Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

John Tilak and Matt Scuffham of Reuters report, Canada’s CPPIB pension fund plans farmland retreat:

Canada Pension Plan Investment Board (CPPIB) has decided against making further investments in farmland and is open to selling its existing portfolio after reviewing the operations, people familiar with the matter told Reuters this week, a shift in strategy after some local farmers voiced concerns.

CPPIB began buying farmland in North America in 2012 and has since purchased about 120,000 acres in the United States and a similar amount in Canada. The country’s biggest public pension fund purchased 115,000 acres of Saskatchewan farmland from Assiniboia Farmland LP in 2013 for C$128 million ($95 million)and had intended to invest another C$500 million in Canadian farmland over a five-year period.

However, its plans met with a backlash from some local farmers who believed they would be squeezed out of buying land themselves and feared rising rents if the CPPIB pursued its mandate to maximize returns for Canada’s pensioners.

Those concerns eventually prompted the Saskatchewan government to ban some institutional investors from buying farmland in the province, whose plains usually grow more wheat than Argentina, thwarting CPPIB’s plans for expansion.CPPIB, a late entrant to farmland business, declined to comment specifically on the changes, but the fund’s global head of public affairs, Michel Leduc, said:

“We assess performance of each investment program with that in mind as well as fit within our total portfolio approach, contribution to diversification and desired return-risk profile.”CPPIB, which had C$298 billion ($219.62 billion) under management at the end of 2016, oversees the national pension fund on behalf of 20 million Canadians.

The fund’s move stands to be good news for some farmers and not so good for others. Those who want to expand the size of their farms are winners because they have one less tough bidder to compete against, but those hoping to sell the farm and retire may find fewer buyers.

Although CPPIB continued to buy farmland in the United States, plans to purchase farmland in Australia, New Zealand and Brazil also failed to materialize. Frustrated by the fund’s lack of progress, CPPIB Chief Executive Mark Machin recently ordered a review of the business led by its global head of real estate investments, Graham Eadie, the people told Reuters.

The sources spoke on condition of anonymity because the matter is confidential.

Eadie’s review concluded the business was not sufficiently scalable to justify further investment. As a result, CPPIB has decided not to acquire more farmland and is open to selling what it already has, the sources added.

It is not clear whether the fund is actively seeking buyers.

CPPIB’s decision comes as some large pension funds continue to look for opportunities in the sector. Wealth funds of Gulf Arab states have been buying farmland in developing nations to ensure food security. Recently, some of the Australian pension funds have started buying farmland after staying away as the local farms were often too small in value to be of interest to the A$2 trillion ($1.51 trillion) pension fund industry.

Global farmland investors range from pension plans like CPPIB to companies including Ontario-based Bonnefield and U.S.-based real estate investment trust Farmland Partners Inc.

The CPPIB has decided instead to focus on the processing, delivery and storage of agricultural products following last year’s acquisition of a 40 percent stake in Glencore Plc’s agricultural business for $2.5 billion.

As part of the changes, the fund has parted company with Angus Selby, who was based in London and had led the bank’s global investment strategy for agriculture and farmland for five years, the people added. The fund’s agriculture trading group was also laid off at the end of last year, one of the people said. Selby was not available for comment and CPPIB declined to comment.

Let me begin my comment by stating I agree with CPPIB’s decision to exit farmland. Graeme Eadie (not Graham Eadie), CPPIB’s Senior Managing Director & Global Head of Real Assets, is right, it’s not scalable and in my opinion, CPPIB is better off focusing on other private markets right now, like infrastructure, real estate, private equity and private debt.

A little over two years ago, I openly questioned whether farmland is a good fit for pensions, stating the following:

[…] the bubble in farmland is bursting and second, when it bursts and farmers walk away from their leases, it could potentially mean costly and lengthy court battles pitting landowners (ie. endowment funds and public pension funds like CPPIB and PSPIB which also invests in farmland) against farmers. That doesn’t look good at all for pensions.

