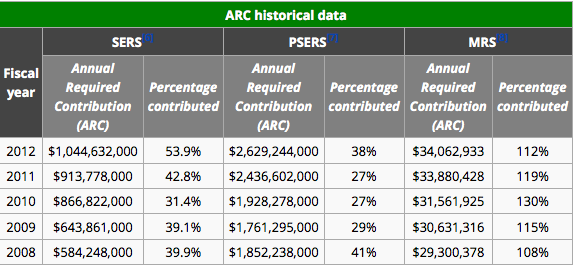

San Francisco Employees’ Retirement System (SFERS) was set to vote yesterday on whether the fund should allocate up to 15 percent of assets, or $3 billion, to hedge funds.

But the vote never happened, in part because of the objections of union members and retirees who showed up to the meeting. Recent reports of conflicts of interest surrounding the hedge fund investments probably didn’t help, either.

From the International Business Times:

San Francisco officials on Wednesday tabled a proposal to move up to 15 percent of the city’s $20 billion pension portfolio into hedge funds. The move came a day after International Business Times reported that the consultants advising the city on whether to invest in hedge funds currently operate a hedge fund based in the Cayman Islands.

The hedge fund proposal, spearheaded by the chief investment officer of the San Francisco Employees’ Retirement System, or SFERS, had been scheduled for action this week. If ultimately enacted, it could move up to $3 billion of retiree money from traditional stocks and bonds into hedge funds, potentially costing taxpayers $100 million a year in additional fees.

Pension beneficiaries who oppose the proposal spoke at Wednesday’s meeting of the SFERS board. They cited financial risks and the appearance of possible conflicts of interest in objecting to the hedge fund investments.

Prior to the meeting, the Service Employees International Union, which represents roughly 12,000 members who are eligible for SFERS benefits, asked city officials to have the hedge fund proposal evaluated by a consultant who has worked with boards that have opted against hedge funds.

David Sirota reported on the possible conflicts of interest earlier this week:

[SFERS is] drawing on the counsel of a company called Angeles Investment Advisors, one of a crop of consulting firms that has emerged across the country in recent years to aid municipalities in navigating the murky waters of managing money.

For two decades, Angeles has been employed by the San Francisco pension system to champion the best interests of city taxpayers and employees — the cops, firefighters and other municipal workers who depend on pension payments after their retirement. But the firm is concurrently playing another role that complicates its image as a disinterested guide: An International Business Times review of U.S. Securities and Exchange Commission documents has found that since 2010, Angeles has run a hedge fund based in the Cayman Islands that invests in other hedge funds.

In other words, the consultants that are supposed to be providing unbiased advice about whether San Francisco would be wise to entrust its money to the hedge fund industry are themselves hedge fund players.

SFERS says that, although the vote is tabled for now, it could be brought back at a later time.

This isn’t the first time the pension fund has delayed voting on hedge fund investments. In fact, it’s the third time: the board first delayed the vote in June. Then it delayed the vote again in August.