Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; Translation_Entry has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/entry.php on line 14

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_Reader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 12

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_FileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 120

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_StringReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 175

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 221

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedIntFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 236

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; WP_Widget_Factory has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/widgets.php on line 544

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/load.php on line 585

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712 Ted Ballantine | Pension360 | Page 156 Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Here’s full video of a panel discussion that was held on November 14 as part of the 2014 National Lawyers Convention. The discussion was titled “”Intergenerational Equity and Social Security, Medicare, Obamacare, and Pensions”; the panelists discuss the sustainability of Social Security, the pension system, and similar programs.

The panelists:

–Hon. Christopher C. DeMuth, Distinguished Fellow, Hudson Institute, Inc., and former Administrator for Information and Regulatory Affairs, U.S. Office of Management and Budget

–Prof. John O. McGinnis, George C. Dix Professor in Constitutional Law, Northwestern University School of Law

–Prof. David A. Weisbach, Walter J. Blum Professor of Law and Senior Fellow, The Computation Institute of the University of Chicago and Argonne National Laboratory

–Moderator: Hon. Frank H. Easterbrook, U.S. Court of Appeals, Seventh Circuit

Several major federal programs directly tax the young to provide benefits to the elderly. This is a main feature of the Affordable Care Act, the Social Security System as it currently works, and of the laws guaranteeing pensions. In addition, the national debt raises intergenerational equity issues. What obligations do these debts impose on the young? Are they all of a piece or are the answers different in each case? Is it true that this generation is likely to be poorer than the previous one? What role does our legal system play in this? How will the law address pensions that contribute to bankrupting cities or states? What is the nature of the Social Security contract?

The Illinois House passed a measure today that aims to prevent full pension benefits from being paid to public officials who have been convicted of felonies related to their public service.

It passed the House by an overwhelming 99-14 count.

The Illinois House voted Wednesday to give the attorney general the ability to go to court to stop future cases in which a pension is being paid to a convicted public official even if a retirement board had approved payments.

The bill is inspired by disgraced former Chicago police Cmdr. Jon Burge, who did not lose his $4,000-a-month pension despite costing the city tens of millions in legal costs because of police torture and abuse in the 1970s and 1980s. This measure would not affect Burge’s pension.

[…]

After his conviction, the police pension board deadlocked 4-4 on a motion to strip Burge of his pension. The key issue before the board was if Burge’s conviction was related to his police work. Four of the current or former Chicago police officers elected to the pension board by their fellow officers supported Burge, while four civilian trustees appointed by then-Mayor Richard Daley voted in opposition.

Attorney General Lisa Madigan filed suit to challenge the decision, but the Illinois Supreme Court ruled she did not have the standing to take up the matter.

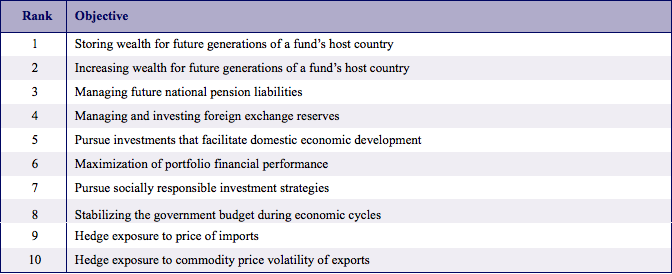

The survey asked respondents to identify and rate the biggest obstacles to cross-border investment:

We first asked respondents to rate, using a five-point Likert- type scale (1 = strongly disagree, 5 = strongly agree), to what extent 20 different issues identified in the investment obstacles literature would “decrease the likelihood your fund will invest in another country.”

[…]

The top two issues, as identified by summing the percentages of “agree” and “strongly agree” responses, were “financial regulation uncertainty” (FP, 80%) and “unfavorable comments by government officials in recipient country” (IC, 73%). While the latter is an IC factor, it focuses on the nation-state and the use of informal suasion by officials, and thus is related to FP factors. Following these items almost two-thirds (64%) of the funds agreed or strongly agreed that “unfavorable tax treatment of your fund type” (FP) and “non-transparent investment review policies” (FP) would reduce the possibility of their fund’s investing in another country. Of these four factors, “financial regulation uncertainty” (FP) and “non-transparent investment review policies” (FP) elicited the highest proportion of “strongly agree” rankings.

The survey also asked respondents to identify the strategies they used to address the barriers:

Respondents were asked to indicate whether or not they used eight specific strategies to address the 20 possible barriers: increase transparency; co-invest; use external managers; restrict voting rights; accept outside investors; use debt; other strategies; and no strategy. Respondents could select all applicable strategies used to address each issue. The strategy identified most often (124 times) to address all three factor classifications was “no strategy,” followed by “external managers” (68) and “increase transparency” (55). Rounding out the top five were “co-investing” (34) and “other strategies” (30). The fact that “other strategies” was selected least often suggests that the survey included the most commonly used strategies.