All this to say, while it’s really cool following Harvard’s mighty endowment into timberland and farmland, when you come down to it, managing and operating farmland is a lot harder than it seems on paper and the risks are greatly under-appreciated. Add the potential of global deflation wreaking havoc on all private market investments and you understand why I’m skeptical that farmland is a good fit for pensions, even if they invest for the long, long run.

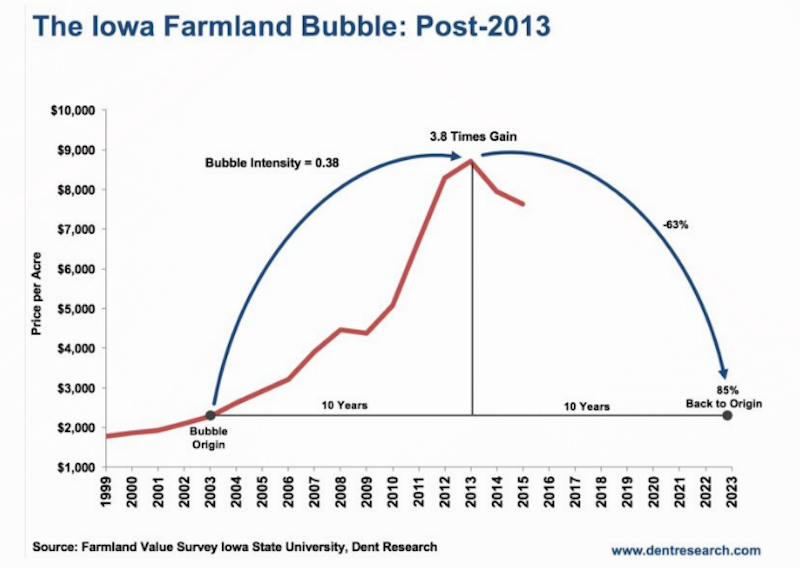

No doubt about it, the farm bubble burst, peaking around 2013 (click on image):

Glenn Kauth, editor of Benefits Canada, recently reported on navigating the complexities of investing in agriculture:

While a recommendation that the government reverse course on maintaining the retirement age at 65 was one of the headline suggestions to come out of the recent report from the federal advisory council on economic growth, a key focus was on four sectors the group felt have a high potential for growth in Canada. One of the four sectors was agriculture.

With US$26.1 billion in agricultural exports in 2015, Canada is already the world’s fifth-largest exporter in that sector, the report noted. The growth of the global middle class signals further growth potential, with worldwide demand expected to rise by 70 per cent by 2050. In his recent budget, Finance Minister Bill Morneau embraced the call to focus on agriculture. As part of the budget’s innovation and skills plan, the government is targeting a rise in exports in the agricultural and food category to $75 billion a year by 2025.

But while J.P. Gervais, vice-president and chief agricultural economist at Farm Credit Canada, says recent years “have been great” for agriculture in Canada, he notes predictions are for a decline of up to four per cent for farm cash receipts in 2016. The reasons, according to Gervais, include weather issues in some regions that have led to poor yields for certain crops. And while falling commodity prices have put a damper on the U.S. agricultural sector, Gervais says the decline of the Canadian dollar has helped to shield Canadian farmers from some of the pressures. “Anything but cereals is generally doing well,” he says, noting crops such as oilseeds and canola are doing better.

Focus on farmland

While Canadian agriculture shows some promise, institutional investors have been active on the global front, particularly when it comes to farmland. The activity started to pick up in 2012, when the Caisse de dépôt et placement du Québec and the British Columbia Investment Management Corp. both invested in an agricultural company launched by the U.S.-based Teachers Insurance and Annuity Association of America-College Retirement Equities Fund (TIAA-CREF). The company, TIAA-CREF Global Agriculture LLC, included $2 billion in commitments to invest in farmland in the United States, Australia and Brazil.

The move followed an investment in 2011 by the Alberta Investment Management Corp. in timberland assets owned by Australia’s Great Southern Plantations. The Alberta fund’s plan is to boost its investment in part by converting some of the land to a higher use, such as agriculture. More recent moves by Canadian plans include the Public Sector Pension Investment Board’s 2015 investment in cattle properties through Queensland-based Hewitt Cattle Australia.

