Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; Translation_Entry has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/entry.php on line 14

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_Reader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 12

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_FileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 120

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_StringReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 175

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 221

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; POMO_CachedIntFileReader has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/pomo/streams.php on line 236

Deprecated: Methods with the same name as their class will not be constructors in a future version of PHP; WP_Widget_Factory has a deprecated constructor in /home/mhuddelson/public_html/pension360.org/wp-includes/widgets.php on line 544

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/load.php on line 585

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712 Pension360 | The Complete View of Public Pensions | Page 269 Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

Deprecated: Function get_magic_quotes_gpc() is deprecated in /home/mhuddelson/public_html/pension360.org/wp-includes/formatting.php on line 3712

While most of the world was sleeping last week, lawmakers in Pennsylvania were scrambling to put the finishing touches on the state budget before the constitutionally-mandated midnight deadline. A little more than an hour before the clock struck 12, a budget was finally put on the desk of Pennsylvania Governor Tom Corbett. Only one problem: he won’t sign it. From the Philadelphia Enquirer:

Gov. Corbett refused late Monday to sign a $29.1 billion budget that the Republican-controlled legislature scrambled to deliver to him just 90 minutes before the midnight deadline.

The legislature approved a plan that includes some increased money for schools, and would not raise any taxes or impose new ones.

But Corbett, a Republican facing a tough reelection battle in the fall, signaled disappointment that the legislature was unable to deliver on one of his priorities: a measure that would change pension benefits for new employees.

“The budget I received tonight makes significant investments in our common priorities of education, jobs, and human services,” the governor said in a statement shortly before 11 p.m. “It does not address all the difficult choices that still need to be made. It leaves pensions, one of the largest expenses to the commonwealth and our school districts, on the table.”

He added: “I will continue to work with the legislature toward meaningful pension reform. I am withholding signing the budget passed by the General Assembly while I deliberate its impact on the people of Pennsylvania.”

It was unclear how long Corbett, who has often boasted of his record of delivering on-time budgets, would hold out. A protracted stalemate could affect the state’s ability to pay bills or workers.

The decision between funding pensions and funding the rest of the state is a difficult one. The ordeal has put Gov. Corbett in between a political rock and a hard place, and its unlikely he will come out of this process unscathed–at least in the electorate’s eyes:

Down by double digits in public opinion polls, Republican Gov. Tom Corbett has few good political choices when deciding by Friday whether to sign the state budget — except some high-risk options of taking on the Legislature, analysts say.

“None of them are great options for the governor in an election year,” said Christopher Borick, a professor and pollster at Muhlenberg College in Allentown. Corbett of Shaler trailed Democrat Tom Wolf of York by 22 points in a Franklin & Marshall poll last week on the November election.

• Let it become law without his signature on Friday, because a governor has 10 days to consider legislation before it automatically becomes law;

• Veto the entire bill;

• Veto some spending in the bill, including the Legislature’s funding.

Corbett could call a special session, which requires lawmakers to gavel into session, but he cannot compel them to consider pension reform if they return.

Over the years, special sessions have had mixed success, experts say. The governor sets the agenda. Topics have included gun control, crime, transportation and property tax reform.

Lawmakers can gavel out of special session and into regular session to consider anything they want.

“It seems like a no-win situation,” said Michael Federici, a political science professor at Mercyhurst University in Erie. “The closer you get to an election, the less willing Republicans will be to sign on” to pension reform.

Gov. Corbett needs to make a decision by Friday–if he doesn’t veto the bill, it will automatically become law.

It’s a question that goes through the mind of everyone: Will I have enough money saved to live comfortably and securely when I retire?

A new survey from Pew Charitable Trusts asked that very question. Turns out, when it comes to retirement, the minds of public sector employees are more at ease than the American workforce on the whole:

According to a survey from The Pew Charitable Trusts, 69% of public employees said they were very or somewhat confident they would have enough money to live comfortably in retirement, compared with 55% of [private and public sector] Americans surveyed for the Employee Benefit Research Institute’s (EBRI) 2014 Retirement Confidence Survey. Female public employees were less likely than men to express confidence in their retirement situation: 63% of women said they were very or somewhat confident, compared with 77% of men.

