Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; Translation_Entry has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/entry.php on line 14

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_Reader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 12

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_FileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 120

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_StringReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 175

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 221

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedIntFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 236

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; WP_Widget_Factory has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/widgets.php on line 544

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/load.php on line 585

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712 investment returns | Pension360 | Page 2 Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

The Canada Pension Plan Investment Board (CPPIB) has had to absorb some criticism lately, stemming from its recent purchase of a large tract of Saskatchewan farmland.

CPPIB bought 115,000 acres of Saskatchewan farmland in 2013; but the fund is now coming under fire for artificially inflating land values, among other things. Some observers are worried that there is a disconnect between what is best for the land and what is best for CPPIB’s bottom line.

CPPIB has the ability to spend money on improvements to the farms, and to own the land for decades. During that time many emerging countries will see rapid increases in population and wealth, increasing the demand for food. Saskatchewan has the potential to be a big beneficiary of this global trend.

We spent a long time studying farming dynamics before we bought this land. And we’re proud to own it.

[…]

For a long time now roughly 40 per cent of Saskatchewan’s farmland has been rented, rather than owned, by the farmers who farm it.

Within about six months of owning the land we ensured that 18 abandoned buildings were demolished, seven old storage and fuel tanks were removed, and three yard sites were cleared up.

In addition, two ponds that were being used to dump waste were cleaned out. An abandoned water well was capped. We are working on improvements to irrigation, storage and drainage.

We want to partner with local farmers to improve production techniques – and the livelihoods of those working in the sector.

[…]

CPPIB is a patient, responsible, long-term investor. We do not plan to amass huge individual holdings of farmland, or to squeeze out returns. We will make reasonable investments to improve farms and help those farmers who choose to partner with us to compete.

Photo credit: “Canada blank map” by Lokal_Profil image cut to remove USA by Paul Robinson – Vector map BlankMap-USA-states-Canada-provinces.svg.Modified by Lokal_Profil. Licensed under CC BY-SA 2.5 via Wikimedia Commons – http://commons.wikimedia.org/wiki/File:Canada_blank_map.svg#mediaviewer/File:Canada_blank_map.svg

The New Orleans Municipal Employees Retirement System returned less than 5 percent in 2014, a number that is pushing some board members – including the city’s finance director – to consider a more passive investment strategy.

Trustee and city finance director Norman Foster argued this week that the fund should be investing in funds that passively follow indices like the S&P 500, which saw double digit returns in 2014.

Several board members expressed some frustration with the fund’s investment performance, none more than Norman Foster, the city’s finance director.

Foster argued that the city would have been better served by investing in index funds, passive investment vehicles that track the market and eliminate costly management fees. “I’ve made the case for passive investment, and I’ll be making it more and more,” he said.

[…]

Some of the performance lag can be attributed to the fund’s asset mix. Like many pension systems, the retirement system invests heavily in bonds, a strategy that minimizes risk but also limits returns during market booms.

Foster pointed out, however, that even when the asset mix is taken into account, the fund’s performance fell short of index benchmarks by nearly 3 percent, which means the managers failed to beat the market, despite collecting handsome fees.

Ian Jones, who advises the retirement system on investment issues, warned against dumping its asset managers based on one year’s worth of data.

The fund assumes a 7.5 percent annual return.

Over the past seven years, the fund’s returns have averaged 4.21 percent annually.

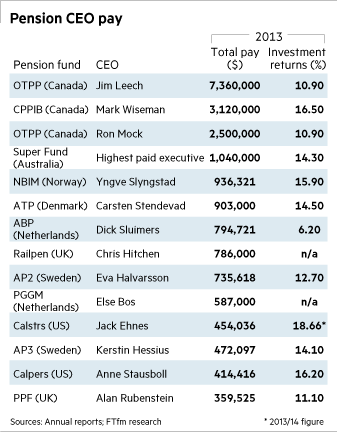

This week, the Financial Times released a list of the highest-paid pension CEOs, and interviewed observers from several corners who criticized the high compensation totals.

On Wednesday, Leo Kolivakis of Pension Pulse weighed in on pension executive pay in an extensive piece. The post is re-printed below.

