Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

The Canada News Wire reports, Canadian pensioners not living as long as expected:

New research finds longevity for Canadian pensioners is lower than anticipated – which may actually be costing defined benefit (DB) plan sponsors.

Canadian male pensioners are living about 1.5 years less than expected from age 65, according to the latest data from Club Vita Canada Inc. – the first dedicated longevity analytics firm for Canadian pension plans and a subsidiary of Eckler Ltd. Female pensioners are living about half a year less than expected.

“Based on our data, some DB plans are overestimating how long their members are currently living and are therefore taking an overly conservative approach to funding their liabilities,” explains Ian Edelist, CEO of Club Vita Canada. “Correcting that overestimation could reduce actuarial reserves by as much as 6% – improving Canadian pension funds’ and their plan sponsors’ balance sheets just by using more accurate, granular and up-to-date longevity assumptions.”

The data comes from Club Vita Canada’s first annual and highly successful longevity study completed in 2016 – one of the largest, most rigorous research studies on the impact of longevity on defined benefit pension and post-retirement health plans.

The newly created “VitaBank” pool of longevity data (provided by Club Vita Canada members) spans a wide range of industries and geographic regions in both the public and private sectors. VitaBank is currently tracking more than 500,000 Canadian pensioners from over 40 pension plans. Unlike the most widely used study to set longevity expectations – the Canadian Pensioners’ Mortality (CPM) study, which relies on data up to 2008 – VitaBank includes fully cleaned and validated data up to 2014.

The Club Vita Canada study brings to the Canadian pension market leading-edge modelling techniques already used by the insurance industry and in other countries. Club Vita U.K. recently released similar results, noting £25 billion could be wiped off the collective U.K. DB deficit by using more accurate longevity assumptions.

“Naturally, the ultimate cost of a pension plan will be determined by how long its members actually live. But assumptions made today really do matter for such long-duration commitments,” explains Douglas Anderson, founder of Club Vita in the U.K. “Club Vita’s data gives DB plan sponsors the tools they need to evaluate their willingness to maintain their longevity risk or offload that risk to insurers.”

About Club Vita Canada Inc. (clubvita.ca)

Club Vita Canada Inc. was created by Eckler Ltd. It is an extension of Club Vita LLP, a longevity centre of excellence launched in the U.K. in 2008 by Hymans Robertson LLP. By pooling robust data from a wide range of pension plans, Club Vita provides its members with leading-edge longevity analytics helping them better measure and manage their retirement plan.

About Eckler Ltd. (eckler.ca)

Eckler is a leading consulting and actuarial firm with offices across Canada and the Caribbean. Owned and operated by active Principals, the company has earned a reputation for service continuity and high professional standards. Our select group of advisers offers excellence in a wide range of areas, including financial services, pensions, benefits, communication, investment management, pension administration, change management and technology. Eckler Ltd. is a founding member of Abelica Global – an international alliance of independent actuarial and consulting firms operating in over 20 countries.

I recently discussed life expectancy in Canada and the United States when I went over statistics on gender and other diversity in the workplace, noting this:

Statistics are a funny thing, they can be used in all sorts of ways, to inform and disinform people by stretching the truth. Let me give you an example. Over the weekend, I went to Indigo bookstore to buy Michael Lewis’s new book, The Undoing Project, and skim through other books.

One of the books on the shelf that caught my attention was Daniel J. Levitin’s book, A Field Guide to Lies: Critical Thinking in the Information Age. Dr. Levitin is a professor of neuroscience at McGill University’s Department of Psychology and he has written a very accessible and entertaining book on critical thinking, a subject that should be required reading for high school and university students.

Anyways, there is a passage in the book where he discusses the often used statistic that the average life expectancy of people living in the 1850s was 38 years old for men and 40 years old for women, and now it’s 76 years old for men and 81 for women (these are the latest US statistics which show life expectancy declining for the first time since 1993. In Canada, the latest figures from 2009 show the life expectancy for men is 79 and for women 83, but bad habits are sure to impact these figures).

You read that statistic and what’s the first thing that comes to your mind? Wow, people didn’t live long back then and now that we are all eating organic foods, exercising and have the benefits of modern medical science, we are living much longer.

