Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; Translation_Entry has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/entry.php on line 14

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_Reader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 12

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_FileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 120

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_StringReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 175

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 221

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedIntFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 236

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; WP_Widget_Factory has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/widgets.php on line 544

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/load.php on line 585

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712 Pension Newsroom | Pension360 | Page 248 Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

The South Carolina Retirement Investment Commission hopes it has found long-term leadership with its newest hire today.

The Commission, which oversees the state’s pension investments, has hired Michael Hitchcock to be its executive director. As reported by the Associated Press:

For the second time in three months, the agency investing South Carolina’s pension portfolio has named an executive director.

The Retirement Systems Investment Commission voted 4-2 on Tuesday to hire Michael Hitchcock, who takes the job Sept. 8. Hitchcock has been the chief attorney and assistant clerk of the South Carolina Senate since 2001. His salary will be $230,000.

Pension360 had previously covered the resignation of Sarah Corbett, who became executive director on June 3 but resigned from the position after two months.

Previous to Corbett, the Commission didn’t have an executive director position. It created the position last Spring.

The Commission manages nearly $30 billion worth of assets

Many people facing retirement ask their financial advisor the same question: is it more advantageous to receive a pension in monthly payments or to take the entire pension as a lump sum to be put in an IRA?

There are big implications attached to either option. And the stakes are high; once you opt for a monthly payment there is no reversing course. As advisor Kevin McKinley writes:

Once the client submits the request to receive the monthly pension payments, there is no turning back. He or she can’t change the time and beneficiary calculation options down the road, and it’s virtually impossible to get an “advance” on future payments.

That could be a problem in several instances, including a need to cover a large emergency expense, the desire to help out a family member, or the emergence of a more attractive investment opportunity.

A big part of the decision to take monthly payments should be how confident you feel in your pension fund’s investment portfolio. A retiree, or his/her financial advisor, might be able to construct an investment portfolio that makes the retiree more comfortable taking the lump sum:

Since the portfolio has to be managed on behalf of thousands of recipients, plus other interested parties, it’s a safe bet that the pension plan’s managers will have to make decisions that may go against what individual clients would like done with their portion of the money.

You can probably tailor a portfolio that is better aligned with the client’s needs and risk tolerance. You certainly can design and manage one that is much more flexible and transparent than if it were left in the pension.

And then there are the tax implications that come with both options, as McKinley writes:

A pension payment is generally going to be fully taxable as ordinary income. But if the funds are instead rolled over into an IRA, the client has several opportunities to reduce his income tax bill each year.

He can take just enough to keep him under a particular federal income tax bracket. Or, he can roll over some (or all) of the account into a Roth IRA, paying the taxes now to hopefully reduce what he pays down the road.

Another option is to take nothing at all and avoid the taxes completely for the time being. The client will likely have to take required minimum distributions after reaching age 70½, but those won’t greatly exceed what a pension payment might otherwise be.

The article notes that, when it comes down to it, retirees need to ask themselves two questions: Are they confident their pension is going to exist as long as they’ll need it?

And, are they confident in their pension fund’s ability to invest and manage their money?

If a retiree lacks confidence in both of those questions, perhaps a lump sum would offer better peace of mind.

When CalPERS moved last week to implement 99 new types of pensionable compensation, Fitch publicly mused whether the action was a “step backward” from the state’s recent pension reforms.

But the rest of California’s economy, combined with provisions in the most recent budget which increase state funding to CalPERS and CalSTRS, was enough for Fitch to uphold its ‘A’ rating on the state’s GO bonds.

Pension funded ratios have declined and there is a history of inadequate contributions to the teacher system; however, the state has instituted some benefit reforms and the fiscal 2015 enacted budget provides the first installment of a long-term plan to increase funding of the teacher pension system.

Full actuarial contributions to the public employees’ system are legally required, but not for the teachers’ system, leading to persistent underfunding of the latter. The state addressed teachers system funding with legislation enacted in June 2014 that will increase statutorily required contributions to the system from the state, school districts, and teachers beginning in the current fiscal year. The legislation gradually increases funding requirements, with the first installment funded in the fiscal 2015 budget, and expects that it will be fully funded by 2046.

Fitch notes that it doesn’t believe California’s two main pension funds, CalPERS and CalSTRS, are necessarily as healthy as their current funding ratios indicate. Still, a diverse economy and the hope of “improved fiscal management” were among the factors that led Fitch to avoid downgrading the state’s debt.

System-wide funded ratios on a reported basis for the state’s two main pension systems, covering public employees and teachers, have eroded due to investment losses. Based on their June 30, 2013 financial reports, the public employees’ plan reported an 83.1% system-wide funded ratio, and the teachers’ plan reported a 67% system-wide funded ratio.