It’s about time the media and non-profit organizations start scrutinizing executive pay at public pension funds. I’ve been covering the good, the bad and downright ugly on executive compensation at Canada’s large public pension funds since the inception of this blog back in June 2008.

If compensation is tied to performance and benchmarks, doesn’t the public have a right to know whether or not the benchmarks used to evaluate this performance accurately reflect the risks taken by the investment manager(s)?

The dirtiest secret in the pension fund world is that benchmarks used to reference the performance of private investments and hedge fund activities in public pension funds are grossly underestimating the risks taken by the managers to achieve their returns. Moreover, most of the “alpha” from these investment activities is just “beta” of the underlying asset class. Why are pension executives being compensated for what is essentially beta?!?!?

There is a disconnect between public market benchmarks and private market benchmarks. Most pension funds use well known public market benchmarks like the S&P 500 to evaluate the performance of their internal and external managers. Public market benchmarks are well known and for the most part, they accurately reflect the risks that investment managers are taking (the worst example was the ABCP fallout at the Caisse which the media keeps covering up).

But there are no standard private market benchmarks; these investments are illiquid and valued on a quarterly basis with lags. This leads to some serious issues. In particular, if the underlying benchmark does not reflect the risk of private market investments, a pension fund can wipe out its entire risk budget if real estate or private equity gets hit hard in any given year, which is not hard to fathom in the current environment.

I followed up that first blog comment with my second comment on alternative investments and bogus benchmarks where I used the returns and benchmarks of real estate investments at a few of Canada’s large public pension funds to demonstrate how some were gaming their benchmarks to claim “significant outperformance and value-added” in order to justify their multimillion compensation packages even as their funds lost billions during the crisis.

In April 2009, I went to Parliament Hill where I was invited to speak at the Standing Committee on Finance on matters relating to pensions (after that hearing, I was even confronted by Claude Lamoureux, the former CEO at Ontario Teachers largely credited for starting this trend to pay top dollars to senior pension fund managers, which then spread elsewhere). There, I discussed abuses on benchmarks and how pension fund managers routinely game private market benchmarks to create “value-added” in their overall results to justify some seriously hefty payouts for their senior executives.

This brings me to the list above (click on image at the top). Where is Gordon Fyfe, the man who you can all indirectly credit for this blog? He should be right up there at the top of this list. He left PSP for bcIMC this past summer right on time to evade getting grilled on why PSP skirted foreign taxes, embarrassing the federal government.

In fact, over the ten years at the helm of PSP Investments, a federal Crown corporation that is in charge of managing the pensions of people on the federal government’s payroll, Gordon Fyfe and his senior executives literally made off like bandits, especially in the last few years. This is why I poked fun at them when I covered PSP’s FY 2014 results but was dead serious when I wrote this:

And why are benchmarks important? Because they determine compensation. Last year, there was an uproar over the hefty payouts for PSP’s senior executives. And this year isn’t much different.

As you can see, PSP’s senior executives all saw a reduction in total compensation (new rules were put in place to curb excessive comp) but they still made off like bandits, collecting millions in total compensation. Once again, Mr. Fyfe made the most, $4.2 million in FY 2014 and a whopping total of close to $13 million over the last three fiscal years.

This type of excessive compensation for public pension fund managers beating their bogus private market benchmarks over a four-year rolling return period really makes my blood boil. Where is the Treasury Board and Auditor General of Canada when it comes to curbing such blatant abuses? (As explained here, the Auditor General of Canada rubber stamps financial audits but has failed to do an in-depth performance audit of PSP).

And don’t think that PSP’s employees are all getting paid big bucks. The lion’s share of the short-term incentive plan (STIP) and long-term incentive plan (LTIP) was paid out to five senior executives but other employees did participate.

But enough ranting about PSP’s tricky balancing act, I’ve covered that topic ad nauseum and think the Auditor General of Canada really dropped the ball in its 2011 Special Examination which was nothing more than a sham, basically rubber stamping the findings of PSP’s financial auditor, Deloitte.