Finally, the survey asked respondents to rank ten long-term investing objectives. The aggregate results:

The article, authored by Rachel Harvey, Patrick Bolton, Laurence Wilse-Samson, Li An, and Frédéric Samama, can be read in full here.

State agencies and local school boards won’t have to pay as much next fiscal year to cover pension costs for active employees after action Wednesday by a special panel.

All told, the Public Retirement Systems’ Actuarial Committee, called PRSAC, approved a $120 million reduction.

The committee must sign off on financial evaluations of the four statewide retirement systems, which among other things, sets the benchmark for investment earnings as well as required employer contribution rates.

Healthy investment earnings — and to some degree — reductions in work force contributed to the coming budget relief on employers.

State agency contributions to the Louisiana State Employees Retirement System, better known as LASERS, are projected to decline by $62.8 million in the fiscal year that starts July 1, 2015.

Meanwhile, school boards’ contributions to the Teachers Retirement System of Louisiana are anticipated to drop by $46 million and to the Louisiana School Employees Retirement System by $13 million.

The Louisiana State Police Retirement System remains flat.

“This is good news for the state as we begin the budgeting process for the next fiscal year,” Commissioner of Administration Kristy Nichols said in a statement issued by her office. “Saving money here helps free up funding for other areas.”

Louisiana School Boards Association executive director Scott Richard, who attended the meeting, praised the committee action. “The fact that school board contribution rates will go down for 2015-16 is welcome news – at a time when the costs to educate students in Louisiana continues to rise,” Richard said.

“The reduction in costs reverses the trend of recent increases that negatively affected local district budgets,” he added.

The State of Wisconsin Investment Board (SWIB), the entity that manages assets for the state’s retirement systems, has made two separate commitments to real estate totaling $300 million.

The Board committed $150 million to one fund that invests in retail, office, and apartment properties. It also made a second commitment of $150 million to another fund that acquires grocery stores.

State of Wisconsin Investment Board (SWIB) is increasing its investment in the UBS Trumbull Property Fund and has awarded two separate account mandates.

The $150m commitment is the second made by SWIB to the core open-ended fund in the past three years, having made an initial $125m allocation in 2012. The investment was worth $165m in September.

UBS Trumbull, managed by UBS Realty Investors, invests in US office, industrial, retail and apartment sectors.

SWIB said it invests in core real estate for its stable income return with low leverage. The investor is expecting its commitment to be called by the manager in the next 12 months.

SWIB has also commited $150m to a new separate account managed by AmCap and $158m to a separate account managed by Heitman.

In a new relationship for the pension fund, AmCap’s Wilson AmCap I fund will be looking to acquire core grocery-anchored/necessity-oriented US retail.

Jake Bisenius, chief investment officer for AmCap, said its total assets under management are now over $1bn.

The real estate manager has a large concentration of assets in Colorado, buying off-market in cash.

“Most of our purchases are done with cap rates that come in the high-5% to low-6% range,” Bisenius said.

The SWIB manages over $100 billion in assets for the state’s retirement systems and trust funds.

CalSTRS has sold its stake in two buildings in Austin, Texas.

The first, One Congress Plaza, is the 8th tallest building in Austin and a city landmark. The second, San Jacinto Center, is a 21-story office building also located in downtown Austin.

Parkway Properties said it has unwound its joint venture with CalSTRS in Austin, Texas, taking the latter’s 60% interest in San Jacinto Center and One Congress Plaza.

The deal gives Parkway full control of the two properties.

Parkway also said it has transferred its 40% interest in Frost Bank Tower, 300 West 6th Street and One American Center to CalSTRS.

Overall, the deals resulted in net proceeds of around $43.6m (€34.7m).

CalSTRS could invest up to $2bn in global real estate over the next 12 months, as reported earlier this year.

The US investor is planning to deploy between $1bn and $2bn in core and value-added strategies in the US, Latin America, Western Europe and Asia.

During the same period – the 2014-15 fiscal year – CalSTRS will reduce its exposure to opportunistic real estate investments.

CalSTRS manages $22 billion in real estate assets.

Bruce Rauner won the Illinois governorship, in part, by campaigning as a reformer and a political outsider who would “shake up Springfield.”

Rauner targeted the state’s underfunded pension systems as a prime candidate for reform in at least one campaign ad, when he noted that Illinois carries “$8,000 of pension debt for every man, woman and child.”

The governor-elect recently appointed Glenn Poshard to his transition team, which spurred an investigation by the Better Government Association and CBS 2 News.

The investigation found that Poshard “triple dips” – or, pulls in pensions from three separate retirement systems, netting him nearly $200,000 annually in pension benefits. Poshard is breaking no laws, but the situation demonstrates the “loopholes” in the Illinois pension system that can sometimes lead to ballooned benefits.