Using Fitch’s more conservative 7% discount rate assumption, funded ratios for the two systems fall to 78.8% for public employees and 63.5% for teachers. On a combined basis, net tax-supported debt and pension liabilities attributable to the state at 8.3% are above the state median of 6.1%, ranking the state 31st.

The state adopted a broad package of pension reforms in 2012 that affect most state and local systems, including through benefit reductions for new workers and higher contributions for employees. While changes are expected to generate only modest near-term annual savings for the state and for local governments whose pension plans are subject to the reforms, annual savings are expected to grow considerably over time.

Fitch considers California’s GO bond outlook to be “stable”.

Photo credit: “GoldenGateBridge-001″ by Rich Niewiroski Jr. Licensed under Creative Commons Attribution 2.5 via Wikimedia Commons

The pension system continues to occupy center stage in Rhode Island’s race for governor. In one corner is current state Treasurer Gina Raimondo, whose 2011 pension reforms were among the boldest in the country and are the subject of numerous lawsuits from labor groups.

In the other corner in Angel Taveras, the current mayor of Providence who has been critical of the pension system’s investments under Raimondo and has accused the Treasurer of being in bed with Wall Street.

Raimondo released a new campaign ad yesterday – you can watch it above – that responded to Taveras’ claims. The Providence Journal reports:

In a new one-minute TV ad released to the media on Monday morning, Raimondo, the state’s general treasurer, looks into the camera and says of her leading rival in the Democratic primary race for governor:

“I’m Gina Raimondo and you might have heard about Mayor Taveras attacking pension reform, claiming I did it to enrich Wall Street. Nothing could be more wrong.”

“I was 11 years old when my dad lost his job at Bulova. I have never forgotten how hard that was. So when I became treasurer and inherited the pension crisis, I knew if we didn’t face up to the problem a lot of people were going to get hurt. And we couldn’t let that happen” she says in the video.

Raimondo, who is being sued by the state’s public-employee unions, next says: “Our reforms passed by overwhelming majorities in the legislature and, in the end, most of our changes were agreed to by every union except one.”

The Taveras campaign has been extremely critical of the hedge funds investments and accompanying investment fees incurred by the state’s pension system under Raimondo’s watch.

A Taveras spokesperson responded to Raimondo’s new ad:

“As a former venture capitalist who raised fees to Wall Street to $70 million, the Treasurer [Raimondo] has taken over $500,000 from the financial industry. The Treasurer received a no bid, secret contract managing taxpayer money that ensured that her venture capital firm was paid whether they made money or not. Rhode Island deserves a governor who has a record of standing up to Wall Street.”

Raimondo has been adamant that most unions were receptive to her reforms. But several union leaders have gone on record to say that is not the case. As the leaders told the Providence Journal:

Leaders of several of the state’s public-employee unions — including Council 94, American Federation of State, County and Municipal Employees — accused Raimondo of misrepresenting their position in the high-stakes pension fight headed for trial next month.

“Council 94, AFSCME vigorously opposed the pension changes. The treasurer’s process was a farce,” said Council 94 President J. Michael Downey, a Taveras backer.

“Our ideas and suggested amendments were ignored. She broke her word about taking care of people with the least amount of pension benefits, in her words: ‘the little guy.’ And she harmed many municipal employees whose pensions were healthy,” Downey said.

Added Paul Reed, president of the Rhode Island State Association of Firefighters: “She never negotiated with us on any of these things.”

The California city Villa Park could vote today to remove itself from the California Public Employees Retirement System (CalPERS).

The decision comes in the face of mounting pension costs and calls for increased transparency in local budgets, which would shine more light on California cities’ unfunded pension liabilities.

The Villa Park City Council could vote Tuesday to end its contract with the California Public Employees’ Retirement System or CalPERS, the world’s sixth largest pension provider, in an effort to reduce increasing pension costs.

The CalPERS move follows an Orange County Grand Jury report that called for greater budget transparency in Orange County cities.

The report indicates Orange County cities’ unfunded pension liabilities have been increasing on an annual basis since 2007.

There have been increased calls for budget transparency in recent years as cities and towns in the CalPERS system have shouldered more liabilities. A recent report called for all cities to put their budgets online and include CalPERS cost projections in all budgets going forward.

Villa Park has millions in unfunded pension liabilities. From Voice of OC:

For its pension costs, Villa Park, a north OC bedroom community of about 5,000, has a shortfall of about $3.5 million, leaving 17.5 percent of its employee pension costs unfunded, according to the grand jury report.