Nothing is more contentious than CEO pay at public sector organizations. The Vancouver Sun just published an article listing the top salaries of public sector executives where it states:

Topping this year’s salary ranking is former bcIMC CEO Doug Pearce, with total remuneration of $1.5 million in 2013, the most recent year for which data is available. That’s a 24-per-cent jump from his pay the year before of $1.2 million.

It could be the last No. 1 ranking for Pearce, who has topped The Sun’s salary ranking several times: he retired in the summer of 2014 and was replaced by Gordon Fyfe.

Wait till the socialist press in British Columbia see Fyfe’s remuneration, that will really rattle them!

It’s worth noting however even in Canada, compensation of senior public pension fund managers varies considerably. On one end of the spectrum, you have Jim Leech and Gordon Fyfe, and on the other end you have Leo de Bever, Michael Sabia and Doug Pearce, Fyfe’s predecessor at bcIMC (Ron Mock currently lies in the middle but his compensation will rise significantly to reflect his new role).

Mark Wiseman and André Bourbonnais, PSP’s new CEO, actually fall in the upper average of this wide spectrum but there’s no doubt, they also enjoyed hefty payouts in FY 2014 (notice however, Wiseman and Bourbonnais made the same amount, which shows you their compensation system is much flatter than the one at PSP’s).

Still, teachers, police officers, firemen, civil servants, soldiers, nurses, all making extremely modest incomes and suffering from budget cuts and austerity, will look at these hefty payouts and rightfully wonder why are senior public pension fund managers managing their retirement being compensated like some of Canada’s top private sector CEOs and making more than their private sector counterparts working at mutual funds and banks?

And therein lies the sticking point. The senior executives at Ontario Teachers, CPPIB, PSP, bcIMC, AIMCo, OMERS, Caisse are all managing assets of public sector workers that have no choice on who manages their assets. These public sector employees are all captive clients of these large pensions. I’m not sure about the nurses and healthcare workers at HOOPP but that is a private pension plan (never understood why it is private and not public but the compensation of HOOPP’s senior executives is in line with that at other large Canadian pension funds, albeit not as high even if along with Teachers, it’s arguably the best pension plan in Canada).

Of course, all this negative press on payouts at public pension funds can also be a huge distraction and potentially disastrous. Importantly, Canada’s large public pension funds are among the best in the world precisely because unlike the United States and elsewhere, they got the governance and compensation right, operating at arms-length from the government and paying people properly to deliver outstanding results in public and private markets.

And let’s be clear on something, the brutal truth on defined-contribution plans is they simply can’t compete with Canada’s large defined-benefit pensions and will never be able to match their results because they’re not investing across public and private markets, they don’t have the scale to significantly lower costs and don’t enjoy a very long investment horizon. Also, Canada’s large pensions invest directly in public and private assets and many of them also invest and co-invest with the very best private equity, real estate funds and hedge funds.

In other words, it’s not easy comparing public pension fund payouts to their private sector counterparts because the skills required to manage private investments are different than those required to manage public investments.

I’ll share something else with you. I remember having a conversation with Mark Wiseman when I last visited CPPIB and he told me flat out that he knows he’s being compensated extremely well. He also told me even though he will never be able to attract top talent away from private equity funds, CPPIB’s large pool of capital (due to captive clients), long investment horizon and competitive compensation is why he’s able to attract top talent from places like Goldman Sachs.

In fact, Bourbonnais’s successor at CPPIB, Mark Jenkins, is a Goldman alumni but let’s be clear, most people are still dying to work at Goldman where compensation is significantly higher than at any other place.

But we need to be very careful when discussing compensation at Canada’s large pensions. The shift toward private assets which everyone is doing — mostly because they want to shift away from volatile public markets and unlock hidden value in private investments using their long investment horizon, and partly because they can game their private market benchmarks more easily — requires a different skill set and you have to pay up for that skill set in order to deliver outstanding long-term results.