Australia, in fact, seems to be a key focus for Canadian pension funds’ agricultural interests. In 2014, the Ontario Teachers’ Pension Plan invested in Aroona Farms, a grower of almonds that operates two properties in the states of Victoria and South Australia. The plan owns a 99 per cent stake in Aroona Farms.

“As part of our natural resources, we have an agriculture strategy,” said Bjarne Graven Larsen, executive vice-president and chief investment officer at the Teachers’ plan, during an announcement in March of the organization’s annual results for 2016. “And we like that a lot because it diversifies. It gives us, at least to some extent, exposure to inflation in food prices and land as well.”

While farm values have been on a long-term upswing, they’ve been on a recent downturn in one key market, the U.S. Midwest. The overall decline in U.S. farm values in 2016 was just 0.3 per cent, according to the U.S. Department of Agriculture. The declines were higher, however, in the midwestern states. Karen Dolenec, global head of real assets at Willis Towers Watson in London, England, notes Australia has generally been attractive for agricultural investments, while South America has good potential for boosting properties to higher uses.

When it comes to the merits of various crops, Dolenec emphasizes diversification. Options include investing in annual row crops that require planting every year, versus permanent ones, such as vineyards, orchards and nuts. Permanent crops, says Dolenec, can require higher upfront and ongoing investments but they do offer an investor the opportunity to add value.

At the Ontario Teachers’ plan, Graven Larsen says the focus is on slower-growing crops. “We like almond, avocado, something of the not-so-fast crop, so far,” he said last month.

How to invest is one of the key questions when it comes to deciding whether to acquire farmland as a landlord renting out the property to farmers or with more of an active role. For Canadian pension plans, the typical approach has been to be a landlord, as is the case with investments like the TIAA-CREF funds. But in Canada, a smaller player on the scene, Area One Farms Ltd., offers what president and chief executive officer Joelle Faulkner describes as a joint venture that’s “more like private equity in that we’re equity partners with the farmer.”

“They put in equity and we put in equity and they co-own,” says Faulkner, noting both owners share in the profits, with an extra portion going to the farmer for running the operation.

Investors get access to higher-quality land that often isn’t available on the open market, according to Faulkner. The idea, she adds, is to boost farm productivity. “We do upgrade about half of our portfolio.”

Faulkner expects Area One Farms, which started in 2012, to close the deal on its third fund soon and she says it’s now seeing some institutional interest. While it targets a return of 15 per cent to investors, Faulkner admits that’s largely on the capital appreciation side. The balance would be from a targeted three to five per cent from crop income.

On the other side, Justin Ourso, managing director and portfolio manager at TIAA Investments, says renting out farmland can be very “fixed income-like.” Investors, he notes, can remove themselves from the volatility of farming and avoid production risks.

The challenges

While rising farmland values are good news for investors already in the area, they can be a challenge for those looking to buy now, an issue Dolenec acknowledges is a concern but one she says is true of all real assets.

And then there are the legal difficulties. Many governments are protective about foreign investment in farmland. Saskatchewan, for example, prohibits foreigners and publicly traded entities from owning more than four hectares of land. According to Faulkner, the rules initially limited pension fund involvement in Saskatchewan farmland to the Canada Pension Plan Investment Board, which in 2013 acquired the assets of Assiniboia Farmland LP. The transaction, which involved a portfolio of more than 45,000 hectares of farmland, included an initial equity investment of about $120 million. The board then bought 12 more farms for $33.7 million.

While the board had been planning additional investments in Canadian farmland, the Saskatchewan government, amid concerns about the impact of inflated farm prices, put a halt to further purchases in 2015. Asked about the board’s investments in agriculture, spokesman Dan Madge declined to comment. “Agriculture isn’t something we’re focused on right now,” he told Benefits Canada.

Pension fund involvement is even more controversial in countries like Brazil. Canadian groups, including several unions and non-profit organizations, have taken investors like the Caisse and bcIMC to task for their involvement in Brazil through TIAA-CREF Global Agriculture LLC and demanded they refrain from further investments in its funds. The controversies centre on concerns about violence and land conflicts in areas where the fund has been acquiring farms.