Gov. Jerry Brown enacted sweeping pension reforms in 2012 aimed at reducing pension payments for most public employees hired after 2013.

But because many public workers were hired before 2013, they are grandfathered into the old system, and reforms likely won’t make a dent for another decade, the grand jury report states.

Villa Park could vote on leaving CalPERS as early as 6:30 pm (Pacific Time) Tuesday. The city wouldn’t be the first to leave CalPERS; Canyon Lake, a city of 11,000, left the system in 2013 due to increasing employee contributions.

After years of negotiations, Philadelphia and its largest union have come to an agreement on a new labor contract that has implications for the city’s pension system and the workers that pay into it.

The union, AFSCME District Council 33, indicated that its members will overwhelmingly approve the deal.

A major provision of the deal gives employees a choice between several retirement plan options. Employees will also have to pay more into the pension system. From Business Insurance:

[The deal] will increase employee contributions to the pension fund and allow new employees the choice between a hybrid plan and the traditional pension plan, said Mark McDonald, a spokesman for Mayor Michael A. Nutter.

The contract agreement term is retroactive from July 1, 2009, through June 30, 2016. Terms of the contract must be ratified by members of DC 33.

Current participants in the $4.8 billion Philadelphia Municipal Retirement System, a defined benefit plan, will have their employee contribution increase by 1% of pay over the next two years — 0.5% effective Jan. 1, 2015, and an additional 0.5% effective Jan. 1, 2016.

All employees hired after the contract is ratified can either enter the defined benefit plan and pay 1% more than current participants or enter a hybrid plan. Current employees have 90 days following ratification to make an irrevocable election to move to the hybrid plan.

The newly reached seven year tentative agreement is retroactive from July 2009 and expires in 2016.

The deal will include wage increases of 3.5 percent this year, 2.5 percent next year plus a lump sum of $2,800 for every member. However the wage increases are not retroactive.

Also in the deal – employee contributions to pensions will increase and the city will pay a one-time $20 million lump sum into their healthcare.

In the future, the city will be able to use temporary layoffs, if needed, during an economic crisis.

The deal marks a compromise for both sides. According to WPVI, the deal will prove expensive for the city—estimates put the cost at $127 million over five years—that will require some budgetary finagling.

One major concession for the union was that sick leave will no longer be eligible for overtime pay.

The investment will be placed in the American Century Non-U.S. Growth strategy, which looks for companies with a market capitalization of $3 billion or more, with accelerating growth and improving fundamentals. The overall portfolio typically invests in about 90 to 135 companies.

The investment management team is led by Senior Portfolio Manager Rajesh Gandhi, a 17-year financial services veteran who joined American Century in 2002.

The Arizona State Retirement Systems manage $34 billion in assets for 500,000 members.

Portfolio Manager Rajesh Gandhi explains his investment strategy in this video, courtesy of American Century.

Christopher Gonzales, the Chief Investment Officer of the Houston Firefighters Relief and Retirement Fund (HFRRF), resigned from his position today. As Pensions & Investments reports:

Mr. Gonzales said he has taken a position with a corporate retirement plan. He declined to provide further information. He has been CIO at the pension fund for 13 years. His last day is Sept. 12.

The board will discuss how to handle the upcoming vacancy at a special board meeting on Thursday, said Chairman Todd E. Clark.

Notably, Gonzales is a staunch supporter of private equity investments. The most recent data reveals the HFRRF allocated just over 10 percent of its assets towards private equity in 2013, but that number was once as high as 18 percent.

In an op-ed written for Pensions & Investments in January 2014, Gonzales lauded the performance of his fund’s private equity investments:

For the second year in a row, the Houston Firefighters’ Relief & Retirement Fund was among the top ranked in the Private Equity Growth Capital Council’s top 10 pension funds by private equity returns.

HFRRF earned a fourth-place spot in the private equity return ranking with a 13.6% annualized return, net of fees, over the 10 years and 9.3% over the five years, ended June 30, 2012.

Returns have shown consistency. In the 10 years ended June 20, 2011, the PEGCC study ranked HFRRF seventh best in private equity portfolio performance.

The PEGCC’s report showed that private equity returns to large public funds outperformed all other asset classes with median annualized 10-year returns of 10% for the subset of 146 large public pension funds that published 10-year returns ended June 30, 2012.

The HFRRF returned 11.24 percent, net of fees, in 2013 after returning 1.89 percent in 2012 and 20.29 percent in 2011.

California is often on the cutting edge of trends that eventually reverberate throughout the rest of the country. The same is true of CalPERS, the pension fund that was among the first to invest in real estate, hedge funds and private equity.

