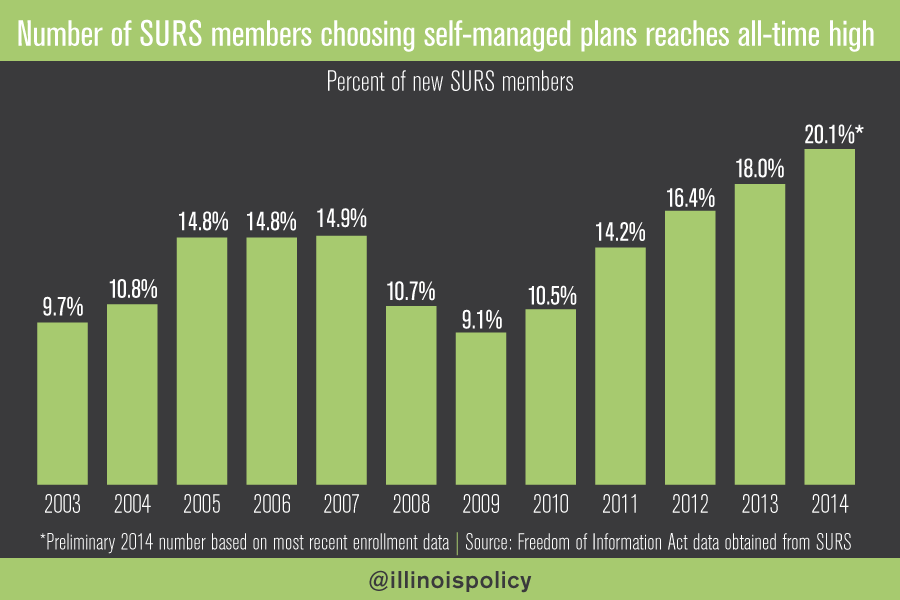

And recent data from SURS obtained through a Freedom of Information Act request shows the popularity of 401(k)-style plans is growing.

Nearly 20 percent of all SURS employees eligible for a retirement plan in 2014 have chosen a self-managed plan over the traditional pension scheme. Just a few years after the Great Recession, the number of SURS members choosing self-managed plans has reached an all-time high.

In 1998, SURS began allowing its new workers to opt into self-managed retirement plans. In these plans, an employee contributes 8 percent of his or her salary toward retirement savings and the employer puts in a matching 7 percent. That means the employee has the equivalent of 15 percent of each paycheck put into an account that’s entirely theirs.

As for why employees are opting into 401(k)s over traditional pensions? The growing concern over the health of Illinois’ pension funds probably plays a big role. Strong stock market gains over the last few years likely play a part, as well.

What you fail to mention is that this choice must be made immediately after being hired, and those starting employment under SURS in 2011 or later had to choose between an unchanged defined contribution plan (where the state does indeed contribute 7% of salary – in total, because it does not pay into Social Security) or a greatly diminished “Tier 2″ defined benefit plan that costs the state considerably less than 7% of payroll to provide. The only surprise is that 100% of new employees since 2011 are not choosing the defined contribution plan, as it is by far the better deal. Also, contrast the paltry options available to new hires under SURS with what the much-maligned firm Walmart provides to its employees: a full 6.2% employer contribution to Social Security plus a 6% matching contribution if the employee also contributes 6% to his/her 401k. By any reasonable measure Walmart’s retirement benefits are far better than those available to new hires under SURS.

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712