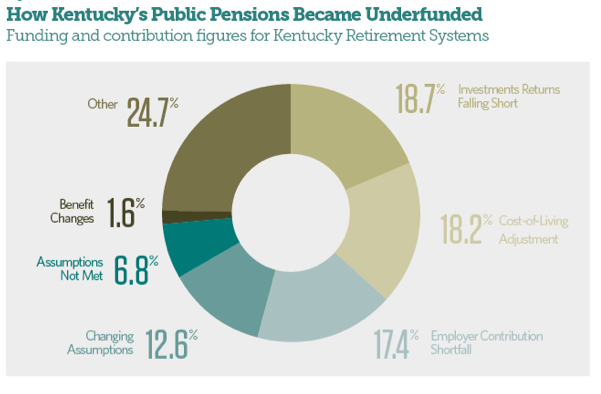

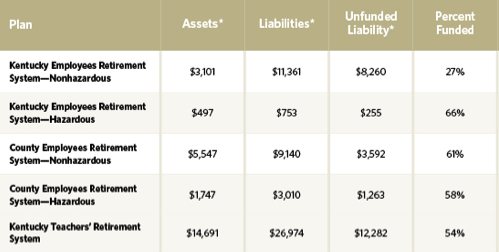

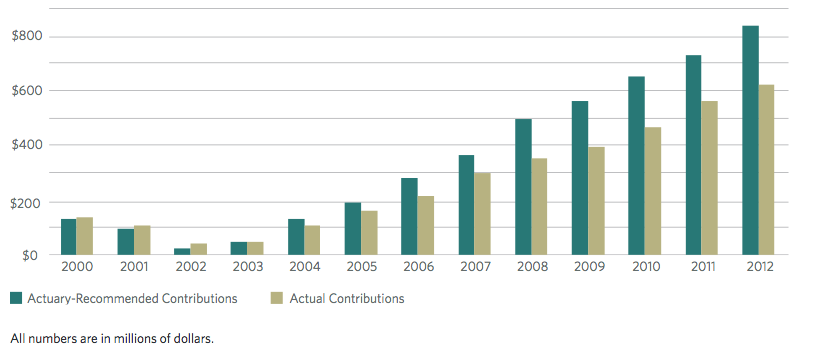

Does a person’s willingness to hold risky assets diminish as they grow older and get closer to retirement? How does aging affect portfolio choices?

A paper published in the October issue of the Journal of Pension Economics and Finance aims to tackle those questions.

The authors analyzed administrative data from an Italian defined-contribution plan spanning 2002-08. Here’s what they found:

We studied investors’ portfolio choices in a very simple real-world setup. Some results prove quite robust across all the empirical exercises we performed. In particular, we found a pronounced tendency to choose safer portfolios as people age. This effect is still there after controlling for several demographic factors, for time effects, and for the sub-fund chosen in the previous period. This result is broadly in line with other micro-evidence from the US market, and is consistent with models of life-cycle rational portfolio allocation.

[…]

The effect of age is more pronounced in the last years of the sample. This might be due to the fact that investors learn form the experience of their colleagues. Indeed, in our sample there have been periods of disappointing stock market performance. Having seen that people who retired during these bear market periods have been severely hit might have pushed investors toward a more active behaviour. A better understanding of this form of learning appears to be an interesting issue for further research.

But not all plan participants reduced risk as they approached retirement. From the paper:

Not all elderly people in our sample reduced their exposure to risk. Looking at the ones present in the sample from the start, it turns out that more than 30% of the elderly workers who were exposed to stock market risk in 2002 were still exposed to it in 2008. As the stock market events of the last decade show, an elderly worker taking risk on the stock market could pay a high price if stocks fall. This evidence suggests that life cycle funds could be a valuable instrument, given that they automatically bring all the participants toward less risky allocations as they get near to retirement (Viceira, 2007). In the Chilean system, for example, a lifecycle fund is the default option for all the workers. Moreover, the riskiest sub-funds are closed to individuals older than a certain age.

The authors also found that job position and education are factors that play into people’s risk choices:

People with a higher position tend to take more risks. This tallies with previous empirical analyses and can be consistent with optimal portfolio allocation. We also found that education has no clear impact on portfolio choices, even if it slightly increases the likelihood of switching for those in the zero-shares sub-funds. The weakness of this effect could be due to the easy set up provided by the fund, and/or to strong social interaction effects, in which the financial skills of the educated employees who make up most of our sample also benefit the few uneducated participants.

Read the entire paper, titled “the effect of age on portfolio choices: evidence from an Italian pension fund”, here.

Photo by www.SeniorLiving.Org