The problem is this is total and utter nonsense! The reason why the life expectancy was much lower in 1850 was that children were dying a lot more often back then. In other words, the child mortality rate heavily skewed the statistics but according to Dr. Levitin, a man or woman reaching the age of 50 back then went on to live past 70. Yes, modern science has increased life expectancy somewhat but not nearly as much as we are led to believe.

Here is another statistic that my close friend, a radiologist who sees all sorts of diseases told me: all men will get prostate cancer if they live long enough. He tells me a 70 year old man has a 70% chance of being diagnosed with prostate cancer, an 80 year old man has an 80% chance and a 90 year old man has a 90% chance.”

Scary stuff, right? Not really because as my buddy tells me: “The reason prostate cancer isn’t a massive health concern is that it typically strikes older men and moves very, very slowly, so by the time men are diagnosed with it, chances are they will die from something else.”

Of course, the key word here is “typically” because if you’re a 50 year old male with high PSA levels and are then diagnosed with prostate cancer after a biopsy confirms you have it, you need to undergo surgery as soon as possible because you might be one of the unlucky few with an aggressive form of the disease (luckily, it can be treated and cured if caught in time).

So, much like the US, it seems the recent statistics on life expectancy in Canada are not that good. Again, you need to be very careful interpreting the data because the heroin epidemic has really skewed the numbers in both countries (much more in the US).

But let’s say the folks at Club Vita Canada and Eckler are doing their job well and Canadian pensioners are living less than previously thought. Does that mean that Canadian DB plans are overestimating their liabilities?

Yes and no. Go read an older comment of mine on whether longevity risk will doom pensions where I stated:

I actually forwarded [John] Mauldin’s comment to my pension contacts yesterday to get some feedback. First, Bernard Dussault, Canada’s former Chief Actuary, shared this with me:

True, longevity is a scary risk, but not as much as most think, the reason being that the calculations of pension costs and liabilities in actuarial reports take into account future improvements in longevity.

For example, as per the demographic assumptions of the latest (March 31, 2011) actuarial report on the federal public service superannuation plan (http://www.osfi-bsif.gc.ca/Eng/Docs/pssa2011.pdf), the longevity at age 75 in 2011 is projected to gradually increase by about 1 year in 10 years (2021). For example, if longevity at age 75 was 12.5 in 2011, it is projected as per the PSSA actuarial report to be about 13.5 in 2021

This 1 year increase at age 75 over 10 years is much less than the average 1year increase at birth every 4 years over the 20th century reported by the Society of Actuaries (SOA). However, this is an apple/orange comparison because longevity improvements are always larger at birth than at any later age and were much larger in the first half of the 20th century than thereafter than at any later age.

Bernard added this in another email correspondence where he clarified the above statement:

Annual longevity improvement rates are assumed to apply for the whole duration of the projection period under any of the periodical actuarial reports on the PSSA, i.e. for all current and future contributors and pensioners.

Moreover, the federal public service superannuation plan is actuarially funded, which means that each generation/cohort of contributors pays for the whole value of all of its accrued benefits. In other words, the financing of the plan is such that there is essentially no inter-generational transfer of pension debt from any cohort to the next.

Second, Jim Keohane, President and CEO of the Healthcare of Ontario Pension Plan (HOOPP), sent me his thoughts:

I am not sure how longevity improvements will play out over the coming decades and neither does anyone else. I wouldn’t dispute the facts being quoted in this article, but what I would point out is that these issues are not exclusive to DB plans. They are problems for anyone saving for retirement whether they are part of a DB plan a DC plan or not in any plan. DB plans get benchmarked against their ability to replace a portion of plan members pre-retirement income (typically 60%). If you measured DC plans on the same basis they are in much worse shape, in fact, they only have about 20 to 25% of the assets needed to produce that level of income.

I would also add that Canadian public sector pension plans are in much better shape than their U.S. Counterparts. We use realistic return assumptions and are in a much stronger funded position.

