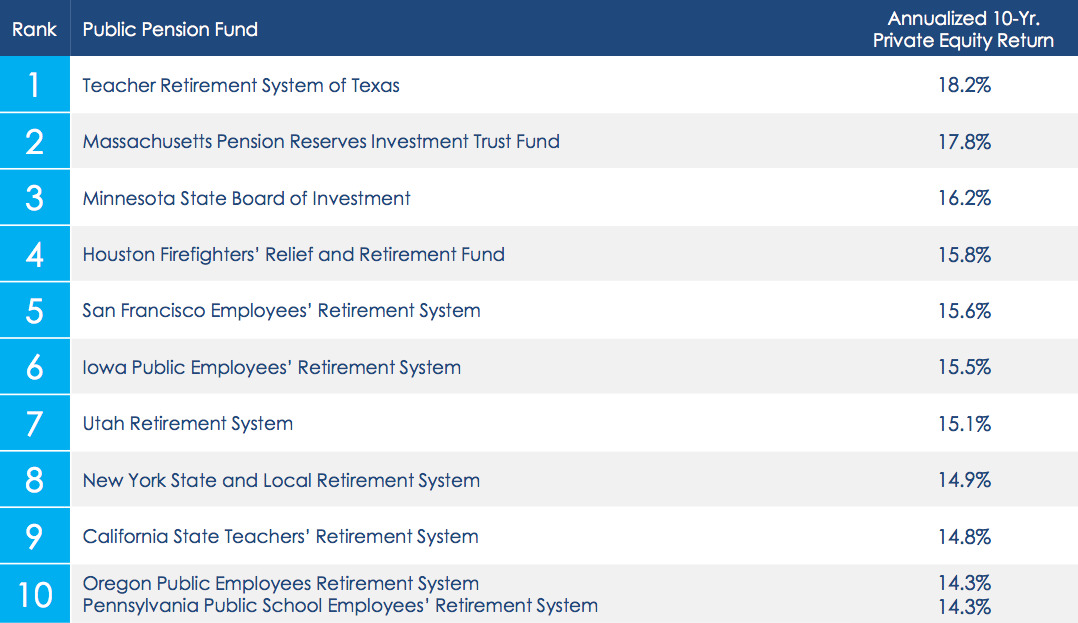

Japan’s Government Pension Investment Fund (GPIF) is in the process of increasing its domestic equity holdings from 12 percent of its portfolio to around 20 percent.

The pension fund announced the plan in June and the implementation is well underway – but one of the fund’s top advisors called the announcement “stupid”.

Why? Here’s his logic, explained by Chief Investment Officer magazine:

Takatoshi Ito, a vocal proponent of overhauling Japan’s $1.2 trillion Government Pension Investment Fund (GPIF), has been among those encouraging the giant fund to increase its allocation to domestic equities. But in an interview with Bloomberg this week, he warned against publishing target weightings before making asset allocation changes as the information could move markets before GPIF has a chance to access good prices.

Ito said: “Saying ‘we’re going to purchase as much as whatever percent’ before buying anything is a stupid idea. It’s tantamount to not fulfilling their fiduciary responsibilities and not appropriately investing the money entrusted to them. It’s wrong, and I’m against it.”

Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank, also hit out at the idea of announcing the allocation changes before acting. He said: “The market will front-run it, and our pension money will be invested at highs. It makes it pointless to entrust our savings to experts, and we should ask for it back so we can manage it ourselves. It makes those experts meaningless.”

The GPIF is currently reviewing its asset allocation, with Prime Minister Shinzo Abe having urged the fund to reach a decision this year. Ito said the fund has probably not started any shift yet, as it would become obvious through market data and filings when the trillions of yen expected to be reallocated start to move.

GPIF plans to slash its fixed-income holdings and shift more money towards domestic equities:

At the end of June the GPIF had 53.4% in domestic fixed income and 17.3% in Japanese equity. Ito’s personal recommendation, according to Bloomberg, was to slash the fixed income element to 35% of the portfolio and increase Japanese equities to 25%. This would involve the sale of roughly $220 billion in bonds and the purchase of roughly $96 billion in equities, based on the fund’s June 2014 valuation of ¥127 trillion ($1.2 trillion).

The GPIF manages $1.2 trillion of pension assets.

Photo by Ville Miettinen via Flickr CC License