Leo Kolivakis is a blogger, trader and independent senior pension and investment analyst. This post was originally published at Pension Pulse.

Geoff Cutmore and Nyshka Chandran of CNBC report, Canada Pension Plan looks to raise its bet on China:

China’s gradual market liberalization may be good news for Canadian pensioners.

Canada Pension Plan Investment Board (CPPIB), the country’s largest pension fund, currently has 4 percent of its portfolio in the mainland — a figure that president and CEO Mark Machin said is too low for a globally diversified portfolio such as his.

But he plans to increase that share as the world’s second-largest economy opens itself up.

“We want to significantly increase our investment here over the long term,” he said, explaining that his fund is “substantially” underweight relative to GDP, but not necessarily relative to available market cap.

Last month, the People’s Bank of China allowed foreign investors to hedge bond positions in the foreign exchange derivatives market — a move that many strategists deemed significant to overall market reform.

“China is now by many measures the third-biggest bond market in the world at around $7 trillion, so allowing that to be more accessible to capital is yet another aspect of making this a more investable place,” Machin told CNBC at the China Development Forum in Beijing.

“We’re value investors and we’re super long term. We like to say a quarter for us is 25 years, not three months,” Machin said. “We don’t necessarily need our money back for immediate use, so I think we’re seen as relatively friendly capital, and therefore our access is reasonably good here.”

CPPIB is particularly big on Chinese e-commerce and despite the dominance of giants such as Alibaba and Tencent, Machin said he believes the sector remains exciting.

Below those large behemoths is an ecosystem of start-ups, Machin explained: “The ecosystem around these large companies is part of the secret source of innovation in this country…China’s been very thoughtful about creating the ingredients of innovation, which is creating more opportunities for all types of companies, whether it’s e-commerce or others, to bloom.”

As a long-term investor in a fast-changing market, it’s key for CPPIB to speedily identify early-stage trends, he continued.

“It now takes very little money to develop a company given the amount of cloud computing capacity…you can get a company some market for very little money, very very quickly and have a very disruptive impact.”

Last week I discussed why the Caisse and CPPIB are investing in Asian warehouses in Singapore and Indonesia noting the following:

I think it’s pretty self-explanatory. The Caisse and CPPIB are betting on the demand from the rise of e-commerce and a burgeoning middle class in southeast Asia. This is a long-term bet and if you’ve been paying attention to e-commerce trends in North America, you can bet the exact same thing will happen in Asia but with exponential growth.

Canada’s large pension funds are competing with large private equity firms for these logistic warehouses. They not only provide great growth potential, they are pretty much all leased up and will provide stable cash flows (rents) over a very long period.

As a burgeoning middle class develops in China and Southeast Asia and their service economy picks up, it will present long-term growth opportunities in many areas, especially e-commerce.

Let me remind you in public markets, CPPIB made a huge windfall off the Alibaba IPO a few years ago but that decision didn’t happen overnight. It took years and boots on the ground to nurture that investment.

The article above quotes CPPIB’s CEO Mark Machin as stating: “China’s been very thoughtful about creating the ingredients of innovation, which is creating more opportunities for all types of companies, whether it’s e-commerce or others, to bloom.”

I will trust Mark’s judgment on this but my own personal money is all invested in US stocks and I think it will only be invested in US stocks for the rest of my life, especially if the new Canadian federal budget announces higher taxes on capital gains and dividends. In my opinion, there is no other country that competes with the US when it comes to real innovation.

And let’s not forget, China is a communist country experimenting with “controlled capitalism”. This means capital isn’t allocated efficiently across various sectors and there is way too much government interference at all levels of the economy.

What the Chinese have managed to do is create a massive overinvestment bubble which threatens economic growth there. In fact, the OECD recently warned that China should urgently address rising levels of corporate debt to contain financial risks as it tries rebalance the nation’s economy:

Beijing should also step up efforts to retire “zombie” state firms in ailing industries to help channel funds to more efficient sectors and enhance the contribution of innovation in the economy, the organisation said its latest survey of China’s economy.