So when CalPERS announces a dramatic change in investment strategy, other funds drop what they’re doing and listen. Funds are certainly listening lately, as CalPERS is considering a handful of moves that would shift its asset allocation significantly.

Among them: the fund is considering taking all of its money out of commodities. From the Wall Street Journal:

One of the more-dramatic moves under consideration is a complete pullback from tradable indexes tied to energy, food, metals and other commodities, according to people familiar with the discussions. Calpers began making such investments in 2007 as a way of diversifying its portfolio and it currently has $2.4 billion in such derivatives, or less than 1% of total holdings.

[…]

The discussions are taking place between the fund’s interim Chief Investment Officer Ted Eliopoulos and Calpers’s other top investment executives. The Calpers board hasn’t yet been informed about any possible changes and no final decisions have been made, the people said.

The move, however jarring, wouldn’t be out of step with other recent investment decisions by CalPERS. The fund has shown a willingness to exit large investments it considers risky. From Wall Street Daily:

CalPERS’ potential retreat from riskier investments is evidence that it’s trying to simplify its portfolio and guard against losses during the next market downturn.

In a sense, CalPERS is turning to a bit of a “risk off” mode in this time of uncertainty.

Ultimately, with the realization that we’re in the midst of the Fed’s continued tapering, talk of interest rates hikes, and geopolitical unrest from the Middle East to the Ukraine, it may be time to dial down risk and play it safe.

In fact, this move is reflective of last fall, when CalPERS hinted at a shift away from complex investments, warning that the fund “will take risk only where we have a strong belief we will be rewarded for it.” This decision came after it had approved a new set of investment goals that reduced future exposure to equities and private equity, while increasing allocations to bonds and real estate.

A similar move by CalPERS also took place at the end of 2012, when the fund chopped commodities investments by more than half – prompting reports that it was shifting from commodities to inflation-linked bonds.

And in both incidences, the commodities markets experienced corrections.

CalPERS is weighing several other ideas, including whether forgo individual stocks in favor of securities that track broader industries.

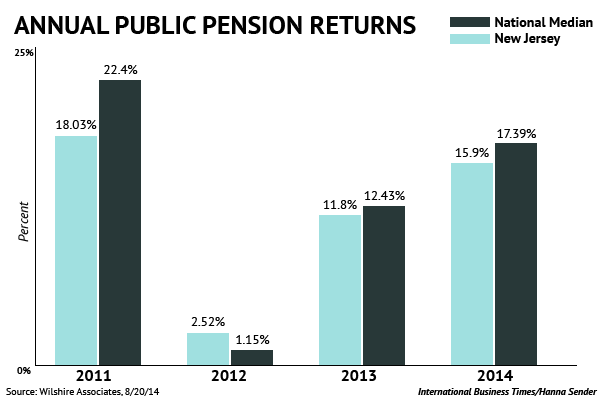

New Jersey is one of the most active states in the country when it comes to investing pension fund assets in hedge funds. That strategy carries risks and boatloads of fees—but it also carries potentially big returns.

Journalist David Sirota investigated the state’s investment decisions and the corresponding return data. He found that New Jersey was certainly straddled with management fees.

Between fiscal year 2011 and 2014, the state’s pension trailed the median returns for similarly sized public pension systems throughout the country, according to data from the financial analysis firm, Wilshire Associates. That below-median performance has cost New Jersey taxpayers billions in unrealized gains and has left the pension system on shaky ground.

Meanwhile, New Jersey is now paying a quarter-billion dollars in additional annual fees to Wall Street firms — many of whose employees have financially supported Republican groups backing Christie’s reelection campaign.

Neither Christie nor the state pension fund’s top investment official responded to Sirota’s requests for comment. But to a certain extent, the numbers speak for themselves. Here’s a chart of the state’s management fees since 2009:

In 2009, the year before Christie took office, New Jersey spent $125.1 million on financial management fees. In 2013, the most recent year for which data is available, the state reported spending $398.7 million on such fees. In all, New Jersey’s pension system has spent $939.8 million on financial fees between fiscal year 2010 and 2013.

That’s only a little less than the amount Christie cut from state education funding in 2010 — a cut that played a major role in shrinking the state’s teaching force by 4,500 teachers. That money might also have reduced the amount the state needs to pay into the pension system to keep it solvent.

That last part, bolded, is important. A major catalyst behind New Jersey’s incoming round of pension reforms was the state’s towering pension payments. Christie decided to divert money from those payments to plug holes in the general budget.

But that decision decreased the health of the state’s pension systems, and Christie now intends to introduce another series of reforms which will likely focus on cuts to benefits.

As you can see, there’s a lot of cause-and-effect reverberating throughout New Jersey’s pension system right now.