Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Watching that awkward moment at the end of Miss Universe 2015 on Sunday evening got me thinking about the biggest pension gaffe of the year. Earlier this month, Adam Mayers of the Toronto Star reported, $10,000 TFSA limit gone to help fund tax cut:

Friday’s Throne Speech didn’t mention Tax Free Savings Accounts (TFSAs), but federal Finance Minister Bill Morneau didn’t leave us in suspense for long.

On Monday afternoon, as part of measures to help pay for a middle-class tax cut, Morneau — cheerfully and in a brisk boardroom manner — said the $10,000 annual limit introduced by Conservative Finance Minister Joe Oliver is gone.

The good news is that the $10,000 amount stands for this year and goes into your lifetime total. But as of Jan. 1, it’s back to the future for this popular savings vehicle, dubbed the Totally Fantastic Savings Account by Wealthy Barber David Chilton. It reverts to $5,500 a year.

The Liberals argued during the election that the higher limit only benefits the rich, but I doubt the rich care one way or another about TFSAs. When you have millions to save, the $41,000 in room we all have after seven years isn’t meaningful. The rich have plenty of other ways to take care of themselves.

“It comes down to how you define ‘wealthy’ — which nobody does when making such statements,” says Dan Hallett, a financial planner and vice president of Oakville’s HighView Financial Group.

“And that’s a critical point. Certainly, those who maximize the TFSA contribution limits are more affluent than those that don’t — on average. But that doesn’t mean a higher limit only benefits the wealthy.”For middle-income Canadians, older Canadians heading into retirement and those already there, the higher limit — and any portion of it they could use — would have been helpful. Savings rates are at record lows, so encouragement to save would seem to be a good thing.

Morneau says the promised middle-class tax cut will average $330 a year for single earners and $540 per couple. He has to pay for that, and imposing a higher tax on those making over $200,000 won’t do the job alone. Rolling back the TFSA is a way to narrow the gap.Here, the new government is out of touch with the people who elected it. An Angus Reid poll in the middle of the election campaign found that 67 per cent of Canadians opposed rolling back the TFSA limit. By party, NDP supporters liked the increase more than Liberals — 63 per cent vs. 62 per cent — with Conservative supporters highest at 78 per cent.

A study by the Canadian Association for Retired People (CARP) this spring found the same thing. Two-thirds of CARP members supported the extra saving room.

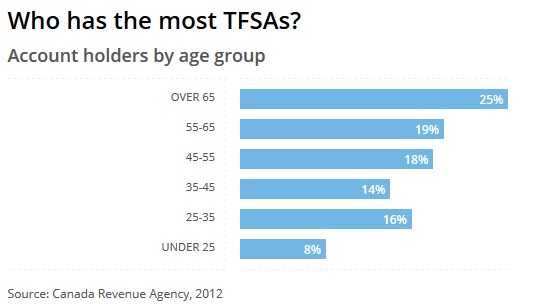

The TFSA has been of particular benefit to older Canadians. It has only been around for seven years and so is a new way to shelter a little more money in retirement. Those 55 and older hold almost half of all TFSA accounts, according to the CRA.

Strict rules force you to convert your RRSP into a Registered Retirement Income Fund (RRIF) when you turn 71. That’s because the government wants the taxes foregone when you put the money into your RRSP and got a refund.

But some older Canadians don’t need all that money to live, on so they use a TFSA to let it grow tax-free.

So here’s where we are:

- The $10,000 TFSA limit introduced this spring stands for the year. If you don’t contribute the full amount, it becomes part of your lifetime limit.

- As of Jan.1, the limit reverts to $5,500 per year, which will be indexed, which the $10,000 wasn’t.

- Morneau said indexing will allow the TFSA to retain its real value. It is set to rise in $500 increments whenever inflation erodes the value by $250.

At a 2 per cent rate of inflation, that bump should come every three years or so, since the $5,500 is worth $110 less each year. The only increase so far was in 2013. It’s unclear when the next one will be.

In the end, the new government had to make choices about how to fund its ambitious agenda. A higher TFSA, cast as a perk for the rich, was an easy choice. But what the middle class is getting in a tax cut isn’t as large as what it’s losing in a higher TFSA limit.

But some people think the TFSA rollback while historic isn’t a big deal. Jennifer Robson, an Assistant Professor at Carleton University, wrote a comment for MacLean’s, The Liberal changes to TFSA contributions were actually historic:

The new government wanted to make its first policy move in the House substantive and symbolic, but it also managed to make it historic. On Monday, the government gave notice that it will introduce a motion (a Ways and Means motion, to be precise) to cut the second federal income tax rate (applied to taxable income between $45,283 and $90,563) and create a new tax bracket applied to taxable incomes of $200,000 or more.