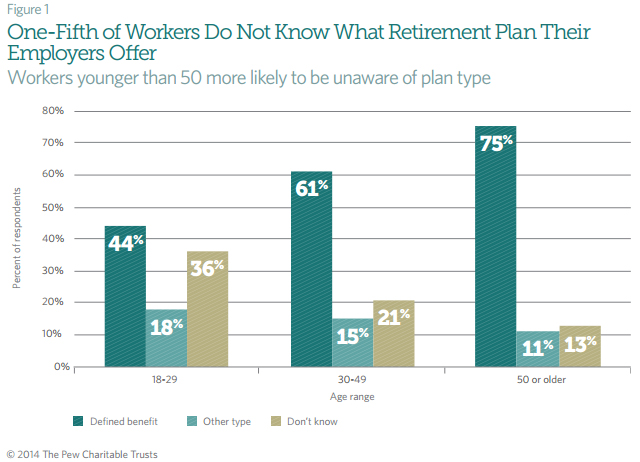

But perhaps the most shocking reveal of the survey was that one of every five public employees didn’t know what kind of retirement plan was offered by their employer.

One-fifth of state and local workers polled said they did not know what type of retirement plan their employers offer. Women were more likely to say this (23%) compared to men (15%). In addition, workers younger than 50 were more likely to report that they did not know what type of retirement plan they have than were workers 50 or older.

Slightly more than half (54%) of state and local public workers said they expected to retire at age 65 or later. Of this group, 25% said they expect to retire at 65, and 29% said they expect to retire after 65. An additional 4% of respondents volunteered that they do not ever expect to fully retire. These results are similar to findings in the EBRI survey.

And how plan design affects retirement decisions:

State and local employees said retirement plan design affects decisions about when to stop working. Eighty percent said they think some government employees who want to leave their jobs keep working until retirement age so they will not lose retirement benefits, including 60% who said they think this happens a lot. Fifty-six percent said they think some workers retire earlier than they would like in order to maximize retirement benefits, including 31% who think this happens a lot. Overall, 88% of respondents said they think workers either work longer or retire earlier than their preference in order to maximize retirement benefits, including 48% who think both things happen.

Many employees also think their plans are in need of changes, whether they be minor tweaks or major overhauls:

Thirty-five percent of respondents said their employer’s retirement system needs changes, including 12% who said it needs major changes. Sixty-one percent said they think their employer’s retirement system should be kept as it is. Those with lower confidence in their ability to live comfortably in retirement were more likely to say they would like to see changes. So were women (38%) compared with men (30%).

While the rest of the country celebrated Fourth of July weekend, members of the Illinois pension sphere got to watch some fireworks of their own. A key Illinois Supreme Court case was decided over the weekend, and the decision does not bode well for the state’s landmark pension reform. (The full court opinion can be read at the bottom of this page.)

According to the 6-1 decision, the pension protection clause — which says that retirement benefits are a contractual agreement that “cannot be diminished or impaired” — applies to other retirement benefits, not just pensions. That overrode the state’s argument that its emergency powers, in dealing with its budget crisis, justified an increase in what retirees must pay for their health benefits.

The court rejected the state’s argument that health care benefits are not covered by the pension protection clause, finding that there is nothing in the state constitution to support that. The only question now is whether the reduction in the state’s health care subsidies constituted an impairment or diminishment of those benefits.

Although the ruling doesn’t directly apply to pensions, the writing seems to be on the wall.

“If the justices can read the pension clause of the constitution to protect health benefits, they certainly would use it to protect pension benefits,” former state Budget Director Steve Schnorf said.

“This bodes very, very ill” for the pension cuts the Legislature approved for state workers, and for a similar set of trims Mayor Rahm Emanuel wants for his workforce, he added.

Time after time, without finally resolving the issue, the court seemed to go out of its way to knock down any changes not agreed to by workers unions, and perhaps by each individual worker.

For instance, one argument defenders of the new pension law have offered is that unfunded pension liability now is so large — $100 billion in the state funds, and at least $32 billion in the city funds, for instance — that government has a right to order changes, using its so-called police powers, to set spending priorities. But, said the court, “In light of the constitutional debates, we have concluded that the (pension) provision was aimed at protecting the right to receive the promised retirement benefits, not the adequacy of the funding to pay for them.”