Also, as I noted above, Canadian pensions invest a significant portion of their assets internally. This last point was underscored in an email Jim Keohane, CEO of HOOPP, sent me regarding the FT article above where he notes (added emphasis is mine):

You have to be careful with this type of simple comparison of Canadian pension plans with their US, European and Australian counterparts. It is a bit like comparing apples to oranges because the Canadian pension funds operate very different business models. The large Canadian funds use in house management teams to manage the vast majority of their assets, whereas most of these foreign funds mentioned outsource all or a significant portion of their assets to third party money managers. They are paying significantly larger amounts to these third party managers to run their money as compared to the amounts that Canadian pension funds pay their internal staff. As a result, their total implementation costs are significantly higher than Canadian funds. The right metric to compare is total implementation costs, and on this metric, Canadian funds are among the most efficient in the world.

We have very low implementation costs, with investment costs of approximately 20bps and total operating costs including the admin side between 30 and 35bps. We hire top investment managers to run our money and need to pay market competitive compensation to attract and retain them. I would agree that our long term nature and captive capital make us an attractive place to work so we don’t have to be the highest payer to attract talent, but we need to be in the ballpark. Running our money internally is significantly cheaper than the outsourcing alternative. It also allows you to pursue strategies that would be very difficult to pursue via an outsourcing solution, and it enables much more effective risk management.

One of the main reasons why Canadian pension plans have been successful is the independent governance structures that have been put in place. This enables funds like HOOPP to be run like a business in the best interest of the plan members. It is in the members best interest to implement the plan at the lowest possible cost. The cheapest way for us to run the fund is using an in-house staff paying them competitive compensation rather than outsource which would be much more costly. To put this in perspective, a few years ago we had 15% of our fund outsourced to third party money managers, and that 15% cost more to run than the other 85%!

Many of the international funds used for comparison in the article have poor governance structures fraught with political interference *which makes it politically unpalatable to write large cheques to in-house managers, so instead they write much larger cheques to outside managers because it gets masked as paying for a service. This is not in plan members best interests.

I agree with all the points Jim Keohane raises in regard to the pitfalls of making international comparisons.

But does this mean we shouldn’t scrutinize compensation at Canada’s large public pensions? Absolutely not. A few weeks ago when I discussed whether pensions are systemically important with Jim, I said we don’t need to regulate them with some omnipotent regulator but we definitely need to continuously improve pension governance:

… I brought up the point that in the past, Canadian public pensions have made unwise investment decisions, and some of them could have exacerbated the financial crisis. The ABCP crisis had a somewhat happy ending but only because the Bank of Canada got involved and forced players to negotiate a deal, averting a systemic crisis. And we still don’t know everything that led to this crisis because the media in Quebec and elsewhere are covering it up.

I also told him we need to introduce uniform comprehensive performance, operational and risk audits at all of Canada’s major pensions and these audits need to be conducted by independent and qualified third parties that are properly staffed to conduct them. I blasted the Auditor General of Canada for its flimsy audit of PSP Investments, but the truth is we need better, more comprehensive audits across the board and the findings should be made public.

Another thing I mentioned was maybe we don’t need any central securities regulator. All we need is for the Bank of Canada to have a lot more transparency on all investment activities at all of Canada’s public and private pensions. The Bank of Canada already has information on public investments but it needs more input, especially on less liquid public and private investments.

This is where I stand. I think it’s up to Canada’s large public (and private) pension funds to really make a serious effort in explaining their benchmarks, the risks they take, the value-added and how it determines their compensation in the clearest, most transparent terms but I also think we need independent overview of their investment and operational activities above and beyond what their financial auditors and public auditors currently provide us.

Importantly, there’s a huge gap that needs to be filled to significantly improve the governance at Canada’s large pensions, even if they are widely recognized as having world-class governance.

Finally, I remind all of you that it takes a lot of time and effort to share these insights. I’ve paid a heavy price for being so outspoken but I’m proud of my contributions and rest assured, while we can debate compensation at Canada’s large pensions, there’s no denying I’m THE most underpaid, under-appreciated senior pension analyst in the world!

Legislation is moving forward that would let the Kentucky Teachers Retirement System (KTRS) issue $3.3 billion in bonds to help ease the system’s funding shortfall.

On Tuesday, the bill cleared Kentucky’s House Budget Committee without any opposition.

The bill’s sponsor, House Speaker Greg Stumbo, said a House vote could be coming as soon as next week.

If passed, the plan’s success hinges on KTRS investment returns exceeding the interest on the issued bonds.