It’s true that this is the first time since 2001 that the basic architecture of federal tax rates has been renovated in a big way. It’s also true that if your taxable income is $45,000 or less, then this tax cut isn’t for you. Finally, yes, it’s true that a person with a taxable income of $120,000 stands to save more ($783) on their federal tax bill than a person with a taxable income of $80,000 ($582).

No, no, that’s not the historic part in my view. Look, 2001 wasn’t that long ago and I’ve written loads before about tax credits and public programs that benefit the better-off.

I’m talking about Clause 9 of the government’s motion that scales back the annual contribution room available to adults who open a Tax-Free Savings Account (TFSA) from the current $10,000 limit introduced for 2015 to the $5,500 annual limit that had done just fine before an election loomed on the horizon. Don’t forget, unused contribution room rolls over each year and there is still no lifetime cap on contributions. This means that between exemptions for home equity, lifetime capital gains rules and the TFSA, it won’t be long before most households in Canada are able to shelter virtually all of their assets from income taxation.

Back before the election, federal officials were at pains to explain that the increase in the TFSA room was well, really, really necessary, because, you see, over a quarter-million low-income Canadians (making less than $20,000 a year) had managed to max out their TFSA room under the $5,500 limit. ”Don’t you understand that these low-income people are just trying to put away some savings? Why do you hate people who are just… frugal?” With the national household savings rate stumbling along at about four per cent these days, shouldn’t we reward those who were saving roughly half of their modest annual incomes?

Well, no, and here’s why: From what I can see, the phenomenon that was offered as”‘the problem” to be fixed is likely temporary.

Looking at data from the 2012 Survey of Financial Security (Statistics Canada) when the TFSA was four years old (offering $20,000 of accumulated room for every adult in Canada) is instructive here:

– Singles and families aged 65 and older are far more likely to own a TFSA than their working-age counterparts (38-47 per cent versus 25-34 per cent respectively).

– Median TFSA balances amongst all working-age singles (under age 65) were just $5,000 (or 25 per cent of that limit) but median balances for singles aged 65+ were $15,000 (75 per cent of the limit). That’s the median, meaning that half of single seniors had TFSA balances between 76 per cent and 100 per cent of their allowable limit.

– Among couples and families, the age-related gap in median TFSA balances persists: $10,000 at the median for working-age households and $20,000 for those aged 65 or older.

– Within the working age population, there are also important age-related differences. Median TFSA values for couples or families aged 35-44 suggest median deposits of about $1,000 per year. But closer to retirement (age 55-64), household TFSA balances suggest median deposits of a little more than $3,500 per year, still well below the old $5,500 limit.

Those older households are, in the vast majority of cases, unlikely to be saving “new” money. Instead, they may well be shifting assets from one source—maybe perhaps proceeds from the sale of a family house that is now too large for their needs; or maybe this is coming from taxable RRIF income that is being recycled into a different and non-taxable registered savings account. Recall that the TFSA doesn’t offer a deduction for (most) deposits, doesn’t create new tax liability on withdrawals and is exempt for the purpose of working out the key income-tested senior’s benefit, the Guaranteed Income Supplement (GIS). Seniors with $20,000 in total personal income have too much income to receive the GIS now, but they may worry about exhausting their savings and needing the GIS later on. In these cases, shifting assets into a TFSA just makes good financial sense.

But that’s not what the TFSA was supposed to be for.

When it was introduced in 2008, the late Jim Flaherty cheerfully called the TFSA “an RRSP for everything else in your life.” His budget communications documents that year offered examples of people saving for all kinds of short- and medium-term uses like vacations and “rainy days.” The literature dating back to at least a 1987 study by the Economic Council of Canada (of which, Liberals, please give thought to reviving that creature to complement the work of a beefed-up Parliamentary Budget Officer) saw tax-prepaid savings as a way to stimulate more saving and investment by giving households choices when RRSP incentives fail. The literature doesn’t seem to have anticipated asset-shifting uses among the already-retired.

Unless the TFSA undergoes more dramatic changes like a lifetime limit, future generations of seniors are unlikely to worry much about annual caps limiting their ability to shift assets around to gain the best tax and benefit treatment. A person aged 55 today will have nearly $100,000 in TFSA room by age 65. And while today’s seniors with low income but some savings may feel cheated by an accident of policy timing, there are many other ways to address some of their concerns—flexibility on RRIF withdrawals for example.

But I still haven’t given you the punchline, have I?

