Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Back in July, Chris Flood and Chris Newlands of the Financial Times reported on CalSTRS’s private equity woes:

The second-largest US public pension fund has admitted it has failed to record total payments made to its private equity managers over a period of 27 years.

The admission by Calstrs, the $191bn California-based pension fund, prompted John Chiang, the state treasurer of California, to declare he will investigate the failure, which poses serious questions as to how pension fund money is being spent.

The news comes a week after FTfm reported that the state treasurer had voiced “great concern” that fellow pension fund Calpers, the US’s largest at $300bn, also has no idea how much it pays its private equity managers.

Mr Chiang said he would demand clear answers from Calpers over why it does not know how much has been paid in “carried interest” or investment profits over a period of 25 years to the private equity managers running its assets.

A spokesman for Calstrs, which helps finance the retirement plans of teachers, said the fund does not record carried interest. “What matters is the overall performance of the portfolio.”

Following questions from FTfm, Mr Chiang said he would demand Calstrs look into payments of carried interest to its private equity managers.

“Disclosure [of carried interest fees] is very important,” said Mr Chiang, who sits on the administration board of both Calstrs and Calpers.

The revelations come just weeks after US regulators issued an explicit warning to the private equity industry to expect more fines for overcharging investors.

Calpers, which uses more than 100 private equity firms, identified a need to track fees and carried interest better in 2011, but it has taken until now to develop a new reporting system for its $30.5bn private equity portfolio.

But Calstrs, which manages a $19.3bn private equity portfolio and has 880,000 members, said it has no plans to upgrade its systems for tracking and reporting payments to private equity managers.

Margot Wirth, director of private equity at Calstrs, said it used “rigorous checks” to ensure private equity managers took the right amount of carried interest.

All of Calstrs’ partnerships with private equity managers were independently audited, Ms Wirth added. She said the pension fund carried out its own internal audits and employed a specialist “deep dive” team to look at private equity contracts.

Professor Ludovic Phalippou, a finance professor at the University of Oxford Saïd Business School, who specialises in private equity, told FTfm last week: “Calpers’ total bill is likely to be astronomical. People will choke when they see the true number.”

Prof Phalippou said the same would be true of Calstrs, which first invested in private equity in 1998.

Ms Wirth argued it was “wrong to conflate the fees paid to private equity managers with carried interest”.

She said: “Carried interest is a profit split between the investor and the private equity manager. The higher that carried interest is, then the better both the investor and private equity manager have performed.”

The fear is that if sophisticated investors such as Calpers and Calstrs faced difficulties in obtaining accurate information, then it could only be harder for smaller pension funds, endowments and wealth managers that are less well resourced.

David Neal, managing director of the Future Fund, Australia’s A$128bn sovereign wealth fund and one of the world’s largest investors in private equity, said: “There just are not enough decent private equity managers around to justify the fees.”

He added: “We negotiate fee arrangements that transparently reward genuine performance and drive alignment of interest. Where managers cannot meet those expectations, we do not invest. While we work hard at the arrangements with our managers, the industry still has some way to go.”

Fast forward to October where Yves Smith of Naked Capitalism just put out another stinging comment, CalSTRS Board Chairman Harry Keiley, in Op-Ed Rejected by Financial Times, Gave Inconsistent and Inaccurate Information in Carry Fee Scandal (added emphasis is mine):

The staff and board members of California public pension fund CalSTRS continue to embarrass themselves in their efforts to justify their indefensible position on private equity carry fees.

Readers may recall that the biggest public pension fund, CalPERS, had a put-foot-in-mouth-and-chew incident when it said it didn’t track the profits interest more commonly called “carry fees,” which is one of the biggest charges it incurs on its private equity investments. CalPERS added to the damage by falsely claiming that no investors could get that information. After we broke that story and a host of experts and media outlets criticized CalPERS over the lapse and the misrepresentation, CalPERS reversed itself. It asked its general partners for all the carry fee data for the entire history of all of its funds, and obtained it all in a mere two weeks, with only one exception out of the nearly 900 funds in which it has invested.

So what has the second biggest public pension fund, CalSTRS, done? Like CalPERS, it has admitted that it does not track carry fees. But in a remarkable contrast, CalSTRS is attempting to justify inaction by misleading beneficiaries as to how much information it really has and saying that it’s thinking really hard about what (if anything) to do.