Without a clear plan to ante up more money, lawmakers on the powerful House Budget Committee are backing legislation that would let KTRS issue $3.3 billion in bonds to prop up its investments over the next eight years.

[…]

If approved, KTRS would issue the bonds in fiscal year 2016. Pension officials estimate that they can borrow money at 4.5 percent interest and earn returns of 7.5 percent through investments. The plan also calls on the state to begin gradually increasing contributions in the next budget cycle.

All together, that would cut the state’s annual retirement contribution in half — from more than $800 million each year to about $400 million a year — by 2026.

KTRS says it can cover the costs by reshuffling finances for certain benefits and by reappropriating debt service that’s already in the state budget and slated to retire.

Stumbo says he traditionally opposes pension bonds but argued Tuesday that the state could capitalize on interest rates, which have dropped to 50-year lows. “That makes this window of opportunity that we have so attractive,” he said.

When Illinois Governor Bruce Rauner was on the campaign trail, he touted his preferred solution to the state’s pension problems: shifting new hires into a system that more resembled a 401(k) plan than a traditional pension.

The idea is commonplace and has been incorporated into dozens of state and local pension plans across the country.

Michael T. Carrigan, president of the Illinois AFL-CIO, has penned a piece lambasting the idea that 401(k)s should replace traditional pensions.

It’s not just basic finance, it’s common sense: A large pool of money invested by professionals will yield far greater returns than small, separate accounts managed by individuals with no professional training in finance.

So why do some think that ending Illinois’ defined benefit pension system and moving workers into privatized, 401(k)-style accounts is a good idea?

[…]

New data from the National Institute for Retirement Security shows just how much Illinois taxpayers stand to lose if we switch to privatized accounts. To provide workers with the same modest retirement benefits, traditional pensions are 48 percent less expensive than 401(k)-style plans. That’s a 48 percent savings to Illinois taxpayers.

According to NIRS, there are a few key reasons why defined benefit pensions are more cost effective:

– Pension plans enjoy higher investment returns and lower fees than individual accounts, generating a 27 percent cost savings.

– Unlike individual investors who generally enjoy high-risk, high-reward investment strategies when they’re young but switch to lower-risk portfolios that yield far lower returns as they age, pension plans can maintain a balanced portfolio that yields consistently high returns, generating an 11 percent cost savings.

– Pension plans pool longevity risk, meaning that they only have to save for the average life expectancy of a group of individuals. Workers in a 401(k) plan need an investment strategy that provides for the event that they live a longer than average life. Longevity risk pooling generates a 10 percent cost savings.

What’s more, cutting public workers’ retirement security by transitioning them to a 401(k) has its own set of unforeseen costs.

The average Illinois public employee makes a salary that is 13.5 percent less than their similarly educated counterparts in the private sector, trading front-end benefits like salary for back-end benefits like pension payments. With pension benefits gone, the state of Illinois may have to drastically increase public sector salaries or risk losing teachers, police officers, firefighters, and thousands of other critical workers.

U.S. public pension funds saw median returns of 6.76 percent in 2014, according to Wilshire Associates. It marks the sixth consecutive year of positive investment performance for public funds in the U.S.

The country’s corporate pension plans returned 6.92 percent.

U.S. public pensions reported median returns of 6.8 percent last year, the sixth year in a row of gains after the financial crisis, according to Wilshire Associates.

The gains, though, are less than the annual investment returns of 7.5 percent to 8 percent that many state and local governments count on to pay benefits for teachers, police and other employees. In the 10 years through Dec. 31, public pensions had a median return of 6.6 percent.

“A lot of the plans can’t be satisfied with a return of less than 7 percent,” said Bob Waid, a managing director at Santa Monica, California-based Wilshire, adding that a portfolio containing 60 percent U.S. stocks and 40 percent U.S. bonds returned 10 percent. “I’m a huge advocate of diversification, but you have to wonder sometimes when you see that the guy who did 60/40 beat you.”

While the Standard & Poor’s 500 Index of U.S. stocks returned 13.7 percent, public pensions were dragged down by international investments. Stagnation in Europe and a strong dollar led to losses of almost 4 percent on foreign stocks, according to Wilshire.

