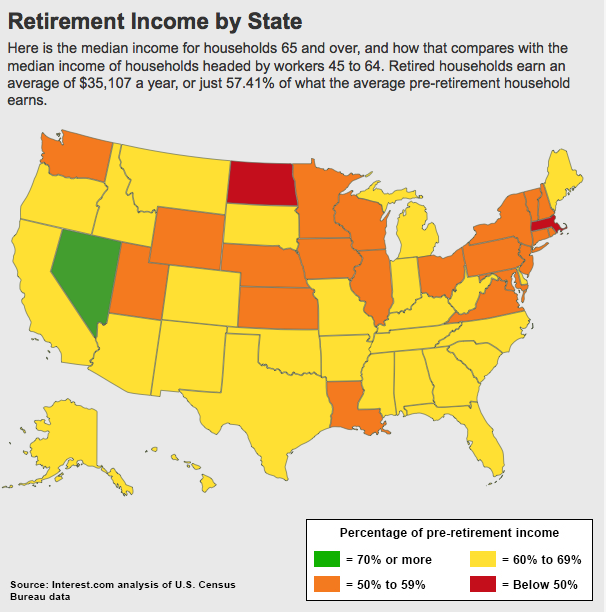

Two studies came out earlier this week that shed further light onto the challenges facing Americans entering retirement.

The Joint Center for Housing Studies of Harvard University (JCHS) released a study on the housing needs of retirees, and the Federal Reserve Board issued its Survey of Consumer Finances (SCF), which gives insights into the income of retirees as well as their participation in retirement plans. Money magazine did a nice job summarizing the findings:

The Harvard study found that our existing housing stock is ill-suited to meet seniors’ needs, including affordability, accessibility, social connectivity and support services. And high housing costs are eating into the ability of low-income older adults to pay for necessities like food and healthcare.

Housing is the largest expenditure in most household budgets, and so is a linchpin of financial security and well-being. “It’s really at the nexus of your financial health, physical health and healthcare,” says Jennifer Molinsky, research associate at the JCHS and principal author of the study.

Harvard found that a third of adults over age 50 pay more than 30% of their income for housing—including 37% of people over age 80. Harvard defines that group as “housing cost burdened.” Another group of “severely burdened” older Americans spend more than 50% of income on housing. That group spends 43% less on food, and 59% less on healthcare, compared with households that can afford their housing.

Homeowners are much less likely to be cost-burdened than renters, the study found. But more homeowners are carrying mortgages well into retirement. More than 70% of homeowners aged 50 to 64 were still paying off mortgages in 2010.

The Federal Reserve Board also released its Survey of Consumer Finances (SCF). The findings, explained by Money:

The Federal Reserve findings on middle-class retirement prospects are equally troubling. Despite the economy’s gradual mending, the SCF found a widening gap in income and net worth. The top 10% of households was the only income band registering rising income (up 2% since 2010). Households between the 40th and 90th percentiles of income saw little change in average real incomes from 2010 to 2013. And the rate of homeownership was 65%, down from 69% in 2004 and 67% in 2010.

Ownership of retirement plan accounts also fell sharply. In the bottom half of income distribution, just 40% of households owned any type of account—IRA, 401(k) or traditional pension—in 2013, down from 48% in the 2007 survey. The Fed attributes the drop mainly to declining IRA and 401(k) coverage, since defined benefit coverage remained flat. Meanwhile, coverage in the top half of income distribution was much higher. In the top 10%, 95% of families are covered.

Overall, the average value of retirement accounts jumped a substantial 10% from 2010 to 2013, to $201,300. The Fed attributed that to the strong stock market and larger contributions. But for the lowest-income group that owned accounts, the average combined IRA and 401(k) value was just $39,100—and that is down more than 20% from 2007.

There’s a growing debate about whether a retirement crisis is real or imagined. These numbers will add to that debate, but will likely do little to resolve it. The Harvard study was funded in part by the AARP Foundation, an affiliation that critics will use to discredit the study’s conclusions.

Photo by www.SeniorLiving.Org