Another argument offered by reform proponents is that annual cost of living adjustments in pensions are not protected by the state constitution in the same way that a person’s original pension is. In other words, a worker who initially got, say, a $3,000-a-month pension is entitled to get it and no more in the future, regardless of inflation. COLAs are far and away the biggest element in the retirement-funding crisis.

But, ruled the court, “Under settled Illinois law, where there is any question as to legislative intent and the clarity of the language of a pension statute, it must be liberally construed in favor of the rights of the pensioner. ”

So, the current 3 percent guaranteed annual COLA would appear to be here to stay.

Ironically, such an interpretation would apply both to the pension reform bill pushed by Gov. Pat Quinn that’s working its way up to the Supreme Court and to an alternative plan offered by his opponent Bruce Rauner. The GOP gubernatorial candidate proposes moving workers to a defined-contribution system that caps state funding.

Many believe lawmakers should now be scrambling to come up with a Plan B to reform pensions in a way allowed by the courts:

State and local lawmakers had better get working on a Plan B. Illinois needs alternatives to the state pension-reform law passed in December and to the Chicago pension-reform law passed in May. The options are limited — it may come down to a constitutional amendment — but the state’s best minds better get cracking.

It isn’t an exaggeration, even in the slightest, to say Illinois’ future depends on it.

There is now but one key question: Does a viable pension reform alternative exist? A bill pushed by Senate President John Cullerton, considered an alternative by many, is now almost certainly off the table. That bill gave workers a choice between full pension benefits or subsidized health care — choose pension benefits and health care would be cut. Given Thursday’s ruling, that now seems highly dubious.

One possibility would be to amend the constitution to modify the pension protection clause — not eliminating it but weakening it some. However, this is a lengthy process and may still not protect the state legally if it reduces benefits already promised.

The world is now watching Australia as the country readies itself for a bold shift in pension policy: raising the retirement age to 70, which would be the highest retirement age in the developed world.

Australia’s workers had previously been able to retire at 65. The five year increase will be phased in over many years, and will take full effect in 2035. The plan was announced by Australian Treasurer Joe Hockey:

Hockey is part of the Liberal-National coalition that won power in September, pledging to end what he called the nation’s Age of Entitlement and repair a budget deficit forecast to reach $49.9 billion AUS this fiscal year. Australia is leading the charge for a group of advanced economies from Japan to Germany that are pushing the retirement age higher to head off a gray disaster caused by a growing army of pensioners and a declining pool of taxpayers.

The ratio of working-age Australians to those over 65 in the world’s 12th-largest economy is expected to decline to 3-1 by 2050 from 5-1 in 2010. In Japan it’s already below 3-1 and in Germany it’s close to that level, according to the International Labor Organization.

“While Australia may be the first to raise the age to 70, it won’t be the last,” said Steve Shepherd of international employment agency Randstad Group in Melbourne. “The world will be watching this.”

Australia’s 2.4 million state-retirement-age pensioners draw about $40 billion AUS a year, making it the largest government spending program. That’s forecast to rise 6.2 per cent a year over the next decade, according to an independent review commissioned by Prime Minister Tony Abbott. The program provides the main source of income for 65 per cent of retired Australians.

Failure to rein in the program would put a greater onus on younger workers to fund it through increased contributions and taxes. Raising the pension age may also mean more competition for those just starting in the workforce. Unemployment among those aged 15-24 reached a 12-year high of 13.1 per cent in May, more than double the national average of 5.8 per cent.

Research shows many people struggle to work until they are 60, let alone 70. The Household, Income and Labour Dynamics in Australia (HILDA) Survey shows that the average retirement age from 2003 to 2011 for men was 62.6 years old and for women it was just under 60. While that is rising, it is still well below the current retirement age of 65.

And the HILDA data shows, for men, nearly half of all retirements are involuntary with most due to poor health. Women are more likely to retire on their own terms but still 43 per cent retire due to reasons such as ill health, losing their job or having to care for others.

The rest of the world will be happy to sit on the sidelines and watch this fascinating policy shift play out.

