Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; Translation_Entry has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/entry.php on line 14

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_Reader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 12

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_FileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 120

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_StringReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 175

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 221

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedIntFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 236

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; WP_Widget_Factory has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/widgets.php on line 544

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/load.php on line 585

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712 pension reform | Pension360 | Page 15 Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

State Reps. Seth Grove (R-Dover Township) and Mike Tobash (R-Schuylkill/Berks) hosted a town hall meeting on state pension reform in early August.

But the video has just recently hit YouTube, and it’s worth watching if you’re interested in the various proposals currently sitting in the Pennsylvania legislature.

Tobash is a legislative appointee to the Public Employee Retirement Commission; he is also sponsoring a pension reform bill that would switch new hires into a hybrid-style 401(k) plan.

A recent white paper by Russell Olson and Douglas Phillips, investment officers at the University of Rochester endowment, argues that its time to blow up the 401(k) plan and replace it with a new system—“Trusteed Retirement Funds”.

The researchers say it’s time to simplify the system, noting that over 40 years more than 14 variations of employer-sponsored defined contribution (DC) retirement plans have evolved, including 401(k)s, 403(b)s, SEP IRAs, SIMPLE IRAs, Roths, Keoghs and more.

“Their proliferation has been complex and bewildering. Each has its own deduction or contribution limits, distribution restrictions, and nondiscrimination rules, and there are many variations of each vehicle,” Olson and Phillips write. “Some are available through employers, others not. Some workers have retirement assets in multiple DC plans as they change employers. While the details for each vehicle seemed to make sense when created, the resulting rules and options can be confusing for many workers, and this confusion can lead to insufficient or poorly invested savings.”

“Without radical reform, our nation will have a rapidly growing percentage of impoverished elderly in need of government support,” they say.

Citing the examples of countries with successful retirement strategies, the authors note that Australia, Denmark, Netherlands and Switzerland all mandate high-percentage employee deferrals to savings plans – without offering an “opt-out” choice.

“We don’t believe Americans would agree to the mandating of large pension contributions in addition to what we already contribute to Social Security (through FICA taxes),” the researchers admit. “But we believe we can best meet the challenge by establishing high levels of retirement contributions by employees to Trusteed Retirement Funds, from which employees have the right to opt out. And by adapting the best of Australia’s superannuation concepts, we can sharply improve the effectiveness of our retirement savings.”

More details of the Trusteed Retirement Fund from Main Street:

The “Trusteed Retirement Funds” would have several key features, including:

– Supervision by a fiduciary trustee with strict requirements regarding investment objectives and fees

– Employee contributions would automatically increase by 1% every time an employee received a pay raise, unless the employee directed otherwise

– At retirement, a portion of the assets would be placed into a deferred annuity to provide for guaranteed income later in life, unless the participant declined the option

Employers would have fewer responsibilities under this new system, and participant education would be mandated – and provided by the government, as it is in Australia.

Read the white paper, which was written last June but released this August, here.

The San Diego County Employees Retirement Association (SDCERA) made headlines this summer with its decision to embrace a high-risk investment strategy including extensive use of leverage and derivatives.

But members of the fund’s board expressed concern at a meeting Thursday over potential losses the fund could experience if the risky strategy goes awry. Reported by UT San Diego:

At a contentious meeting Thursday, the pension fund’s board directed managers to fence in potential losses without reducing expected investment returns.

Under a revised investment strategy that took effect July 1, managers can use derivatives to put $20 billion or more at risk in financial markets, using the fund’s $10 billion in assets as collateral.

“Frankly, it scares the heck out of me,” said Dianne Jacob, a county supervisor and appointed member of the pension board, said Thursday.

The fund’s chief investment strategist, Lee Partridge of Salient Partners, said the probability of total losses was exceedingly low. The view was echoed by the fund’s chief executive and a consultant charged with risk management oversight.

Board members approved the new strategy in April, by a unanimous vote that included Jacob.

“The draft IPS does not include appropriate limits and board approval processes in the areas of asset allocation, leverage and portfolio risk monitoring,” said county Treasurer and board member Dan McAllister, in a letter given Thursday to the fund’s chief executive, Brian White.

The point was driven home by Samantha Begovich, a county prosecutor who joined the board in July.

Holding up a dollar bill, then adding a second dollar bill, Begovich asked directly whether the fund could lose its entire balance — and still owe $10 billion.

Fund officials maintained that the probability of a total loss of assets as a result of the strategy was close to zero.

Chris Christie’s lawyers submitted a court filing yesterday urging a judge to dismiss lawsuits from unions alleging that Christie broke the law when he reduced the state’s pension payments earlier this year.