Third, Jim Leech, the former CEO of Ontario Teachers’ Pension Plan (OTPP) and co-author of The Third Rail, sent me this:

Very consistent with my thoughts/observations. It is a shame that “short term” motivations (masking reality by manipulating valuations, migration from DB to DC, elimination of workplace plans altogether, kicking the can down the road, etc) have taken over what is supposed to be a “long horizon” instrument (pension plan).

But Jim Keohane makes a good point – this applies ONLY to DB valuations. Anyone with DC (RRSP), ie. most Canadians, is really jiggered by longevity increases.

No doubt about it, the Oracle of Ontario, HOOPP and other Canadian pensions use much more realistic return assumptions to discount their future liabilities. In fact, Neil Petroff, CIO at Ontario Teachers once told me bluntly: “If U.S. public pensions were using our discount rate, they’d be insolvent.”

Mauldin raises issues I’ve discussed extensively on my blog, including what if 8% is really 0%, the pension rate-of-return fantasy, how useless investment consultants have hijacked U.S. pension funds, how longevity risk is adding to the pressures of corporate and public defined-benefit (DB) pensions.

Mauldin isn’t the first to sound the alarm and he won’t be the last. Warren Buffett’s dire warning on pensions fell largely on deaf ears as did Bridgewater’s. I knew a long time ago that the pension crisis and jobs crisis were going to be the two main issues plaguing policymakers around the world.

And I’ve got some very bad news for you, when global deflation hits us, it will decimate pensions. That’s where I part ways with Mauldin because longevity risk, while important, is nothing compared to a substantial decline in real interest rates.

Importantly, a decline in real rates, especially now when rates are at historic lows, is far more detrimental to pension deficits than people living longer.

What else did Mauldin conveniently miss? He ignores the brutal truth on DC pensions and misses how the ‘inexorable’ shift to DC pensions will exacerbate inequality and pretty much condemn millions of Americans to more pension poverty.

The important point is that last one, a decline in interest rates is far, far more damaging to pension liabilities than an increase in longevity risk.

Last year, I wrote a comment on why ultra low rates are here to stay, and San Francisco Fed President John Williams penned a note today that pretty much agrees with me:

The decline in the natural rate of interest, or r-star, over the past decade raises three important questions. First, is this low level for the real short-term interest rate unique to the U.S. economy? Second, is the natural rate likely to remain low in the future? And third, is this low level confined to “safe” assets? In answer to these questions, evidence suggests that low r-star is a global phenomenon, is likely to be very persistent, and is not confined only to safe assets.

So, if you ask me, I wouldn’t read too much into this latest study stating Canadian pensioners are living less than previously thought and Canadian DB plans are “overestimating” their liabilities (persistent low rates = persistent pension deficits).

Worse still, the stakeholders of these DB plans might take this data and twist it to their advantage by asking to lower the contribution rate of their plans. This would be a grave mistake.

Lastly, I want to bring something to your attention. Last week, after I wrote my comment on a lunch with PSP’s André Bourbonnais, where I stated that the Chief Actuary of Canada is rightly looking into whether PSP’s 4.1% real return target is too high, I received an email from Bernard Dussault, Canada’s former Chief Actuary, stating he didn’t agree with me or others that PSP’s target rate of return needs to be lowered.

Specifically, Bernard shared this with me:

I still do not understand why “suddenly” investment experts (including Keith Ambachtsheer) think that the expected/assumed long term real rate of return will decrease compared to what it has been expected/assumed for so many years in the past.

I look forward to Bourbonnais’ and the Chief Actuary’s rationale if they were to reduce the 4.1% rate below 4.0%.

The rationale I used for the 4% I assumed for the CPP and the PSPP when I was the Chief Actuary is briefly described as follows in the 16th actuarial report on the CPP:

The CPP Account is made of two components: the Operating Balance, which corresponds in size to the benefit payments expected over the next three months, and the Fund, which represents the excess of all CPP assets over the Operating Balance.

In accordance with the new policy of investing the Fund in a diversified portfolio, the ultimate real interest rate assumed on future net cash flows to the Account is 3.8%. This rate is a constant weighted average of the real unchanged rate of 1.5% assumed on the Operating Balance and of the real rate of 4% which replaces the rate of 2.5% assumed on the Fund in previous actuarial reports.