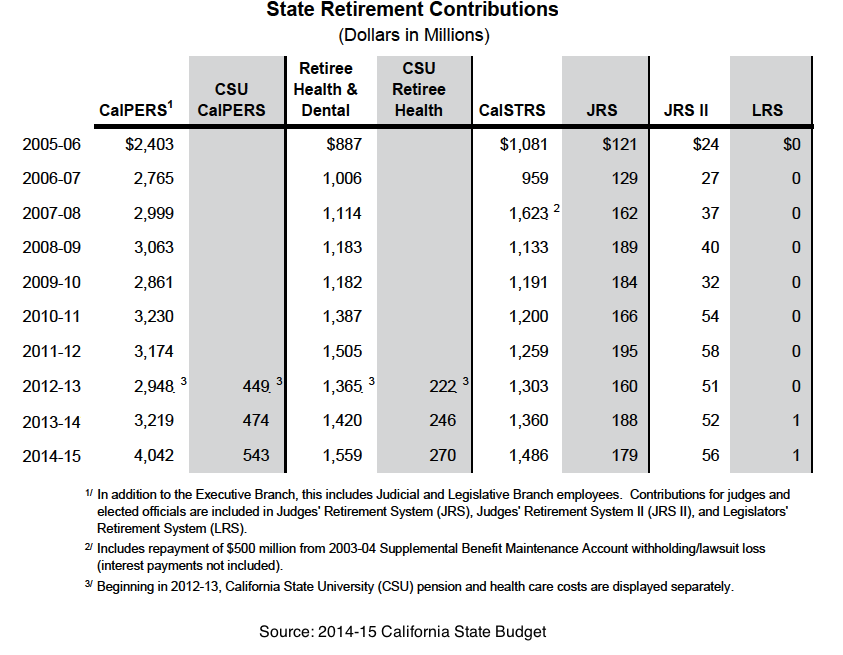

California actually has a good track record making its payments to CalPERS — unfortunately, the same can’t be said for CalSTRS. Even so, the state’s track record on both fronts got better last week when lawmakers upped its 2014 payment to the two systems by a combined $1 billion.

Contributions to CalPERS aren’t the problem; the state has made good on their Actuarially Required Contribution for years now (although, if we’re being honest, the fund could always use more state dollars. And there’s no rule against paying more than 100% of an ARC). But CalSTRS is another story.

For years, CalPERS—the largest public pension fund in the country— was a hotbed of backdoor scheming, shady dealings and outright fraud.

That was thanks to two long-time friends, Fred Buenrostro and Alfred J.R. Villalobos, who we now know (well, allegedly) profited greatly from greasing the wheels on billions of dollars of CalPERS investments from behind the scenes in 2007-2008, and probably years before.

Buenrostro was CalPERS’ CEO from 2002-2008, and Villalobos sat on the fund’s Board from 1993-1995.

The story starts in 2007 when Villalobos, acting as a placement agent, was hired by the investment firm Apollo Global Management to secure investment business from CalPERS.

The two men created a series of fake letters on CalPERS’ stationery to make sure Villalobos got paid millions in commissions by a Wall Street private equity firm that was investing the pension fund’s money.

Buenrostro created phony letters on the pension fund’s letterhead after another CalPERS official refused to sign the disclosure documents. After receiving the letters, Apollo was able to obtain $3 billion in CalPERS investments between August 2007 and April 2008.

Villalobos, by the way, earned around $50 million worth of commission from those deals, according to CalPERS reports.

But Buenrostro made out well, too: after he retired from CalPERS in 2008, he was allegedly gifted a free Tahoe condo and a cushy job at Villalobos’ investment firm.

In March 2013, former California Public Employee Retirement System CEO Fred Buenrostro was indicted by a San Francisco grand jury and charged with conspiracy in connection with a scheme involving fraudulent documents related to a $3 billion investment by the retirement system in funds managed by Apollo Global Management.

Now, over a year after charges were filed against the two men, it seems one of them has finally admitted to himself that the gig is up—Buenrostro’s lawyer told a judge Monday that he plans to enter a guilty plea and cooperate with authorities. That includes assisting the government with its case against Villalobos.

Buenrostro’s plea bargain isn’t yet final, so it isn’t clear how much jail-time he is now looking at.

The True Cost?

This isn’t nearly the first time corruption and fraud has made its way in the public pension system, and it won’t be the last. That’s why its important to assign some numbers to these news stories—if only so we can appreciate the tangible costs that this type of cronyism incurs to the system, its members and taxpayers on the whole.