Christie himself signed a law in 2011 mandating that the state make payments into the pension system. But now, Christie’s lawyers have said that the 2011 reform law was unconstitutional to begin with. From the Asbury Park Press:

In a 122-page court filing submitted Tuesday, in response to four lawsuits filed by unions objecting to the reduced $681 million contribution that’s in this year’s budget, Christie’s lawyers argue, in essence, that one of the key concessions the governor made to get Democrats on board with his signature legislative achievement isn’t legal.

Democrats such as Senate President Stephen Sweeney have said the portions of the 2011 pension reforms that made retirement-system contributions a contractual obligation and gave unions the right to sue if they weren’t made were an important provision they wanted in exchange for agreeing to increase workers’ contributions for pensions and health care.

In the court filing, Christie’s administration says three separate sections of the state constitution — the debt limitation clause, the approprations clause and a governor’s veto power — overrule the pension reform’s effort to mandate pension contributions as a contractual right.

The court filing says the final word about appropriations rests with a governor, not lawmakers or judges, unless the state’s voters approve of such a change in a November referendum. As such, the state asks a judge to dismiss the unions’ lawsuits.

“Plaintiffs ask New Jersey to keep a commitment that the state was constitutionally incapable of making. The constitution forbids the Legislature from placing an unwilling populace in an eternal fiscal stranglehold. The Legislature may not incur long-term financial obligations that create an enforceable right to an appropriation without first obtaining permission from the citizenry whose budgetary options, preferences and needs will thereafter be constrained.”

If you knew your pension fund was in great shape, would it alter when you chose to retire? Conversely, if you knew your fund was in dire straits, would it increase the probably of working part-time during retirement?

We present the results of a survey experiment where the treatment group was provided with an information brochure regarding recently implemented changes in the Norwegian pension system, whereas a control group was not. We find that those who received the information are more likely to respond correctly to questions regarding the new pension system. The information effect is larger for those with high education, but only for the most complex aspect of the reform. Despite greater knowledge of the reform in the treatment group, we find no differences between the treatment and control group in their preferences regarding when to retire or whether to combine work and pension uptake.

The Jacksonville City Council unanimously agreed yesterday night to shelve a proposal that could have given the Mayor the power to appoint a member to the city’s Police and Fire Pension Fund board. Reported by the Florida Times-Union:

A wall-to-wall crowd of police and firefighters only had to wait a few minutes Wednesday evening to learn the fate of legislation aimed at giving city leaders the ability to appoint a majority of the Police and Fire Pension Fund board.

In contrast to the debate two weeks ago, the discussion Wednesday night among City Council members only lasted long enough for City Councilman John Crescimbeni to make a motion for withdrawal of his bill.

The council agreed 18-0, resulting in a win for police and firefighters who rallied in opposition to the legislation. Mayor Alvin Brown’s aides also lobbied against the bill, arguing it might unravel a proposed package of pension reforms negotiated by Brown and the Police and Fire Pension Fund.

Crescimbeni’s bill would have scheduled a November referendum for voters to decide whether the mayor should have the power to appoint the fifth member of the Police and Fire Pension Fund board.

Currently, two members of the board are chosen by police and firefighters, two are selected by City Council, and those four members jointly pick the fifth member.

Leaders representing city firefighters applauded the council’s decision But at least part of the reasoning behind shelving the bill had less to do with pension reform and more to do with logistical issues. From the Florida Times-Union:

Randy Wyse, president of the Jacksonville Association of Fire Fighters, said the demise of the bill clears the way for City Council to consider a separate bill containing a host of changes to the police and fire pension system.

“We can move on and get true pension reform,” Wyse said after the vote.

In asking to withdraw the bill, Crescimbeni said there wouldn’t be enough time for election officials to take the procedural steps for placing the referendum on the November ballot.

Duval County Supervisor of Elections Jerry Holland has said the legislation needed to be wrapped up this week.

A handful of council members tried to pass the bill earlier this month, but the council postponed the passage of the bill in a 9-8 vote.

When CalPERS moved last week to implement 99 new types of pensionable compensation, Fitch publicly mused whether the action was a “step backward” from the state’s recent pension reforms.

But the rest of California’s economy, combined with provisions in the most recent budget which increase state funding to CalPERS and CalSTRS, was enough for Fitch to uphold its ‘A’ rating on the state’s GO bonds.

Pension funded ratios have declined and there is a history of inadequate contributions to the teacher system; however, the state has instituted some benefit reforms and the fiscal 2015 enacted budget provides the first installment of a long-term plan to increase funding of the teacher pension system.

