The New Jersey State Investment Council, the entity that oversees investments for the state’s pension fund, has lately been embroiled in controversy revolving around Council Chairman Robert Grady and allegations of conflicts of interest driving investment decisions.

On Thursday, one member of the Council, Guy Haselmann, defended Grady in a letter to the editor published in the Times of Trenton. The letter reads:

The chairman of the State Investment Council (SIC), Robert Grady, has done an outstanding job conducting the business of the council wisely, ethically, apolitically and with the utmost propriety. Recent criticisms levied against the chairman personally, and against the performance of the SIC and the Division of Investments (DOI) politically, are without merit.

The mission of the SIC, of which I am a member, is to provide policy and governance oversight of the DOI. In other words, the SIC does not make investment decisions or select outside managers; rather, it verifies that procedures and investment parameters are met, with the goal of maximizing return per unit of risk.

Disagreements or complaints regarding the governor’s stance on pension reform are matters completely separate from the management and oversight of the pension’s assets. Public input is always welcome; however, baseless attacks and misinformation disseminated via blogs and other means interfere with the timely and efficient work of the DOI and the SIC, and thus does a disservice to all involved, and especially to the 767,000 beneficiaries of the New Jersey Pension System.

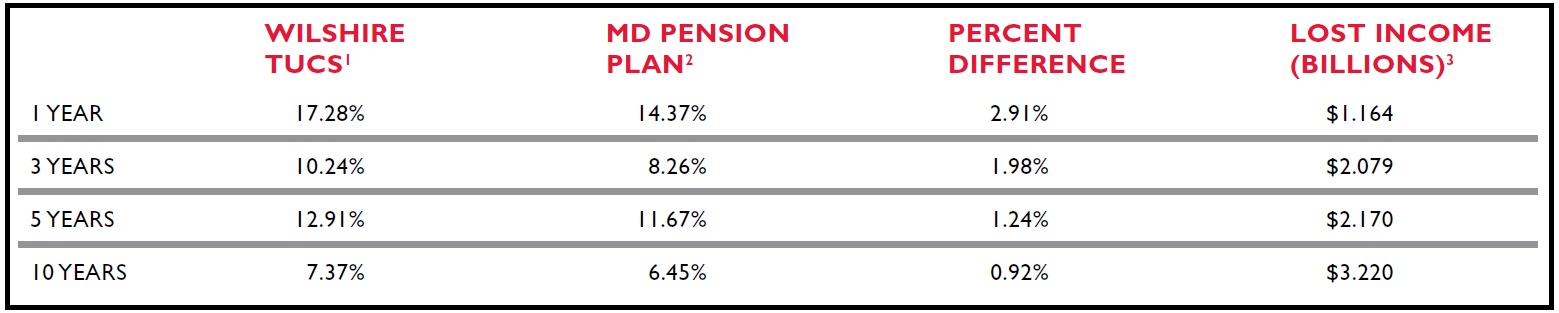

The pension fund returned 16.9 percent in FY 2014, which ends June 30, well above benchmarks and the actuary return assumption. This is testament to the successful oversight and fiduciary duties of the SIC and the DOI.

Pension360 has covered the ethics complaint filed by a union over the alleged conflicts of interest.

Reporting by David Sirota sparked the controversy. His pieces on the topic can be read here.