The TFSA is just one among five separate tax-preferred and registered savings instruments in Canada. The first was the RRSP, introduced in 1957. When Kenneth Carter recommended scaling back RRSP limits in his 1966 report on Canadian tax reform, he was summarily ignored. Instead, we have, through relentless incremental policy choices, grown a tax and transfer system that is schizophrenic in its treatment of savings—rewarding people who already have money for saving it but often penalizing small savers. In the last 58 years, there have been exactly zero reductions to annual contribution room to any of these instruments—that is, until now.

By scaling back annual TFSA limits, the new government can keep the flexibility that tax pre-paid accounts offer without encouraging as much asset-shifting among the already comfortable. Promoting economic growth is the stated motive behind this renovation to the income tax brackets. If the government is serious about making that growth inclusive, then removing regressive incentives is a good start at breaking a 58-year trend. But it’s just a start.

Jennifer Robson raises good points in her article but I think the Liberals’ policy to rollback TFSA contributions is the dumbest most populist gaffe the Trudeau government could have done and I explicitly warned against this when I discussed real change to Canada’s pension plan:

There are other problems with the Liberals’ retirement policy. I disagree with their stance on limiting the amount in tax-free savings accounts (TFSAs) because while most Canadians aren’t saving enough, TFSAs help a lot of professionals and others with no pensions who do manage to save for retirement (of course, TFSAs are no substitute to enhancing the CPP!).

The point I’m trying to make here is that rolling back TFSA limits hurts a lot of hard working people who aren’t rich, they’re just trying to save as much money as possible for retirement because unlike the government bureaucrats that design these policies, they have no defined-benefit pension plan to rely on during their golden years.

And it’s not just hard working people with no pension getting hurt with this asinine TFSA rollback. Neil Mohindra, a public policy consultant based in Toronto wrote a comment for the National Post earlier this month, TFSA rollbacks will hurt the needy:

The debate over maintaining or rolling back the TFSA limit of $10,000 has centred on whether middle class Canadians or only the rich benefit from the higher limit. But a rollback will disproportionately affect middle and lower income Canadians with limited work histories in this country, including new immigrants and Canadians who have spent time as caregivers.

Take the following fictitious example. Jonathan, a welder by trade, immigrated to Canada in his mid-forties with $175,000 in savings. During the three years he needed to qualify for this profession in Canada, he supported himself with minimum wage jobs. Every year he places $10,000 of his savings into his TFSA, to obtain a reasonable standard of living in retirement.

In Jonathan’s case, retirement income and savings in Canada will be limited. His CPP income will be lower because of fewer qualifying years and he will have limited RRSP space and no accumulated TFSA space on arrival in Canada. He will qualify for Old Age Security because of a social security agreement between Canada and his home country that will allow Jonathan to meet the minimum eligibility criteria. Despite earning a good living as a welder, Jonathan could be at risk of having inadequate income in retirement.

Many face Jonathan’s predicament. In the five years ending 2014-2015, 1.3 million immigrants arrived in Canada, 23 per cent of them over age 40 with limited work histories in Canada. While not all immigrants have savings, many will have real assets like houses or pensions that can be converted to savings and brought to Canada. Maintaining the TFSA limit at $10,000 instead of rolling it back to $5,500 allows these new Canadians to convert more savings into tax sheltered investments, reducing any disadvantage they may have relative to other Canadians.

Returning emigrants, people who work in boom-bust industries, and anyone whose working life is disrupted by a physical or mental disability could also be at risk of inadequate retirement income. A very significant group of Canadians at risk are caregivers. Take Mary, a recently widowed 67-year-old who worked full time for five years before quitting to raise children and care for a disabled sister. She worked part-time later in life. She has a modest inheritance from her sister’s estate of $50,000, and a payout from her husband’s life insurance policy of $250,000. Accumulated TFSA space will allow her to earn investment income on these amounts, and she will make modest periodic withdrawals to supplement her retirement income.

Mary, what Statistics Canada would describe as a “sandwiched caregiver,” may be representative of a significant number of Canadians. A Statistics Canada article, based on 2012 data, noted 28 per cent of caregivers, or 2.2 million individuals were sandwiched between raising children and caregiving. The article also indicated that in 2012, 8.1 million individuals, or 28 per cent of Canadians aged 15 years and older, provided some care to a family member or friend with a long-term health condition, disability or aging needs.

In Mary’s case, it is not the annual TFSA limit that is important but the accumulated limit. In her scenario, Mary would not have anywhere near the accumulated space that she needs, since TFSAs were only introduced in 2009. It will actually take 27 years before individuals will have the accumulated space they need for this scenario even at $10,000 per year.

A Broadbent Institute report criticized higher TFSA limit for not necessarily incenting Canadians to save more, rather to shift taxable assets into TFSA accounts. Jonathan and Mary provide counter examples. Maintaining the higher TFSA limit can play a role in helping low and middle income Canadians with limited work history in Canada successfully meet retirement goals.