“Orderly rebalancing requires addressing corporate over-leveraging, overcapacity in real estate and heavy industries and debt-financed overinvestment in asset markets,” the report said.

It forecast China’s economy would grow 6.5 per cent this year and 6.3 per cent in 2018.The report warned of mounting financial risks as enterprises are heavily indebted, while housing prices have become “bubbly”.

Corporate debt is estimated at 175 per cent of GDP, among the highest in emerging economies, climbing from under 100 per cent of GDP at the end of 2008, the report said.“Soaring property prices in the largest cities and leveraged investment in asset markets magnify vulnerability and the risk of disorderly defaults,” it said. “Excessive leverage and mounting debt in the corporate sector compound financial stability problems, even though a number of tax cuts are being implemented to reduce the burden on enterprises.

Alvaro Santos Pereira, director of the country studies division at the OECD’s economics department, said at a briefing on the report: “Although the risks are rising, the firepower in the Chinese government is big enough and if there’s a problem, it’s able to sort it out.”

The report called for better and more timely fiscal data releases and to expand funding in health and education. Monetary policy should rely more on market-oriented tools and less on targeted government policy, it said.

China is trying to boost the services sector and encourage greater innovation in the economy, partly through promoting greater entrepreneurship and the commercial use of the internet.

Official data shows more than 100,000 new firms were registered each day last year in China, but the report said there were too many unviable firms and the progress on scrapping zombie state-run companies was modest.

It cited a research report published last year saying that nearly half of steel mills and half of developers were making losses, but could still obtain loans. Zombie companies, mainly state-owned enterprises in industries plagued by excess capacity, have aggravated credit misallocation and dragged down productivity, the report said.

The State-owned Asset Supervision and Administration Commission said last year it aimed to close 345 zombie firms in the coming three years. The report said the number was “rather modest” given that the commission controls about 40,000 companies.

It added that the government should remove implicit guarantees to state firms as a way to stop corporate debt from piling up and that bankruptcy laws should be improved to help phase out zombie state firms.

China is increasing spending on research and development, but innovation does not significantly contribute to growth, the report said. Despite the soaring number of patents, “only a small share are genuine inventions”. The utilisation rate of university patents is only about five per cent compared to 27 per cent in Japan.

“Only a fraction of Chinese patents are registered in the United States, the European Union and Japan and Chinese researchers are weakly linked to global networks,” the report said. Margit Molnar, chief China economist and lead author of the report, added: “The internet should be faster and cheaper.”

The report suggested government support for innovation should extend to more sectors rather than strategically important projects and high-tech industries.

The OECD has 35 member countries, with China a strategic partner.

The organisation has a stringent set of criteria for membership based on data transparency and other factors including oil reserve levels.

The attraction of membership for China has waned as it favours involvement with other international organisations, including the International Money Fund and the G20 group of industrialised nations.

“The OECD is no longer a rich men’s club. It is important the OECD is becoming more and more global because the world has been changing dramatically over the past years,” said Pereira. “China is looking at the OECD, hopefully, with increasing interest.”

He added the organisation had close cooperation with the Chinese authorities. “We welcome that,” he said.

As you can see, even though China is still “officially” growing at a 6.5% clip, most of this growth is increasingly financed by debt to support thousands of zombie companies that should be shut down.

Also, innovation in China is not a meaningful contributor to economic growth because the Chinese don’t excel in innovation and have very few patents on any genuine inventions.

Having said this, China has managed its growth admirably thus far and we can debate whether a country like China can thrive on laissez-faire American capitalism (I personally don’t think so, not that there has been much laissez-faire capitalism going on in the US either).

In my last comment on the $3 trillion shift in investing, I stated the following:

Given my views on the reflation chimera and the risks of a US dollar crisis developing this year, I would be actively shorting emerging markets (EEM), Chinese (FXI), Industrials (XLI), Metal & Mining (XME), Energy (XLE) and Financial (XLF) shares on any strength here (book your profits while you still can). The only sector I trade now, and it’s very volatile, is biotech (XBI) but technology (XLK) is also doing well, for now.