Asked about the allegations, Ourso questions their accuracy and says the TIAA-CREF fund has worked to address the concerns. “We take those allegations quite seriously,” he says.

“We don’t believe that they are accurate.”

The actions the fund has taken include title searches to verify ownership for a minimum of 20 years and an assessment of legal, civil, tax or criminal matters related to the seller of the land. In Brazil, it reviews licences permitting land conversion to agriculture and satellite images to assess historical uses.

Devlin Kuyek, a researcher at Grain, a non-profiit organization that has criticized farmland investments by pension plans in Brazil, acknowledges that TIAA-CREF has made strides on disclosing the locations of its holdings in that country. The organization still has concerns about the acquisitions, however. “If TIAA is sincere about its intentions, then it should not be investing in any part of the world where there are land conflicts and ongoing processes of agrarian reform,” he says.

And beyond the legal and financial concerns is a more practical one. According to Dolenec, the fund offerings available to institutional investors remained limited, despite the interest in agriculture over the past decade.

“The range of offerings has really not grown as quickly as people expected,” she says.But as Dolenec notes, there are other opportunities in agriculture besides farmland. Last year, for example, the CPPIB announced it was buying a 40 per cent stake in Glencore Agricultural Products, a global grains and oilseeds company whose operations include processing, storage, logistics and marketing.

As for farmland, the investment opportunities have typically been on the small side, Ontario Teachers’ Graven Larsen noted last month.

Climate change, he added, is another big consideration. “We will continue to focus on that area, but it’s not going to be huge,” he said in reference to agriculture.“But it’s probably going to be larger than today.”

Nobody knows more about the challenges of investing in farmland than TIIA, one of the largest global investors in farmland.

Recently, protesters rallied outside TIAA’s New York offices to protest its farmland deals and TIAA’s investment services clients – 14,000 of them – and a broad coalition of international organizations requested last week that TIAA address material financial risks in how the firm’s manages its global agriculture investments:

TIAA is one of the largest global investors in farmland, with over 607,000 hectares under management in the U.S. and around the world. These farmland assets are worth about USD 8 billion. In aggregate, they represent about 1 percent of TIAA’s overall assets under management.

To mitigate this material financial risks, back in 2011, TIAA signed the Farmland Principles for responsible investing focusing on robust investment and sustainable management of farmland assets. Now this TIAA–CREF client–led coalition is requesting that TIAA demonstrate compliance with these principles in how they manage their assets under management.

This is because recent reports, described in The New York Times in 2015, claim that TIAA has promoted land speculation by investing hundreds of millions of dollars in Brazil’s cerrado wooded prairielands. These TIAA clients allege that the firm’s investments lead to land speculation in Brazil that contravenes Brazilian law restricting land ownership by foreign corporations.

Similarly, according to TIAA’s 2015 report Responsible Investing in Farmland, the firm owns 256,300 hectares of farmland in Brazil. Their clients are extremely concerned that reports of land grabbing and human rights violations in Brazil are systemic.

Beyond its direct land investments, as of March 20, 2017, TIAA has at least USD 170 million invested in SE Asian palm oil companies, some of who also represent similar material financial risks to TIAA and its clients.

As reported by Chain Reaction Research, Pepsico and TIAA face financial risks from agricultural investments and supply chains.

When you read these articles, you realize that investing in farmland isn’t clean and smooth, it’s fraught with all sorts of political, legal and financial risks.

Yes, on a smaller scale, Ontario Teachers’ CIO Graven Larsen is right, you can invest in some nice deals. I too like almonds, avocados, and walnuts, all are regular staples of my daily diet.

But investing in farmland on a much larger scale is fraught with all sorts of risks, so maybe a better approach is the private equity approach where you partner up with local experts and farmers who have an equity stake in the investment (like Area One Farms in Canada). Another approach is what CPPIB did with its massive Glencore deal.

All I know is I think CPPIB made a wise decision to retreat from farmland, especially now that it’s preparing for landing and taking a much more defensive stance, waiting for the right moment to pounce on opportunities as they arise in the future.

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712