Full actuarial contributions to the public employees’ system are legally required, but not for the teachers’ system, leading to persistent underfunding of the latter. The state addressed teachers system funding with legislation enacted in June 2014 that will increase statutorily required contributions to the system from the state, school districts, and teachers beginning in the current fiscal year. The legislation gradually increases funding requirements, with the first installment funded in the fiscal 2015 budget, and expects that it will be fully funded by 2046.

Fitch notes that it doesn’t believe California’s two main pension funds, CalPERS and CalSTRS, are necessarily as healthy as their current funding ratios indicate. Still, a diverse economy and the hope of “improved fiscal management” were among the factors that led Fitch to avoid downgrading the state’s debt.

System-wide funded ratios on a reported basis for the state’s two main pension systems, covering public employees and teachers, have eroded due to investment losses. Based on their June 30, 2013 financial reports, the public employees’ plan reported an 83.1% system-wide funded ratio, and the teachers’ plan reported a 67% system-wide funded ratio.

Using Fitch’s more conservative 7% discount rate assumption, funded ratios for the two systems fall to 78.8% for public employees and 63.5% for teachers. On a combined basis, net tax-supported debt and pension liabilities attributable to the state at 8.3% are above the state median of 6.1%, ranking the state 31st.

The state adopted a broad package of pension reforms in 2012 that affect most state and local systems, including through benefit reductions for new workers and higher contributions for employees. While changes are expected to generate only modest near-term annual savings for the state and for local governments whose pension plans are subject to the reforms, annual savings are expected to grow considerably over time.

Fitch considers California’s GO bond outlook to be “stable”.

Photo credit: “GoldenGateBridge-001″ by Rich Niewiroski Jr. Licensed under Creative Commons Attribution 2.5 via Wikimedia Commons

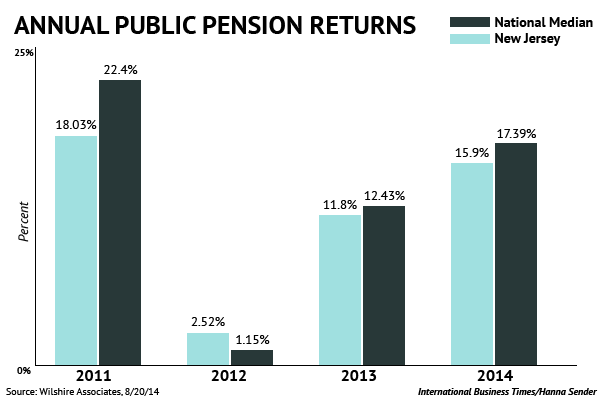

New Jersey is one of the most active states in the country when it comes to investing pension fund assets in hedge funds. That strategy carries risks and boatloads of fees—but it also carries potentially big returns.

Journalist David Sirota investigated the state’s investment decisions and the corresponding return data. He found that New Jersey was certainly straddled with management fees.

Between fiscal year 2011 and 2014, the state’s pension trailed the median returns for similarly sized public pension systems throughout the country, according to data from the financial analysis firm, Wilshire Associates. That below-median performance has cost New Jersey taxpayers billions in unrealized gains and has left the pension system on shaky ground.

Meanwhile, New Jersey is now paying a quarter-billion dollars in additional annual fees to Wall Street firms — many of whose employees have financially supported Republican groups backing Christie’s reelection campaign.

Neither Christie nor the state pension fund’s top investment official responded to Sirota’s requests for comment. But to a certain extent, the numbers speak for themselves. Here’s a chart of the state’s management fees since 2009:

In 2009, the year before Christie took office, New Jersey spent $125.1 million on financial management fees. In 2013, the most recent year for which data is available, the state reported spending $398.7 million on such fees. In all, New Jersey’s pension system has spent $939.8 million on financial fees between fiscal year 2010 and 2013.

That’s only a little less than the amount Christie cut from state education funding in 2010 — a cut that played a major role in shrinking the state’s teaching force by 4,500 teachers. That money might also have reduced the amount the state needs to pay into the pension system to keep it solvent.

That last part, bolded, is important. A major catalyst behind New Jersey’s incoming round of pension reforms was the state’s towering pension payments. Christie decided to divert money from those payments to plug holes in the general budget.

But that decision decreased the health of the state’s pension systems, and Christie now intends to introduce another series of reforms which will likely focus on cuts to benefits.

As you can see, there’s a lot of cause-and-effect reverberating throughout New Jersey’s pension system right now.

A coalition of some of the largest labor groups in Illinois filed a motion today calling on the court to speed up its ruling regarding the constitutionality of Illinois’ pension reform law.

The coalition, We Are One Illinois, says the Supreme Court’s July decision—where the court ruled retirees’ health benefits are protected under the state’s constitution—confirms that Illinois’ pension reform law is illegal.