Andy Shaw, CEO of the Better Government Association, told CBS: “Governor-elect Rauner could probably learn a lot about how to reform the pension system by looking at the ways in which Glenn Poshard used loopholes to enrich his own pension.”

Poshard collects $189,979 a year in state pensions from three separate public-sector retirement systems, more than the $177,412 salary currently paid to Gov. Pat Quinn, the BGA found. Among former governors, only Jim Edgar gets more in retirement: $205,425, having recently picked up a second pension from his days teaching at the University of Illinois. Former Gov. Jim Thompson gets $143,181 in state pension benefits, records show.

In addition to his state-government pensions, Poshard collects a $15,000-a-year federal pension for his 10 years in the U.S. Congress representing a southeastern Illinois district, bringing his total retirement package to slightly more than $200,000 annually, according to records and interviews.

To date, he’s collected more than $1.4 million in state pension benefits, and if he lives until he’s 80, that $200,000 he’s now getting could increase to an estimated $280,000 a year.

[…]

The cornerstone of Poshard’s generous state pension is the five years he served as a state senator. Of all state pension systems, the General Assembly Retirement System, or GARS, has the most deluxe features, designed and passed by members of the General Assembly.

Chief among those features is a formula that allowed him to collect a pension starting at 85 percent of his final state-government salaries – which averaged $165,000 as an SIU administrator during his first of two stints at the state government-run college.

Poshard also was allowed to increase his years of state service and thus boost his state pensions by counting unused sick time, un-served state Senate time, and credits purchased for past jobs in the military and while working his way through college, the BGA found. Overall, Poshard’s state pensions are based on 30 years of service and credit.

“I am very appreciative for the retirement benefits I now receive which were determined by the laws in place at both the state and federal levels. If some of those laws need to be changed in order to more fully fund the pension system, as I myself have advocated before the legislature, then I am more than happy to see a reduction in my own retirement benefits.”

He also gave a phone interview to the Better Government Association:

In a telephone interview, Poshard said he has done nothing unethical and “never tried to game the system.”

“I can tell you, I worked hard my whole life,” said Poshard, 69. “I never shortchanged the state.”

[…]

“I’m grateful for what I got. I’m happy with it. I can’t pass judgment on whether the overall pension was too generous,” said Poshard.

A spokesman for Bruce Rauner said the Poshard’s role on the transition team will not be focused on pension issues.

Robert Grady has resigned from his position as chairman of the New Jersey State Investment Council. He announced his decision during the council’s meeting on Wednesday.

The Council formulates investment polices that govern New Jersey’s Division of Investment, which manages the state’s pension assets.

The rest of the board members collectively commented on Grady’s tenure with the Council, according to ai-cio.com:

“The members of the council acknowledge and appreciate Chairman Grady’s unique blend of outstanding investment and communication skills, which will be deeply missed,” the resolution stated. “We are grateful for his leadership, will miss his warmth and wisdom and good humor, and thank him for his selfless and exemplary service.”

Grady’s tenure was marked by the outperformance of benchmarks – but also controversy. From Chief Investment Officer:

For the four years ending May 30, 2014, the fund has outperformed its policy benchmark by an annualized rate of 1%, generating an additional $3 billion in alpha. New Jersey’s pension returned 17% in the 2014 fiscal year—in line with the median large public plan, according to Wilshire Associates—while taking less risk than 85% of its peers.

[…]

Earlier this year, Grady was the target of criticism from a major New Jersey union, which accused the fund of pay-to-play violations during his and prior chairman’s tenures. The state ethics commission has taken no action on the union’s allegations, which it addressed to the department.

In recent months, campaign finance documents revealed that under Grady’s leadership, the state has awarded lucrative pension management contracts to hedge fund, private equity, venture capital and other so-called “alternative investment” firms whose executives made campaign contributions to Christie’s campaign, his state party, the Christie-led Republican Governors Association and the Republican National Committee. The donations included a $10,000 contribution from Massachusetts Republican Gov.-elect Charlie Baker to the New Jersey Republican State Committee just months before Baker’s firm was given a New Jersey pension investment.

The donations were made despite New Jersey and federal rules aiming to restrict contributions to state officials like Christie who oversee pension investment decisions. Documents uncovered by International Business Times showed that Grady, a former Carlyle Group executive, was in regular communication with Christie’s campaign officials at the time the campaign was raising money and he was overseeing the state’s pension investments. Grady pushed New Jersey to move pension money into an investment in which his private financial firm was also investing, documents revealed. New Jersey also invested in Carlyle Group funds during Grady’s tenure, though he recused himself from final votes on those investments.

Grady has categorically denied the pay-to-play allegations, saying that his position doesn’t give him the power to give pension money to investment firms.