Nevertheless, it’s not all bad news. As provincial and territorial finance ministers gathered with their new federal counterpart in Ottawa on Sunday night to begin confronting the hard economic truths facing Canada, the good news is there seems to be enough provincial support to boost the CPP.

I can’t overemphasize how crucial it will be to bolster Canada’s retirement policy now more than ever. I’ve been warning of Canada’s perfect storm since January 2013 and think our country will experience a serious crisis in the next few years which will bring about negative interest rates and other unconventional monetary policy responses.

Importantly, this isn’t the time to rollback the TFSA contribution limit or to implement other populist policies “against the rich,” but it’s the time for the bureaucrats in Ottawa to finally get their heads out of their asses and closely examine all pension policies very carefully. Keep what works well and bolster what needs to be bolstered.

And it’s not just the rollback in TFSA limit that irks me. The age limit on converting RRSPs to RRIFs should be pushed back for seniors who continue to work in their seventies (there’s a reason why they’re working so why should they get penalized?). Also, Ottawa needs to significantly improve the registered disability savings plan (RDSP) which Jim Flaherty started to help Canadians with disabilities and parents with disabled kids to save money for their needs (the program is excellent but there should be an option to have the money managed by CPPIB).

What else? Dominic Clermont, formerly of the Caisse and now back from working at Barra in London sent me this interesting comparison to pt things in perespective:

In the UK, taxpayers can invest in an ISA which is equivalent to our TFSA. The yearly contribution limit for the fiscal year 2015-2016 is £15,240 which at current exchange rate is about $31,600 – much higher than the $10,000 which the Liberals found too high.

Interest rates are so low (you can find savings accounts paying 0.75% interest…), it doesn’t make much sense to tax small investors on such small interest. The first £1,000 of interest income is now non-taxable – that is more than $2,000/year of tax free interest income outside of the ISA (TSFA).

The maximum contribution to a pension scheme (employer or private – equivalent to our RRSP) is also much higher in the IK: £40,000 per year or about $83,000.

In Canada and particularly in Quebec, taxing the rich is always popular. The are such a minority that their vote is less important. The ultra-rich can afford to pay for the best fiscalist anyway. The regular rich can move elsewhere.

Also, a friend of mine shared this with me over the weekend on negative rates coming to Canada after he read the unintended consequences of negative interest rates in Switzerland:

“I found this article fascinating. Central Banks around the world have been experimenting with the economies of the G20 countries since the crisis. They are doing shit that they have never done before and it is clear that the world has become their Petri dish.

All of this comes from one fundamental issue – a demographic bubble of baby boomers going through the system. The world (including Canada) is completely unprepared for this new economic reality.

When push comes to shove, it is this demographic bubble that will drive the Canadian economy over the next 40 years and, unfortunately, I do not see Canadian policy preparing for this at all.

For example, the country should have increased immigration in 1990s but it did not because the unions stopped it. Instead, they invited high net worth individual to move to Canada (i.e. we want your money without you stealing our jobs). The unintended consequence of this policy was that these “high net worth individuals” came in droves, most of them Chinese and Middle Eastern, and pushed real estate prices skyward in two of our major cities to the point where no one in their 20s can buy a home.

So expect more of the same, Justin is not a visionary. He is simply a populist Prime Minister (no different than Greek PM Tsipras). He got voted in because everybody hated the other guy. He is now implementing tax policy that completely ignores reality but will secure his populist promises (tax the rich – give to the poor). When the next election comes, he will be faced with an opponent who will try to one-up him and the race to bottom will continue.

My reaction to Justin’s tax policy. At a 53% marginal rate, I have a whole bunch of tax advisors looking at what to do to minimize it. I am sure that they will find a loophole than hasn’t been plugged yet. If they don’t, I will just adapt and perhaps leave Canada when I retire with my future tax dollars in hand.”

I’m sure a lot of people sick and tired with dumb policies which supposedly favor the poor share my friend’s views. Interestingly, we share conservative economic views and he completely agrees with me that bolstering the CPP is smart pension and economic policy:

“It’s not about left wing or right wing politics. Enhancing the CPP is just a smart move. You’re right, companies are unloading retirement risk on to the state and unless something is done, this demographic nightmare I’m talking about will explode in Canada and we’ll see a huge rise in social welfare costs.”

I hope someone in Ottawa will share this comment with the Privy Council and other offices in Ottawa. Unfortunately, the Conservatives made plenty of pension gaffes (and other gaffes) but raising the contribution limit on the TFSA wasn’t one of them.

Photo by Roland O’Daniel via Flickr CC License