Yesterday, the We Are One Illinois coalition, along with other plaintiffs, filed a motion in Sangamon County urging the Circuit Court to enter judgment in the plaintiffs’ favor on the State’s affirmative defense in light of the recent Supreme Court decision in the case of Kanerva v. Weems. The We Are One Illinois coalition and other plaintiffs assert that the Kanerva decision confirms that the Pension Protection Clause in the Illinois Constitution is absolute and without exception, even with respect to the fiscal circumstances alleged by the State in its defense.

Illinois says its dire fiscal situation gives it the authority to cut to pension benefits, even if they are constitutionally protected. From Reuters:

The state has contended that its sovereign powers allow it to act in a fiscal emergency. Illinois has a $100 billion unfunded pension liability and the country’s worst funded state retirement system. Illinois’s credit ratings are also the lowest among U.S. states.

But the court’s July decision doesn’t bode well for the state’s case. At the time, the court wrote:

“[I]t is clear that if something qualifies as a benefit of the enforceable contractual relationship resulting from membership in one of the State’s pension or retirement systems, it cannot be diminished or impaired … Giving the language of article XIII, section 5, its plain and ordinary meaning, all of these benefits, including subsidized health care, must be considered to be benefits of membership in a pension or retirement system of the State and, therefore, within that provision’s protections.”

“The Kanerva decision confirms what we have always argued, that the state’s constitutional language guards against any diminishment or impairment of pension benefits that Senate Bill 1 imposes. We believe, then, that the State’s defense is without merit and so have asked the Court in this motion to rule in our favor on the State’s defense that seeks to justify Senate Bill 1. We maintain that the constitution protects the hard-earned and promised retirement savings of our members and remain ready to work with any legislator willing to develop a fair and legal solution to our state’s challenges.”

Photo credit: “Gfp-illinois-springfield-capitol-and-sky” by Yinan Chen, Via Wikimedia Commons

Today CalPERS approved 99 types of “special pay”, or additional income that can be included in calculating a worker’s pension.

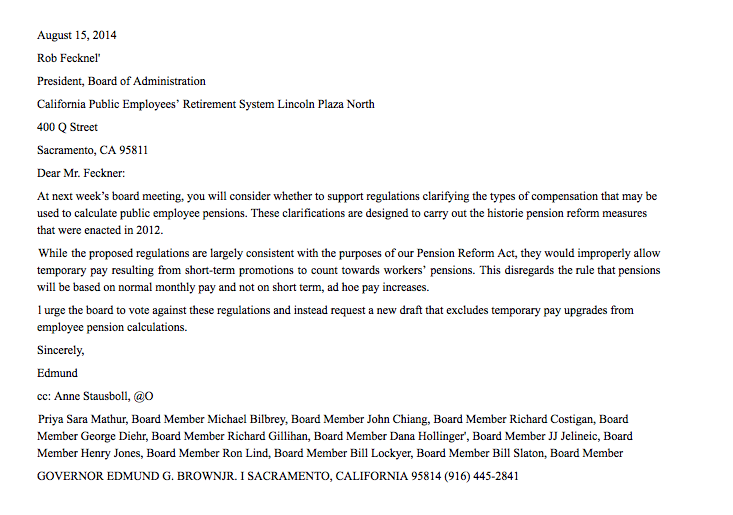

California Governor Jerry Brown was receptive to most of the “special pay” items—except for one. But it was enough to compel him to send a letter to CalPERS urging the board not to approve the pending changes.

At issue is a section of the CalPERS proposal that allows pension benefits to be increased based on temporary pay increases and ad hoc payments.

That contradicts a section of Jerry Brown’s 2012 reform law which states that pension benefits can only be based on “normal monthly pay”, and not “short-term” pay increases. From Reuters:

Although Calpers approved 99 types of extra pay that can be factored in to a worker’s income when calculating their pension, Brown only objected to one of those: allowing temporary upgrade pay to be counted as permanent, pensionable income.

Brown, a Democrat, sent a letter to Calpers last week asking them not to allow temporary upgrade pay to count toward pensions.

On Wednesday, the Calpers board rejected Brown’s opposition and voted to pass all 99 pay provisions, including that temporary pay hikes can be factored into a final pension.

“Today Calpers got it wrong,” Brown said in a statement. “This vote undermines the pension reforms enacted just two years ago. I’ve asked my staff to determine what actions can be taken to protect the integrity of the Public Employees’ Pension Reform Act.”

Read the full letter below, courtesy of the Sacramento Bee:

[A quick PSA, in case you don’t live in California: Edmund is the legal first name of Gov. Jerry Brown.]

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712