The long term real rate of interest of 4% on the Fund was assumed taking into account the following factors:

- from 1966 to 1995, the average real yield on the Québec Pension Plan (QPP) account, which has always been invested in a diversified portfolio, is close to 4%;

- as reported in the Canadian Institute of Actuaries’ (CIA) annual report on Canadian Economic Statistics, the average real yield over the period of 25 years ending in 1996 on the funds of a sample of the largest private pension plans in Canada is close to 5%, resulting from a nominal yield of about 11.0% reduced by the average increase of about 6% in the Consumer Price Index;

- using historical results published by the CIA in the Report on Canadian Economic Statistics, the real average yield over the 50-year (43 in the case of mortgages) period ending in 1994 is 4.03% in respect of an hypothetical portfolio invested equally in each of the following five areas: conventional mortgages, long term federal bonds (Government of Canada bonds with a term to maturity of at least 20 years), Government of Canada 91-day Treasury Bills, domestic equities (Canadian common stocks) and non‑domestic equities (U.S. common stocks). The assumed real rate of 4% retained for the Fund is therefore deemed realistic but erring on the safe side, especially considering that:

Ø replacing federal bonds by provincial bonds in this model portfolio would increase the average yield to the extent that provincial bonds carry a higher return than federal bonds; and

Ø the 3-month Treasury Bills, which bear lower returns, would normally be invested for the Operating Balance rather than the Fund.

From a larger perspective, assuming a real yield of 4% on the CPP Fund means that the CPP Investment Board would be expected to achieve investment returns comparable to those of the QPP and of large private pension plans.

On the other hand, I think I heard Bourbonnais saying last year at a presentation of the PSP annual report to the Public Service Pension advisory Committee (and I could well have misheard or misinterpreted what he said) that he was reducing the proportion of equities in the PSP fund in order to reduce the volatility/fluctuation of the returns.

If he is really doing this, then that would be a valid reason for reducing the expected 4.1% return. Besides, if he is doing this, I opine that this is not consistent with the PSP objective to maximize returns. Indeed, a more risky investment portfolio carries higher volatility though BUT it is coupled with a higher long term average return (which both the CPP and the PSP funds have achieved on average over at least the last 15 years).

As I explained to Bernard, PSP Investments and other large Canadian pensions are indeed reducing their proportion in public equities precisely because in a historically low rate environment, the returns on public equities will be lower and more importantly, the volatility will be much higher.

I also told him that given my long-term forecast of global deflation, I think more and more US and Canadian pensions should lower their target rate and that the contribution rates should rise.

Of course, someone may claim the only reason PSP and others want to lower their actuarial target rate of return is because it lowers their bar to attain their bogey and collect millions in compensation.

I’m not that cynical, I think there are legitimate reasons to review this target rate of return and I look forward to seeing the Chief Actuary’s report to understand his logic and why he thinks it needs to be lowered.

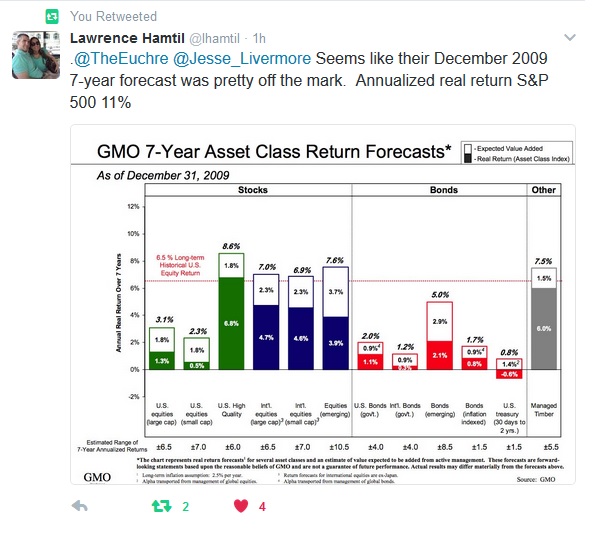

I would also warn all of you to take GMO’s 7-year asset class return projections with a shaker of salt (click on image below):

GMO may be right but I never bought into this nonsense and I’m not about to begin now. I guarantee you seven years from now, they will be way off once more!

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712