The dishonesty of the CalSTRS position is evident in its e-mails with the Financial Times after the pink paper reported that CalSTRS, like CalPERS, did not track carry fees, and California Treasurer John Chiang, who sits on both the CalPERS and CalSTRS boards, said he would press CalSTRS to look into the matter. I became aware of the contretemps when an FT reporter called me to thank me for my work. I asked him how CalSTRS was taking his story. He said they weren’t happy with it and they’d offered CalSTRS the opportunity to publish an op-ed, which was running early the following week. When I failed to see any such article, I contacted the reporter, who said his editor had rejected the article. I then lodged a Public Records Act request (California-speak for FOIA) for the op-ed and all e-mails between CalSTRS and the Financial Times from the date the Financial Times ran the article on CalSTRS’ carry fee tracking.

It’s important to remember that CalSTRS had said, flatly, that it does not know what it pays in carry fees. From the Sacramento Bee on July 2:

Ricardo Duran, a spokesman for the California State Teachers’ Retirement System, said CalSTRS can estimate the fees “within a couple of percentage points” but doesn’t report the figure.

“It’s not a number that we track,” Duran said. “It’s not that important to us as a measure of performance.”

Memo to CalSTRS: if you are estimating, you don’t know for sure.*

After the Financial Times ran its CalSTRS story, Ricardo Duran, CalSTRS’ head of communications, sent a clearly-annoyed e-mail to the Financial Times’ Chris Flood. Duran tried objecting that the so-called carry fee was not a fee because….drumroll..it was not paid directly by CalSTRS to general partners:

The following paragraph talks about [California Treasurer and CalSTRS board member] Mr. Chiang’s demand of CalPERS about how much has been “paid in carried interest.” Carried interest is not a payment but a profit split. I believe [head of private equity] Margot [Wirth] mentioned that distinction as well.

The language throughout the piece conflated carried interest with management/manager fees. That’s fine if that’s the way you want to characterize it. I only ask if you write about CalSTRS and carried interest again, you specifically mention this and attribute it to me or Margot.

So get a load of this: CalSTRS demanding that if the FT ever dare report on CalSTRS’ carry fee reporting again, that it include the staff’s pet position that a carry fee is not a fee, even when that contradicts statements by board members who oversee CalSTRS. Since when do mere employees a California agency have the right to undercut on-the-record statements of top California government officials?

And that’s before you get to the fact that this “carry fee is not a fee” position is bogus. As Eileen Appelbaum, the co-author of Private Equity at Work, wrote:

The email exchange in which CalSTERS argues with the Financial Times over the question of when is a fee not a fee has a certain Alice in Wonderland quality. The CalSTRS representative insists that a fee is not a fee if it takes the form of profit sharing. But profit sharing is clearly a performance fee – a fee paid to the PE investment manager based on the performance of the PE fund.

And as an expert who has been writing about private equity fees for decades said:

Private equity general partners put up around 1% of the money in a fund once you back out management fee waivers. They get 20% of the profits. The part over and above their pro-rata share is clearly a fee. As we lawyers like to say, res ipsa loquitur.

But the best part is Duran’s wounded claim that the FT “conflated” interest with management fees, as if that were inaccurate. This is from the very first limited partnership agreement I looked at from our document trove, KKR’s 2006 fund:

The Partnership will not invest in investment funds sponsored by, and as to which a management fee or carried interest is payable to, any Person….

Gee, KKR says in its own agreement that carried interest is indeed “paid” just like management fees!

But this is all a warm-up to the op-ed that the chairman of CalSTRS’ board, Harry Keiley, submitted to the Financial Times.

[snip]

Go to Naked Capitalism to read the rest of the story, including the rejected op-ed.

Wow, where do I begin? First, let me praise Yves Smith (aka Susan Webber) for lodging a Public Records Act request (California-speak for FOIA) for the op-ed and all e-mails between CalSTRS and the Financial Times and bringing this to our attention.

Second, in sharp contrast to other tirades, I completely agree with Yves Smith, these emails and that editorial are a total embarrassment to CalSTRS and either show gross incompetence on the part of CalSTRS’s private equity staff (Keiley didn’t write that without their input) or more likely, a pathetic attempt to misinform the public on how much has been doled out in management fees and carried interest (“carry” or performance) fees throughout all these years.

Third, and most importantly, I do not buy for one second that the private equity staff at CalPERS or CalSTRS do not track all fees doled out to each GP (general partner or fund) to the penny. If they don’t, they all need to be immediately dismissed for gross incompetence and breach of their fiduciary duties and their respective boards need be replaced for being equally incompetent in their supervision of staff (except keep JJ Jelincic on CalPERS’s board as he’s the only one doing his job, grilling CalPERS’s private equity team and asking tough questions that need to be answered).

