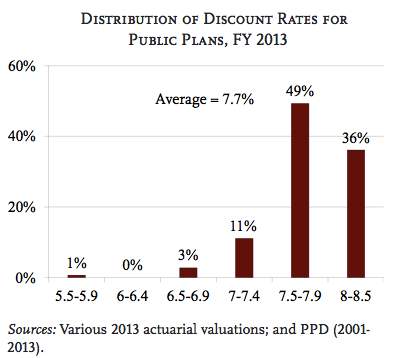

Canada Pension Plan Investment Board (CPPIB) CEO Mark Wiseman told Bloomberg this week that his fund can invest like “an 18-year old” as he looks to cut the fund’s bond allocation and move more money into riskier assets.

CPPIB allocates 28 percent of assets to fixed income. That’s down from 95 percent 15 years ago.

More from the Bloomberg interview:

With years of income and investing ahead, the Canada Pension Plan Investment Board can afford to own more risky assets such as real estate and stocks, according to Chief Executive Officer Mark Wiseman. Pension contributions will continue to grow through 2022, allowing the fund to reduce its 28 percent holdings in fixed income, he said.

“We’re an 18-year-old investor,” Wiseman, who’s 44, said during an interview Tuesday at Bloomberg’s Toronto office. “The portfolio can afford to have less bonds than it has today.”

With yields on fixed-income securities at or close to record lows, Wiseman is joining Canada’s second largest pension plan, the Caisse de Depot et Placement du Quebec, in saying he’s looking to reduce the amount of money invested in debt to seek higher returns elsewhere.

“The low interest environment is a big challenge for institutional investors,” Wiseman said. “We can get higher risk-adjusted returns than we can in the bond market.”

The yield on Canada’s benchmark 10-year bond fell to a record 1.294 percent Friday after government data showed gross domestic product contracted in November. The central bank unexpectedly cut its key interest rate Jan. 21.

CPPIB manages $183 billion in assets.

Photo credit: “Canada blank map” by Lokal_Profil image cut to remove USA by Paul Robinson – Vector map BlankMap-USA-states-Canada-provinces.svg.Modified by Lokal_Profil. Licensed under CC BY-SA 2.5 via Wikimedia Commons – http://commons.wikimedia.org/wiki/File:Canada_blank_map.svg#mediaviewer/File:Canada_blank_map.svg