CalPERS had been putting money in Apollo funds for years—at least as far back as 2002. But the alleged misconduct supposedly happened between 2007 and 2008, when CalPERS put quite a lot of money in the hands of Apollo.

Those investments included at least six Apollo funds: Apollo Investments FD III LP; Apollo Group Inc Cl A; Apollo investment Fund VII LP; Apollo Global Management LLC; Apollo Real Estate Investment Fund; and Apollo Euro Principal Finance.

CalPERS still has all of those funds on the books as of 2013 except for two: Real Estate Investment and Europe Principal Finance. The system offloaded those two in 2012 with mixed results—Real Estate Investment Fund had lost $19 million of its book value, a 32% loss. Meanwhile, Europe Principal Finance had fared well, and saw its value increase 23% by the time CalPERS got out.

Of the four funds still on CalPERS’ books, three of them are now worth significantly less than their book value: Investment FD III LP is down 43%; Group Inc Cl A is down 57%; and Global Management LLC was down over 8%. All in all, those funds lost about $56 million of their book value. (These are all 2013 numbers—the most recent CalPERS provides.)

However, CalPERS got bailed out by one Apollo fund which did so well it erased all those losses and then some: the Investment Fund VII LP, whose market value in 2013 stood 47% higher than its book value. If CalPERS got out today, they would come out with over $200 million.

With great risk comes great reward. And Fund VII was certainly a risk—it was invested heavily in distressed companies:

In Fund VII, 57 percent of Apollo’s deals involved buying debt of distressed companies or buying distressed companies outright, while only 28 percent were straightforward acquisitions of companies not in distress. Corporate carve-outs of divisions accounted for 15 percent.

It paid off for CalPERS, as Fund VII has been one of the best-performing private equity funds in the world since 2008.

Still, four out of those six funds lost value. If CalPERS had invested that money in other funds, would they have fared better? We’ll never have any idea.

But the point is, these investment decisions were not made on the merit of the investments themselves, but instead on the basis of friendship and monetary gain for the dealmakers involved.

In late May 2004, Alfred Villalobos hosted a meeting at his home in Nevada, a few miles from Lake Tahoe and the California border. Villalobos was joined by David Snow, the Chairman and Chief Executive Officer of Medco Health Solutions, one of the nation’s largest pharmacy benefit management (“PBM”) companies, and Fred Buenrostro, who was the Chief Executive Officer of CalPERS at the time.

Soon after the May 2004 meeting at the Villalobos home, Medco agreed to retain Villalobos as a consultant and pay him $4 million.

Buenrostro was married in 2004, while serving as CEO, and allowed Villalobos to not only host the wedding at his home in Nevada, but reportedly also allowed Villalobos to pay for the event as well as lodging nearby for Buenrostro’s guests who attended the ceremony.

In October 2005, the year after Buenrostro got married on Snow’s consultant’s dime, Medco got the CalPERS contract.

That contract was worth $48 million dollars, and you can bet Villalobos got a hefty finders fee for that, too.

One thing’s for sure: he’ll be able to afford a lot of cigarettes in prison.

Author: Paul M. Secunda, Marquette University – Law School

ABSTRACT: It is nearly impossible in the United States today to go long without reading a headline about some aspect of the American public pension crisis or about some State undertaking public pension reform. Public pensions are horribly unfunded, millions of public employees are being forced to make greater contributions to their pensions, retirees are being forced to take benefit cuts, retirement ages and service requirements are being increased, and the list goes on and on. These headlines involve all level of American government, from the recent move to require new federal employees to contribute more to their pensions, to the significant underfunding of state and local public pension funds across the country, to the sad spectacle of the Detroit municipal bankruptcy where the plight of public pensions plays a leading role in that drama. The underfunding of public pension plans has led not only to a number of bankruptcy proceedings, but has also led various states to reduce promised pension payouts to retired plan members or to increase pension contribution requirements for active employees. As a result, government officials, employees, and retirees are in the midst of litigating for the future of American public pensions. This article focuses on all three levels of American government (federal, state, and local), and reviews the current status of pension litigation at each level.

This is the first in a series of charts designed to illustrate the context and consequences of New Jersey Gov. Chris Christie’s plan to cut the state’s pension contributions by $2.4 billion over the next two years.