As Pension360 covered this week, the assets of U.S. public plans also rose to all-time highs.

The average hedge fund has returned 5.1 percent annually over the last 10 years, according to HFR, a hedge fund data firm.

The investment vehicle has even been outperformed by many “balanced” mutual funds. But the flow of clients to hedge funds isn’t slowing down, which begs the question: how do hedge funds keep winning clients when performance is so paltry?

How to explain the paradox of a superhot investment vehicle producing ice-cold returns for clients more smitten than ever?

Part of the reason for the lackluster returns: Hedge funds don’t have the same incentive to hit home runs they once did. They can charge management fees of close to 2% of assets. As the industry swells, many managers can get rich just keeping their funds afloat. A decent performance and no huge loss will do just fine.

The head of one of the world’s largest funds recently told me his challenge is to get his traders to embrace more risk, not less. Hedge-fund traders are more conservative because it’s in their self-interest to be more conservative.

There are similar ways to explain why hedge-fund clients aren’t up in arms. Some see an expensive market and want to be in a vehicle that should do better in a downturn.

But others simply want to keep their jobs. Recommending low-cost balanced mutual funds can be hard to justify if one has a well-paid job at a big pension fund or endowment. Properly allocating money to hedge funds is seen as a bigger challenge. Investing in brand-name hedge funds instead of big stocks once might have put an institutional investor’s career on thin ice. Today, avoiding popular hedge funds to wager on the market is seen as a risky career move.

Kansas Gov. Sam Brownback last month proposed issuing $1.5 billion in bonds to help cover the state’s pension funding shortfall.

The bonds would allow Brownback to go through with another proposal – lowering state payments to the pension system by $39 million in fiscal year 2015-16 and by $92 million in fiscal year 2016-17.

But pension bonds don’t come without risks. Over the weekend, a former New York lieutenant governor called Brownback’s plan “a dreadful idea”. From the Wall Street Journal:

Richard Ravitch, the former New York lieutenant governor who helped save New York from bankruptcy in the 1970s and now sits on the board of The Volcker Alliance, called Kansas’ plan “a dreadful idea.”

“If you cover current obligations by borrowing money, you’re on an unstable course,” said Mr. Ravitch.

There are other criticisms of pension obligation bonds, as well. The states and municipalities that issue them, for example, are frequently in ill-equipped to deal with the fallout if pension investment returns don’t exceed bond interest rates.

The state would make a decades-long bet that pension-fund returns will exceed current interest rates for taxable municipal bonds. Kansas officials said interest rates near historic lows make the bonds an attractive way to help manage retirement obligations.

If examined from the stock market highs at the end of 2007, such deals returned an average of 0.8%, the Center [For Retirement Research] said in a report last year. By 2009, however, most pension bonds were a net drain of -2.6%. Thanks to stock market gains following the recession, however, most of the deals were back in positive territory by 2014, returning an average of 1.5%.

Pension-bond deals made at the end of the market run-up in the 1990s, or right before the crash in 2007, have produced negative returns, the report said. Many of the bonds have a 30-year lifespan, meaning the final results won’t be known for years.

“This should be a tool in a well-functioning governments arsenal,” said Alicia Munnell, the Center’s director. “Unfortunately, those that use them tend to be cash-strapped and desperate.”

Philadelphia’s is the only system in Pennsylvania that ties payment of the extra cash to investment returns, said James McAneny, executive director of the state’s Public Employee Retirement Commission, which monitors local plans.

About two-thirds of plans around the country provide stipends pegged to inflation or predetermined rates, rather than investment performance, according to a survey by the National Association of State Retirement Administrators.

[…]

As soon as April, beneficiaries in the system for a decade may see a bonus, said Francis Bielli, executive director of the board of pensions and retirement. Officials haven’t determined how many people are eligible and may spread payments over two checks, he said. The payouts amount to half the extra investment earnings.

The city last paid the bonus in 2008, distributing $40.5 million, Bielli said. He declined to comment on the effect of the stipends or the oversight board’s recommendations.

As noted above, the bonus checks could come as soon as April.

Photo by c_ambler via Flickr CC License

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712