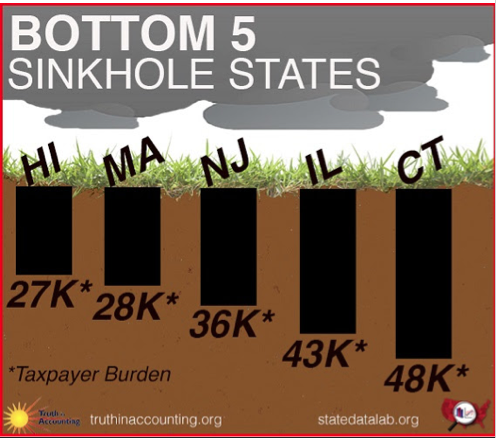

Every year, watchdog group Truth in Accounting scrutinizes the finances of every states and produces a report on what they find.

By and large, Nebraska passed TiA’s fiscal test with flying colors—except when it came to retirement liabilities. The state reported its liabilities to be a little over $1 million. But Truth in Accounting says the liabilities are closer to $770 million.

From Nebraska Watchdog:

Truth in Accounting, an economic think tank based in Chicago, named Nebraska one of just a handful of “sunshine states” with more than enough money to pay its bills. The state has $4.3 billion in liquid assets and owes about $3 billion, for a surplus of $1.3 billion — or $2,200 per taxpayer.

However, Truth in Accounting says Nebraska’s retirement liabilities are “massively underreported” at $1.1 million. Its detailed analysis of the state’s assets and liabilities, including unreported pension and retirement health liabilities, found $772.5 million in retirement benefits promised but not funded.

“Because of the confusing way the state does its accounting, only $1.1 million of these liabilities are reported on Nebraska’s balance sheet,” TIA wrote.

The report says unfunded employee retirement benefits represent 26 percent of state bills, as state employees have been promised $772.5 million in pension benefits. The good news is Nebraska has the money to pay for the liabilities.

Read the detailed report on Nebraska’s fiscal situation here.

Photo by Tom Benson via Flickr CC