As you’ll see in the chart below, beginning in 2010 New Jersey was slowly paying higher percentages of it’s required annual contributions into the pension system. Its 2014 payment was set to be the biggest yet–but that will no longer be the case.

Stay tuned for more charts on a weekly basis, including New Jersey’s contributions to other systems, what those contributions look like side-by-side with unfunded liabilities, and how Christie’s cuts will affect system liabilities and state contributions going forward.

California is a state known for its positive vibes, but those vibes have not historically extended to its financial condition. That’s changed just a bit in the last week, due to a string of financially sound (and therefore surprising) budget decisions on the pension front.

It happened last Tuesday, when Gov. Jerry Brown signed into law a section of the state’s new budget that addressed CALSTRS’ $74 billion shortfall by raising contributions rates from teachers, school districts and the state. The budget also addressed CalPERS’ underfunding by increasing the state’s 2014-15 contribution by a pretty sizeable amount.

An important note: it took Moody’s less than 24 hours to upgrade California’s credit rating after seeing this budget—from A1 to Aa3—and predictably, those pension provisions were a big reason why. That’s important, because states need all the positive reinforcement they can get when it comes to making these politically tough decisions.

And they were politically tough (albeit economically obvious) decisions—the California Teachers Association donated $290,000 to state politicians during the last election cycle, and put $4.7 million in Gov. Brown’s coffers to help elect him in 2010.

Okay, now the details of the budget.

The portion of the budget summary that addresses the state’s pension systems, which you can read here, leads with this line:

In its 101‑year history, contributions to CalSTRS have rarely aligned with investment income to meet the promises owed to retired teachers, community college instructors, and school administrators.

Indeed. That’s refreshingly honest, even if those issues only represent a fraction of California’s larger pension problems.

To be fair, the state’s recent pension reform law addressed some of these issues in 2012 by raising retirement ages and reducing benefits. But it wasn’t enough, and the budget says as much:

Even with those changes, and despite recent investment success, the viability of CalSTRS ultimately requires significant new money on an annual basis.

My god, the state budget has become self-aware! And it doesn’t matter if lawmakers are playing the part of Captain Obvious here. It’s still a positive sign to see this stuff, in writing, in the document that’ll be determining the state’s expenditures for the next fiscal year.

Onto the numbers: The budget directs an additional $276 million in contributions from teachers, schools and the state to the CALSTRS system in fiscal year 2014-15. That will be accomplished by:

Increasing teacher contribution rates from 8 percent of pay to 10.25 percent of pay, to be phased in over the next three years.

Increasing school contribution rates from 8.25 percent of payroll to 19.1 percent of payroll, to be phased in over the next seven years.

Increasing the state’s contribution rate from 3 percent of payroll to 6.3 percent of payroll over the next three years.

The budget gives the CALSTRS Board the authority to increase school and state contributions if they see fit. On the other hand, the Board gets the authority to reduce them, too.

CalPERS is also set to receive a big contribution from the state, which is good news because California was consistently lagging behind in that department before modestly increasing its contribution last year. But 2014 represents a big step forward, as the state increases its contribution by 20 percent.

This coming fiscal year (2014-15) will also represent the 7th straight year California has increased its contribution to CalSTRS. All told, the plan is to fully fund CALSTRS in 30 years.

Of course, that projection is contingent on CalSTRS meeting its investment return assumptions, which currently sit at 7.5% annually. How likely is it to meet that target over the next 30 years?

“Highly unlikely,” said Gov. Brown at a press conference back in May.

He’s right. And it’s important to maintain perspective.

This is but a small step on the road to responsibly managing the state’s pension funds. Declaring victory now is like buying a house on a 30-year mortgage, making the first payment without a hitch and then proclaiming, “We did it!”

All the same, it is a step forward, and you need to crawl before you can walk. Let’s hope California learns how to run sooner than later.

By now, you know the story: New Jersey Gov. Chris Christie’s plan to cut pension funding by $2.4 billion over two years has been met with controversy, outrage, a string of lawsuits and numerous legal questions.

The answers to some of those legal questions may come as soon as Wednesday, when Christie’s plan will see its first day in court.

