In many states, newly hired public employees are faced with a choice: enrollment in a traditional defined-benefit plan, or a 401(k)-style defined-contribution plan.

What drives the decision-making of those who choose DC plans? Scott J. Weisbenner and Jeffrey R. Brown examined the topic in a recent paper in the Journal of Public Economics.

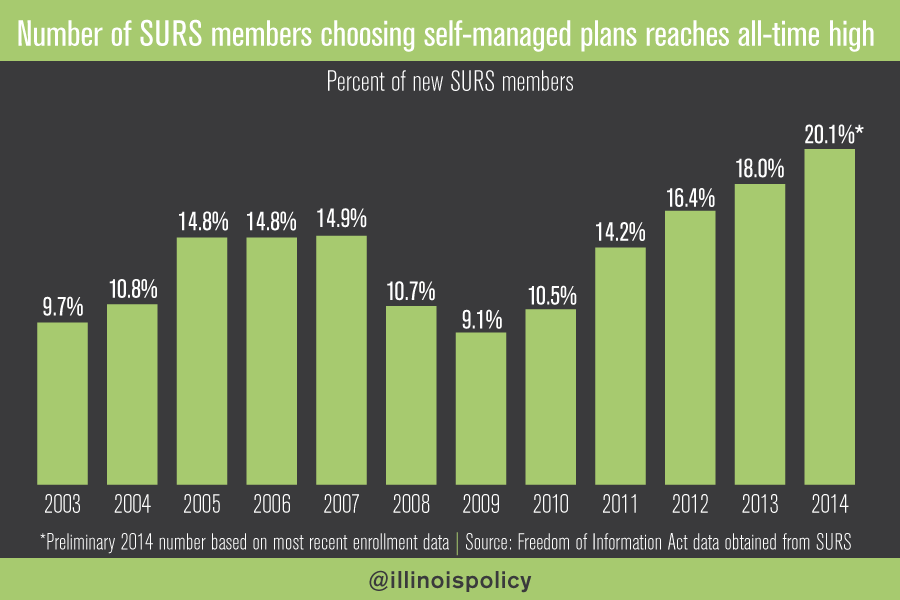

They studied employees in the State Universities Retirement System (SURS) of Illinois, a system that gives every employee a one-time, permanent choice between enrolling in a DB or a DC plan. Here’s what they found about why people might choose DC plans:

First, we find sensible patterns with regard to economic and demographic factors: the probability of choosing the DC plan decreases with the relative financial generosity of the DB plans versus the DC plans and rises with education and income. However, while the relative generosity of the plans does have a nontrivial effect on pension plan choice, it certainly is not a “sufficient statistic” in explaining that choice nor is it the most important determinant in terms of its economic magnitude.

Second, we find that the ability to control for beliefs, preferences, financial skills, and plan knowledge – variables that are not available in standard administrative data sets – increases the amount of variation in plan choice that we are able to explain by approximately seven-fold, relative to using standard economic and demographic variables alone. Specifically, as measured by adjusted R-squared, economic and demographic characteristics such as gender, marital status, presence of children, education, income, net worth, occupation, and (self-reported) health can explain only 6.2% of the overall variation in the DB versus DC plan choice (adjusted R-squared = 0.062). When we expand our regression to include information about beliefs, preferences, financial skills, and plan knowledge, the adjusted R-squared rises to 0.471. Among the important factors in the DB/DC plan choice are respondent attitudes about risk/return trade-offs, financial literacy, beliefs about plan parameters, and attitudes about the importance of various plan attributes.

Third, we note that beliefs about plan parameters are important even when these beliefs are incorrect. In general, people seem to make sensible choices based on what they believe to be true about the plans, but they do not always have accurate beliefs (and thus may not be making optimal decisions). Finally, we provide evidence that preferences over the attributes of the retirement system (e.g., the degree of control provided) are also significant determinants of the DB/DC plan decision.

The paper is titled “Why do individuals choose defined contribution plans? Evidence from participants in a large public plan” and can be read in full here.

Photo by TaxCredits.net

William Mabe, executive director of the State University Retirement System of Illinois (SURS), announced in September that he would be retiring on March 31.

William Mabe, executive director of the State University Retirement System of Illinois (SURS), announced in September that he would be retiring on March 31.