I’m not going to mince my words, it’s simply indefensible for any large public pension fund investing billions in private equity, real estate and hedge funds not to track all the fees paid out to the GPs as well as track any hidden rebates with third parties which these GPs hide from their clients, effectively stealing from them.

You might be wondering, how hard is it for a CalPERS or a CalSTRS to track fees and other pertinent information from their private equity fund investments? The answer is it’s not hard at all. Over the weekend, I was looking at buying a few more books in finance (not that I need to add to my insanely large collection) and was looking at one called Inside Private Equity.

I was attracted to the book because one of the authors is Austin Long of Alignment Capital who I met back in 2004 when I was helping Derek Murphy set up private equity as an asset class at PSP Investments. I liked Austin and their approach to rigorous due diligence before investing in a private equity fund (like on-site visits where they pull records off a deal thy pick at random to analyze it and pick a junior staff member at random to ask them soft and hard questions on the fund’s culture).

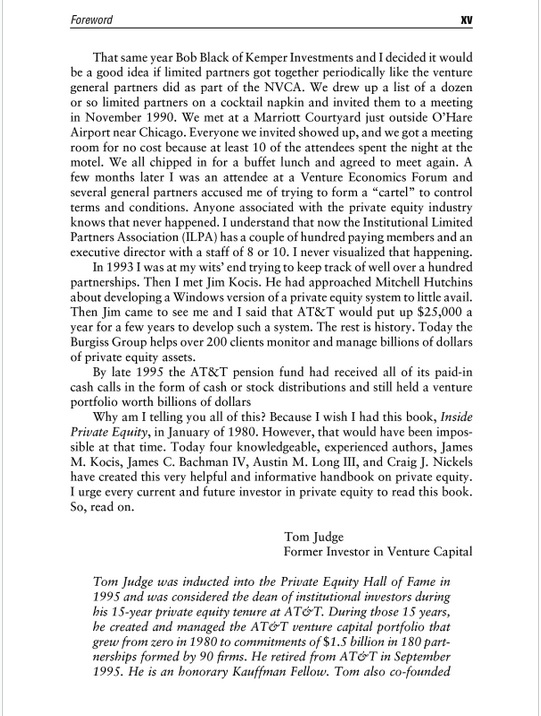

Anyways, I was reading the foreword of the book which was written by Tom Judge, a former VC investor and inductee to the Private Equity Hall of Fame (1995), and he was writing about how it used to be complicated tracking over 100 partnerships for the AT&T pension fund until he met Jim Kocis, another author of the book, and founder of the Burgiss Group which provides software-based solutions for investors in private equity and other alternative assets (click on image to read passage):

Today the tools Burgiss Group developed support over a thousand clients representing over $2 trillion of committed capital.

Why am I writing this? I’m not plugging Burgiss Group because I simply don’t know them well enough and haven’t performed a due diligence on them but obviously it’s a huge firm with excellent experience in tracking detailed information of PE partnerships on behalf of their clients, providing them with the transparency they need to track their fund investments.

Again, in 2015, it’s simply mind-boggling and inexcusable for a CalPERS or a CalSTRS not to be able to track detailed information on all their fund investments going back decades. This includes detailed information on management fees and carry.

What are CalPERS and CalSTRS hiding? I don’t know but I think John Chiang, the state treasurer of California, is absolutely right to investigate and inform Califonia’s taxpayers on exactly how much has been doled out in private equity, real estate and hedge fund fees over the years at these two giant funds which pride themselves on transparency.

Below, I embedded the three investment committee clips from CalSTRS’s September board meeting. In the first clip, Chris Ailman, CalSTRS’s CIO, discusses their risk mitigation strategies and Mike Moy of Pension consulting Alliance, discusses the performance of private equity in the third clip.

I know they’re excruciatingly long (you can fast-forward boring sections) but take the time to listen to these investment committees as they provide a lot of excellent insights. Not surprisingly, nothing was mentioned on how exactly CalSTRS is going to track and disclose all fees paid to their private equity partnerships (however, in the third clip, Mr. Murphy, a teacher representing the California Federation of Teachers did mention this issue was a huge concern).

If the staff at CalSTRS, CalPERS or anyone else has anything to add, feel free to reach out to me at LKolivakis@gmail.com. I have my views but I don’t have a monopoly of wisdom when it comes to pensions and investments and I welcome constructive criticism on all my comments and will openly share your input, good or bad.

Photo by Stephen Curtin via Flickr CC License