Last week, Pension360 covered a question asked by the Washington Post’s Wonkblog:

Does it make sense for local governments to turn over the assets of their employee pension plans to insurance companies, who would in turn make monthly payments to retirees?

This week, Mary Pat Campbell (who runs the STUMP blog) has given an in-depth answer to the above question:

Here is the problem: for all of my posts about alternative assets in public pensions (though those are troubling when they are a huge portion of the portfolio), it’s not the financial risks per se, or even the longevity risk, that has been killing public pensions, though those do contribute.

It’s that governments are great at promising, but not so great at putting money by to pay for those promises.

[…]

Insurers are willing to write group annuities to back pension promises — they did this with GM and Verizon pensions — but you have to give them all the assets they require to back that business. A “fair price” would be less than what is statutorily required, probably, because statutory requirements tend to be very conservative in valuing the liabilities, in order to protect policyholders/annuitants. This is called surplus strain.

But the thing is, even with the “fair price”, governments would have to pay amounts way beyond what they’re paying now, just to meet the pension promises made for past service, forget about any future service accruals.

The main problem is that not enough money has been put by. The risk is not so much that public pensions across the country have been investing too riskily or anything like that (but overly risky investing can make the bad situation worse.)

Now, not all pensions are underfunded as grossly as New Jersey or Illinois. But you don’t get to a 72% overall funded ratio just from those two states.

While insurers might be able to reduce the worry about longevity risk and financial risk for fully-funded plans, they cannot help politicians trying to lowball pension costs.

Her answer, in other words: “No”.

Photo by www.stockmonkeys.com

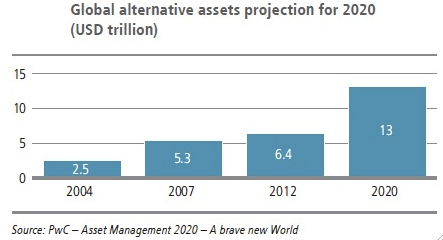

Chart credit: Chief Investment Officer and PwC

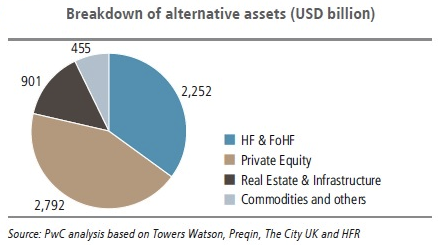

Chart credit: Chief Investment Officer and PwC