It’s likely that Grady will become a bigger part of Chris Christie’s potential campaign for the presidency.

Paul Singer, a hedge fund manager, activist investor and billionaire, wrote in a recent letter to clients that CalPERS’ exit from hedge funds was “off-base”.

CalPERS said at the time that its decision to exit hedge funds was based on their “complexity, cost and the lack of ability to scale at CalPERS’ size”.

“We are certainly not in a position to be opining on the ‘asset class’ of hedge funds, or on any of the specific funds that were held or rejected by CalPERS, but we think the decision to abandon hedge funds altogether is off-base,” Singer wrote in a recent letter to clients of his $25.4 billion Elliott Management Corp.

[…]

On complexity, Singer wrote that it should be a positive.

“It is precisely complexity that provides the opportunity for certain managers to generate different patterns of returns than those available from securities, markets and styles that are accessible to anyone and everyone,” the letter said.

“We also never understood the discussions framed around full transparency. While nobody wants to invest in a black box, Elliott (and other funds) trade positions that could be harmed by public knowledge of their size, short-term direction or even their identity.”

Singer also slammed CalPERs for its complaint about the relative high cost of hedge funds.

“We at Elliott do not understand manager selection criteria based on the level of fees rather than on the result that investors could reasonably expect after fees and expenses are taken into account,” he wrote.

The broader point Singer makes is on the enduring value of hedge funds to diversify a portfolio.

“Current bond prices seem to create a modest performance comparator for some well-managed hedge funds. Moreover, stocks are priced to be consistent with bond prices, and we have a hard time envisioning double-digit annual stock index gains in the next few years,” the letter said.

“Many hedge funds may have as much trouble in the next few years as institutional investors, but investors should be looking for the prospective survivors of the next rounds of real market turmoil.”

Hedge funds have returned 2.92 percent this year, according to Preqin. Singer’s hedge fund, Elliott Associates LP, has 13.9 percent annually since 1977.

Photo by World Economic Forum via Wikimedia Commons

The Naked Capitalism blog has been given ten private equity limited partnership agreements from “a source authorized to receive them who is not bound by a confidentiality agreement.”

Pension funds sign limited partnership agreements when they do business with private equity firms. Observers are typically very interested in seeing the documents because they are usually kept under lock-and-key, as PE firms claim the documents contain “trade secrets” that would harm business if made public.

The agreements received by Naked Capitalism can be read here.

Here’s an excerpt of the Naked Capitalism post accompanying the release of the documents:

__________________

By Yves Smith

There is a vital public interest in having this information in the open. Public pension funds, which are government bodies, are the biggest single group of investors in private equity, representing roughly 25% of total industry assets. Yet private equity limited partnership agreements are the only contracts at the state and local government level that are systematically shielded from public scrutiny, through state legislation or favorable state attorney opinions.

Yet in countries less captured by rampant free market ideology and private equity political donations, a revolt is underway against this secrecy regime. As the Financial Times reported:

Anger has erupted over the practice of asset managers coercing pension funds into signing non-disclosure agreements. Pension schemes argue it is uncompetitive and prevents them from securing the best deals for their members.

The imposition of confidentiality agreements means pension funds are not able to compare how much they are being charged by fund managers, potentially exposing them and their scheme members to unnecessarily high fees.

The practice is of particular concern with respect to public sector pension plans, which are effectively funded by the taxpayer.

David Blake, director of the Pensions Institute at Cass Business School in London, said: “Local authorities are not allowed to compare fee deals, and that is an outrage. It should be made illegal that fund managers demand an investment mandate is confidential.”

How do private equity kingpins justify their extreme demands for confidentiality, their assertion that limited partnership agreements in their entirety are trade secrets? Consider this “we’ll fight them on the beaches” argument from this Monday’s Private Fund Management, that if general partners, meaning the private equity funds, are forced to divulge fees, they’ll eventually have to expose more of the limited partnership agreement. And of course they claim that would do them competitive harm:

It’s impossible to have a debate about public pension plans disclosing their fee payments without first acknowledging why GPs want them kept private in the first place…

In this context, GPs are being portrayed as secretive and heavy-handed. But so far, what hasn’t been addressed properly is why GPs are apparently so keen to prevent fee receipts from entering the public domain in the first place.

Speaking to pfm off the record, no manager has ever told us that they consider management fees a vital trade secret. No one has defended the idea that disclosing them can make or break a firm.

What we are hearing instead is that GPs perceive the fee debate as a proxy battle for disclosing other data that really are sensitive to the firm’s ability to do business, such as the finer points of their investment strategies, key man clauses and the like. All these things are documented in the LPA, and if the LPA can no longer be subjected to non-disclosure, then sooner or later demands will be made to publish other types of fund-specific information also.