I still maintain that if you want to sleep well, buy US long bonds (TLT) and thank me later this year. In this deflationary environment, bonds remain the ultimate diversifier.

Now, this morning I read that Asian shares are at 21-month highs and the US dollar is soft on Fed views which are less hawkish than previously anticipated.

Great, so am I wrong on my macro call? Nope, I am rarely wrong on my macro calls but the story I’m describing won’t hit us till the second half of the year and perhaps even in the last quarter of the year.

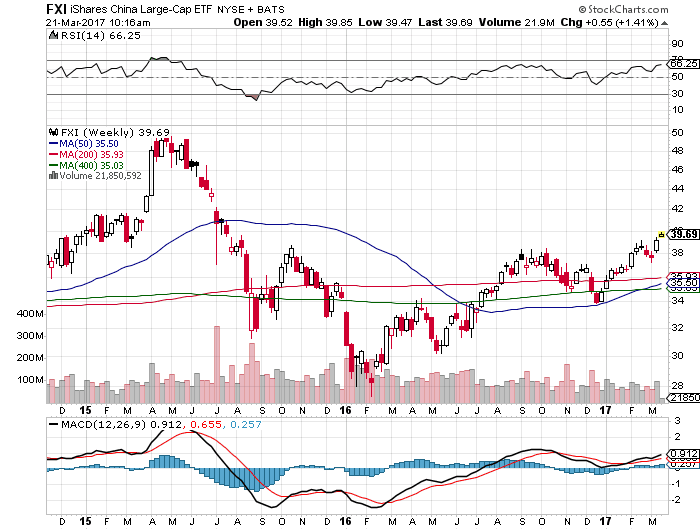

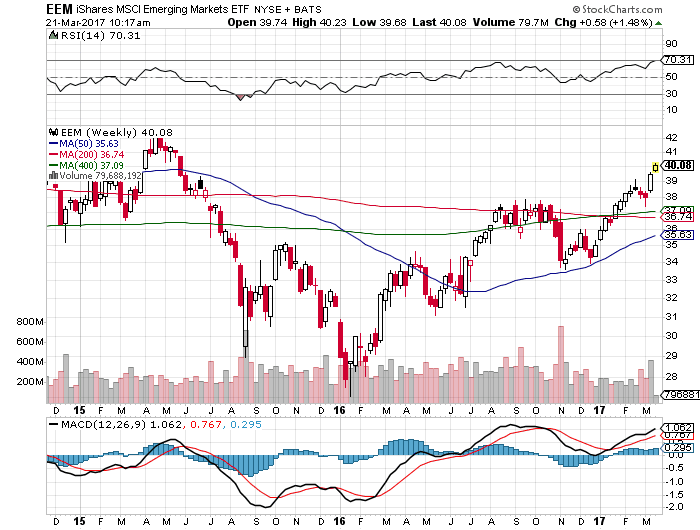

Yes, Chinese (FXI) shares have been breaking out on the weekly chart, propelling emerging market (EEM) shares higher too (click on images):

These are bullish weekly breakouts that augur well for these shares in the short run, but given my global deflation view, I wouldn’t be investing here and I’m pretty sure once global leading indicators start heading south, these markets are in big trouble (keep shorting them on any strength).

What does this have to do with CPPIB raising its stakes in China over the long term? Nothing except I would be more like PSP and remain very cautious on emerging markets including China over the near term. If there is a massive downturn in China, then reevaluate and go in and raise your stakes.

Having said this, I realize that CPPIB is a super long term investor and doesn’t need to perfectly time its entry in public and private markets, but all this bullishness on China at this particular time makes me very nervous.

Still, CPPIB is helping China fix its pension future (they need all the help they can get) and it has developed solid relationships there, including high level government relationships it can leverage off of to make smart investments over the long run.

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712