A few names consistently pop up in any discussion of states with the most pension debt—Illinois, New Jersey and a handful of other states are frequently cited as shouldering the heaviest pension burdens.

Hawaii isn’t always on that list. But according to one watchdog group, Truth in Accounting, the state’s pension burden is among the worst in the country. The Hawaii Reporter recaps:

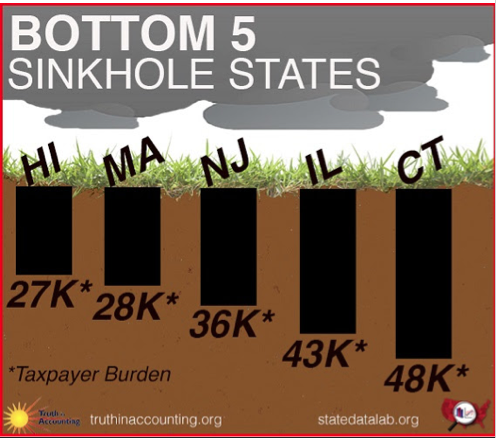

Only Massachusetts, New Jersey, Illinois and Connecticut are in worse fiscal condition that Hawaii.

Donna Rook, president of StateDataLab.org, a division of Truth in Accounting, said Hawaii has been one of the five worst states since this annual study was started in 2009.

“The average Hawaii taxpayer’s share of the state’s debt is $27,000 after available assets are tapped. Since we set aside both capital assets and debt related to capital, the remaining debt is primarily unfunded pensions and retirement health,” Rook said.

The $27,000 per taxpayer is about 57 percent of the average resident’s annual income, Rook said.

Sheila Weinberg, founder and CEO of Truth in Accounting, said Hawaii financial statements show $4 billion in retirement liabilities, but the state actually has nearly $15 billion of unfunded retirement promises.

Hawaii has only $5 billion to pay the state’s bills, which total $18 billion, Weinberg said.

The same Truth in Accounting report also shared some better news: Hawaii has vastly improved the timeliness of its year-end financial reports.

For more data on Hawaii, visit Truth in Accounting’s data lab here.