But outside the courtroom, a new bill is gaining steam among state lawmakers—a bill that finally puts a tangible, short-term solution on the table. And even if it doesn’t come without its kinks, it’s the first plan that has been offered up to counteract Christie’s measure. (More on the bill below).

Meanwhile, more data is emerging on the true costs of Christie’s plan. Spoiler alert: the snowball effect is real, and it’s prohibitively expensive.

Cuts Bring Consequences, Now and in the Future

Every passing day brings a bit more clarity as to just how expensive Christie’s plan to cut pension funding by $2.4 billion would be. In a bond disclosure released by the state, the ramifications of the cuts are outlined in four points.

The proposed reduction in contributions…could have the effect of (1) delaying the phase-in of the State’s full actuarially required contribution, (2) increasing the amount of such contribution, (3) increasing the size of the UAAL and (4) decreasing the percentage of the Funded Ratio of the Pension Plans once the phase-in is completed.

Indeed, New Jersey can expect all four of those points to materialize, some sooner than others. And when you attach numbers to them, the urgency of New Jersey’s upcoming fiscal situation really starts to set in. If Christie goes through with his plan, here’s what New Jersey could be facing in fiscal year 2019:

The state’s actuarially required contribution would be $4.8 billion—for context, that sum would represent 26 percent of New Jersey’s general fund budget, based on 2012 expenditures.

The unfunded liabilities of the state’s pension plans would total $46 billion. Christie could decrease these liabilities by $4 billion if he scrapped his plan to cut contributions by $2.4 billion in 2015-16.

The funded ratio of state plans would drop to 48.25 percent. The funded ratio sat at 67.5 percent in 2011.

Rest assured, Christie has seen these numbers—they came from his own financial team.

A New Bill Emerges in the Legislature

On Monday, news broke that New Jersey state legislature had agreed on an alternate budget proposal that would raise enough revenue to cover the state’s full contribution to the pension system, a payment that Christie’s plan had drastically cut.

Sources inside the legislature told the Star-Ledger that Democrats in the state Senate and Assembly had reached a deal to raise more than $1.3 billion in revenue—money that would cover the state’s full annual contribution of $2.25 billion to the pension system. Christie’s plan had cut that payment down to just $681 million.

The revenue would come from tax increases on high-income earners and businesses, among other things. From the Star-Ledger:

Under the Democrats’ budget:

• The marginal tax rate on income above $1 million would rise from 8.97 percent to 10.75 percent, retroactive to January of this year, netting $667 million.

• The corporate business tax would rise from 9 percent to 10.35 percent, yielding $375 million.

• The Business Employment Incentive Program (BEIP) of tax abatements would be suspended for a year, freeing up $175 million.

• A tax hike on income between $500,000 and $1 million that Sweeney had proposed would be scrapped, as Prieto suggested.

In addition, some new taxes or fees Christie proposed would be folded into the Democrats’ budget, such as a penalty for making bad electronic payments ($25 million) and a move to subject all online retailers to the state sales tax ($25 million).

Taxes Christie proposed on electronic cigarettes and the Urban Enterprise Zone program would be cut out of the budget under the Democrats’ deal.

Of course, the deal doesn’t come without its hitches. Despite the bill’s focus on raising revenue, it actually earmarks more money toward several of the areas that Democrats lost out on in the last budget dealings: the new bill restores funding for the Earned Income Tax Credit, nursing homes, legal services for the poor, and women’s health care centers.

Those are all items that deserve funding, but their inclusion makes the bill much less politically palatable to lawmakers on the other side of the aisle. Of course, it was already unpalatable to politicians who, on principle, oppose tax increases.

Indeed, state Republicans are none too happy about the proposed measure.

“It would be suicidal to…New Jersey’s economy,” said Assemblyman Declan O’Scanlon (R-Monmouth) during a Monday morning press conference.

The Democrats would likely be able to overcome Republican opposition. They hold 48 seats (60 percent) in the General Assembly, and 24 seats (60 percent) in the Senate.

The Senate and General Assembly are holding hearings on the bill Tuesday, and the measure is expected pass by vote through the two houses by Thursday.

Still, the chances that the bill becomes law in its current form, or at all, are slim. That’s because the buck stops with Gov. Christie, who has line-item veto power and has repeatedly states he will oppose any tax hikes on wealthy individuals or businesses.